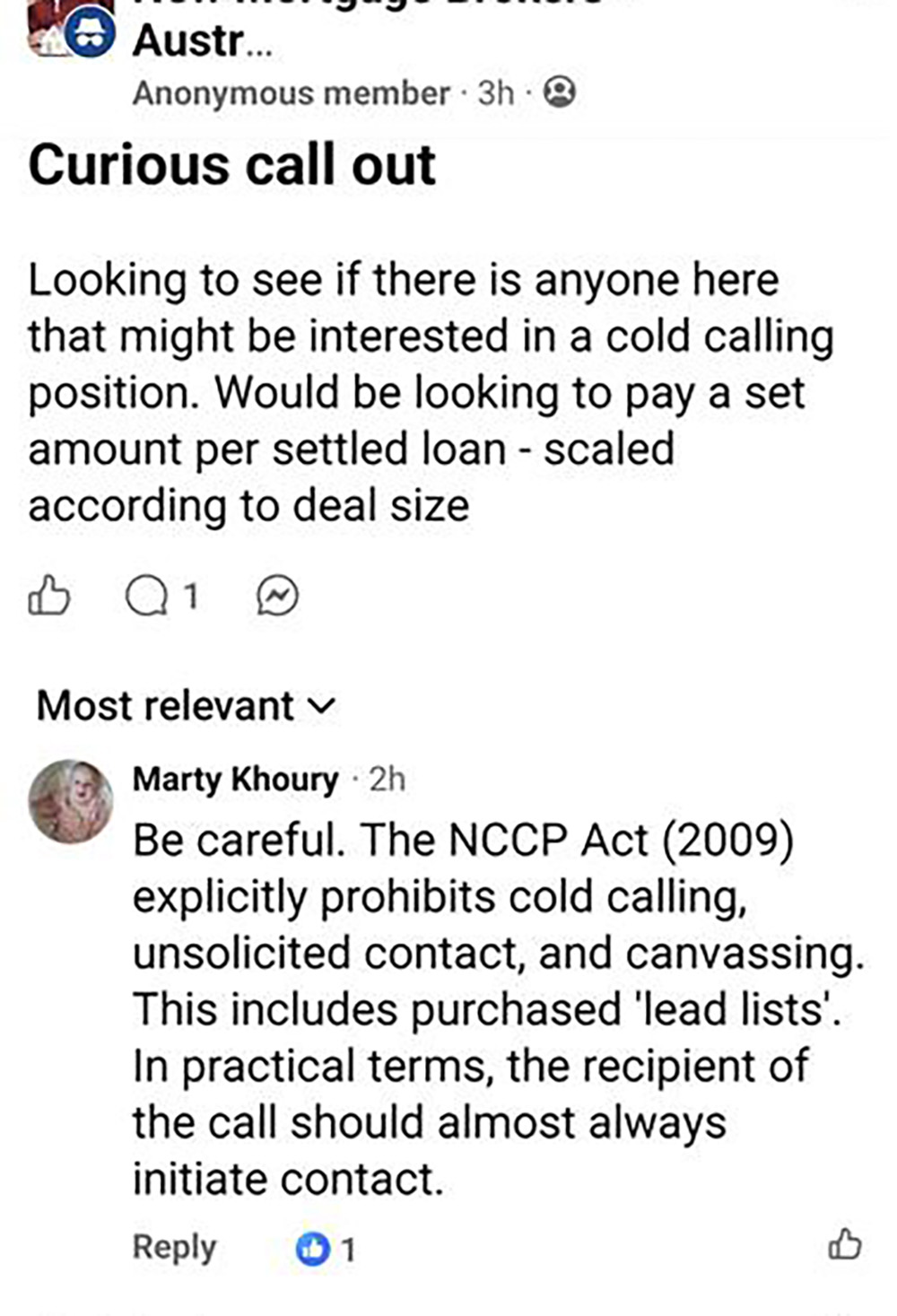

I came across a post on Facebook  today where a broker was scouting for an individual for the purpose of cold calling potential mortgage clients with renumeration determined by the loan size. Apart from the fact that the employment conditions are typically appalling, the role itself is one that exposes significant legal exposure. First, the person making these 'cold calls' is engaging with 'credit activities' in a manner not unlike illegal 'call setters', and the role itself is objectively illegal and the subject of very specific legislation. In this article, we'll look at the colder style of marketing which includes phone calls, LinkedIn and other social platforms, open home records, and general canvassing.

today where a broker was scouting for an individual for the purpose of cold calling potential mortgage clients with renumeration determined by the loan size. Apart from the fact that the employment conditions are typically appalling, the role itself is one that exposes significant legal exposure. First, the person making these 'cold calls' is engaging with 'credit activities' in a manner not unlike illegal 'call setters', and the role itself is objectively illegal and the subject of very specific legislation. In this article, we'll look at the colder style of marketing which includes phone calls, LinkedIn and other social platforms, open home records, and general canvassing.

Not Legal Advice: Nothing in this article represents legal advice of any type. We're merely discussing the practical application of unsolicited lead generation with reference to the legislation that prevents it. Consult your legal representation for information relating to your specific circumstances.

Marketing and Fintech: We are a marketing company and fintech company, but unlike others, we diligently measure legislation against our consumer-facing programs of all types to ensure compliance. While the focus of this article relates to unsolicited telephone calls ("cold calls"), the unsolicited messaging applies across all platforms - including social media, such as LinkedIn and similar. Many brokers engage in unsolicited messaging on LinkedIn (in particular) which is a practice that probably needs to stop if you choose to remain compliant. Again, our focus is high-performing technology, creative, and advertising... but we take necessary measures to ensure compliance.

Unsolicited cold calling for mortgage products is heavily restricted and, in most practical circumstances, prohibited. The relevant provisions sit within the Australian consumer credit regime under the National Consumer Credit Protection Act 2009, particularly the rules dealing with unsolicited contact and hawking. A mortgage broker, lender, or their representative generally cannot simply telephone a consumer out of the blue to promote or arrange a home loan if the consumer has not consented to the contact, so cold calling is expressly prohibited.

Meaning of unsolicited communication to a consumer (NCCP, 2009): An unsolicited communication to a consumer is a communication to a consumer or a consumer’s agent that is made by a person by dealing directly with the consumer or the consumer’s agent in any of the following circumstances: (a) no prior request has been made by the consumer to the licensee for that communication; (b) the consumer has made a prior request to the licensee for that communication and that request was solicited by or on behalf of the licensee; (c) circumstances of a kind prescribed by the [NCCP] regulations.

Best Interest Duty: NCCP Act, 158L, "A Licensee must act in the best interests of the consumer .. "[t]he licensee must act in the best interests of the consumer in relation to the credit assistance". Mortgage brokers also have a statutory best interests duty. Generally, an unsolicited sales approach will likely cause significant regulatory risk because it may suggest that the transaction originated from the salesperson's commercial interests rather than the consumer's expressed needs.

Video: The phone call in the video - one of several hundred we've recorded - was received at 1.02pm on 13th October 2025. The number displayed was (02) 8080 2104. There are a number of violations here outside the scope of this article, such as the caller offering product advice and rates, using a false company name (typical of leadgen, and the name often changes during the same conversation), avoiding disclosure of lender information, withholding information, and failing to provide a Credit Licence number when asked. These calls normally start with the fake "you will remember you spoke to my colleague last month..." - used to create uncertainty that will encourage the conversation. In this particular case, the call was tracked back to a service operating in Sydney as part of a much bigger fraudulent operation. I offered the identifying information to the CEO and legal council from a large aggregation group but acesss to the information was declined... although they're now dealing with associated issues that might have been prevented had they applied appropriate mitigation before the problem was identified by regulators (this information was passed onto Austrac a few months ago by request). As is the case with most offshore leadgen services, this particular group shared an office with fraudsters engaged with typical gift card scams and other types of identify theft. We have often campaigned against unvetted and unscrupulous lead generation services, and their behaviour is having a seriously negative impact on legitimate businesses . If you can't operate ethically and legally, you shouldn't be operating at all, and if you do deliberately engage in nefarious practices, you should be prosecuted. Note: We will often meet with those brokers that engaged these types of services, and we'll play them the call that initiated the contact. The brokers are often unaware of the mechanics that delivered their 'lead', and they're usually unfamiliar with the consequence of their illegal funnel. Following through to the broker is usually the only reliable method of identifying the source of the leadgen service (most of the brokers will jump into our compliant programs). The videos in this article are indeed deception funnels, albeit with the starting point taking place via telephone.

There are several legal frameworks operating simultaneously as it relates to unsolicited contact:

- The credit licensing obligations under the National Consumer Credit Protection Act.

- The anti-hawking provisions applying to financial products.

- The Australian Privacy Principles regarding the use of personal information.

- The telemarketing rules under the Do Not Call Register legislation.

The position of unsolicited contact became considerably stricter following the anti-hawking reforms introduced through the Financial Sector Reform (Hayne Royal Commission Response) Act 2020, which took effect in 2021. These reforms prohibit the unsolicited selling of financial products and substantially tightened expectations around consumer consent.

Broker Growth: Our Broker Growth program includes a full session on advertising and marketing compliance. The program teaches you how to run your own advertising, with the first advert running at the end of the very first webinar. Results far exceed those that claim to provide an industry service. Interested? Call us for a discussion.

Anti-hawking - The Primary Legal Anchor

The core “cold contact” prohibition for 'financial products' generally sits in the anti-hawking regime in the Corporations Act 2001, specifically: Section 992A (and related provisions in Part 7.8A). However, the legislation is broadly correct in substance and not semantic implementation because it applies primarily to retail financial products. The legislation was significantly tightened following the Banking Royal Commission into Misconduct as it applied to the Banking, Superannuation and Financial Services Industry reforms, with the modern regime taking effect from 5 October 2021.

General prohibition, Corporations Act, 2001, Division 8 - Miscellaneous. Section 992A, Prohibition on hawking of financial products: (1) A person must not offer a financial product for issue or sale to another person (the consumer), or request or invite the consumer to ask or apply for a financial product or to purchase a financial product, if: (a) the consumer is a retail client; and (b) the offer, request or invitation is made in the course of, or because of, an unsolicited contact with the consumer.

Meaning of unsolicited contact, Corporations Act, 2001, Division 8 - Miscellaneous. Section 992A, Meaning of unsolicited contact: (4) Contact by a person with the consumer, in connection with a financial product, is unsolicited contact with the consumer in connection with the product if: (a) the contact is wholly or partly in one or more of the following forms: (i) a telephone call; (ii) a face‑to‑face meeting; (iii) any other real‑time interaction in the nature of a discussion or conversation; and (b) either: (i) the consumer did not consent to the contact; or (ii) if the consumer consented to the contact—the requirements of subsection (5) are not met.

The important distinction is this: Home loans themselves are credit products, not necessarily "financial products" regulated under the Corporations Act. So in mortgage land, there is no single equivalent of s992A that directly bans unsolicited real-time selling of home loans. Instead, the prohibition is functionally reconstructed across multiple regimes with behaviour and expectations directly implied.

Why aren't home loans 'Financial Products'?: Home loans are excluded from the Chapter 7 financial product regime by section 765A of the Corporations Act 2001. Specifically: 765A - Certain facilities are not financial products. The relevant provision is: 765A(1)(h) - "a credit facility within the meaning of the regulations is not a financial product".

However, the 'essence' of Section 992A - and when viewed through the lens of practical application and those that enforce conduct - means that you would have a hard time defending yourself against prosecution based on violating the broad prohibition in the Corporations Act. The application of the Act makes conceptual compliance sense because it correctly captures the policy logic of anti-hawking, which includes unsolicited real-time contact followed by product pitch or invitation without consumer consent, and this is the core prohibited behaviour pattern. That behavioural logic absolutely does map onto mortgages, even though the legal source differs.

Even without this directly stated contact prohibition, other Acts - and the direct influence of Best Interest Duty - provide clear guardrails on how telemarketing can be used.

While a residential mortgage is generally excluded from the definition of a financial product as a credit facility under section 765A of the Corporations Act, modern mortgage distribution frequently involves associated products such as deposit accounts, insurance products, and other financial facilities. To the extent that unsolicited contact results in the offering, recommendation, or invitation to acquire those products, the anti-hawking provisions in section 992A may become relevant notwithstanding that the underlying home loan itself remains outside the Chapter 7 financial product regime... although those that engage with the practice would sensibly argue that the dominant purpose of the contact was credit assistance, and this counterargument is probably the stronger legal position in most ordinary mortgage transactions. That said, you'd be foolish to test the increasingly blurred boundary between credit distribution and broader financial product distribution, particularly when broader legislation and industry guidance is considered to be quite definitive.

To summarise the overarching prohibition more succinctly, legislation effectively prohibits mortgage brokers from engaging in unsolicited cold calling for most new client acquisition. While the anti-hawking rules in section 992A of the Corporations Act 2001 (Cth) do not directly apply to standard credit products like home loans (due to their exclusion as 'financial products' under section 765A, and with the exclusion of some products such as Margin Loans), brokers must still comply with strict obligations under the National Consumer Credit Protection Act 2009. This includes the best interests duty and responsible lending requirements, and broader consumer protections.

RG234, The hawking prohibition: ASIC's document RG234 is for people who offer financial products for issue or sale. It sets out our guidance on the hawking provisions in s992A and 992AA of the Corporations Act. In particular, this guide explains how to comply with the hawking prohibition contained in s992A, a prohibition that aims to protect consumers from unsolicited offers of financial products.

The Regulatory Architecture of Cold Contact for Brokers

The concept of "cold calling" in mortgage origination is often mistakenly treated as a single legal question governed by a single statute. In reality, it is a fragmented regulatory construct, where permissibility is determined not by one prohibitive clause but by the interaction of four overlapping regimes. Each regime regulates a different dimension of the same behavioural act: initiating contact with a consumer for the purpose of influencing a credit decision.

Understanding why cold calling is effectively prohibited in most mortgage contexts requires unpacking the distinct legal logic of each framework and how they operate cumulatively rather than independently.

The Conceptual Boundary of “Unsolicited Credit Assistance”

Within the National Consumer Credit Protection Act 2009, there is no standalone provision that states mortgage brokers are prohibited from cold calling consumers. Instead, the Act constructs a behavioural boundary through the concept of unsolicited engagement in the credit assistance process, primarily located in Part 3-5A.

The NCCP regime is not designed as a telemarketing statute; it is a conduct and licensing framework. Its relevance to cold calling arises from the requirement that credit assistance be provided in a manner consistent with statutory obligations, including the best interests duty and obligations to ensure that recommendations are not shaped by inappropriate sales pressure or inducement structures.

The critical conceptual constraint is that credit assistance becomes legally sensitive when it is causally linked to unsolicited initiation by the provider. In other words, the Act does not say “do not call,” but it does regulate the downstream consequence of initiating credit assistance as a result of unsolicited contact. This is why the NCCP framework functions as a behavioural deterrent rather than a direct prohibition mechanism: it renders unsolicited origination commercially and legally unstable by attaching compliance consequences to the advisory outcome, not merely the communication itself.

Do Not Call Register, a Direct Telemarketing Prohibition

The operative prohibition on cold calling in the literal sense is found in the Do Not Call Register Act 2006. This is the primary legal instrument governing unsolicited telemarketing communications by telephone.

Unlike the NCCP Act, this regime is explicitly behavioural and procedural. It prohibits the making of unsolicited telemarketing calls to numbers listed on the Do Not Call Register, unless a statutory exemption applies. The legal test is not whether advice is appropriate or whether credit assistance standards are met, but whether the communication itself is an unsolicited commercial solicitation delivered by telephone to a protected number.

In mortgage contexts, this creates a structural prohibition on classic “cold calling” models where brokers purchase or compile lists of potential borrowers and initiate outbound calls without prior consent. Even where a number is not on the register, the broader regulatory expectation is that telemarketing must be consent-based, and compliance is further constrained by industry standards governing call timing, identification, and permitted calling practices.

The significance of this regime is that it regulates the medium itself. A mortgage broker cannot reframe telemarketing as “relationship building” to avoid its application; the legal trigger is the unsolicited commercial nature of the call, not the semantic framing of the conversation.

Privacy Act, The Constraint on Acquisition and Use of Data

The third layer of constraint arises from the Privacy Act 1988, which governs the collection, use, and disclosure of personal information used in marketing workflows, including lead generation lists derived from property inspections, enquiries, or third-party databases.

In the context of mortgage cold calling, the Privacy Act becomes critical at the point of data acquisition and secondary use. For example, inspection attendee lists obtained by a real estate agent are collected for a primary purpose: facilitating attendance and follow-up by the agent in relation to the property transaction. The subsequent use of that data by a mortgage broker introduces a secondary purpose, namely financial product marketing.

Unless the consumer has expressly consented to that secondary use and disclosure, the transfer of inspection data to a broker for the purpose of solicitation may breach privacy principles relating to use and disclosure. This is not merely an administrative concern; it directly undermines the legality of building outbound calling lists derived from property engagement activity.

Accordingly, even before a call is made, the regulatory system may already prohibit the creation of the call list itself, depending on the nature of consent obtained at the point of data collection. This is why modern property and finance referral ecosystems increasingly rely on explicit opt-in language rather than implied or inferred permission.

The Operational Rules Governing Call Conduct

The final layer of regulation is the Telecommunications (Telemarketing and Research Calls) Industry Standard 2017 under the Telecommunications Act 1997 Industry Standard (Telemarketing and Research Calls) 2017 framework. This instrument governs the operational mechanics of telemarketing calls, even where those calls are otherwise lawful under consent and privacy rules.

The Standard prescribes how calls must be conducted, including identification requirements, permitted calling hours, disclosure obligations, and restrictions on call behaviour. It applies to authorised telemarketing activity and assumes that consent or lawful authority already exists to initiate the call.

Its relevance to mortgage cold calling is that it removes any residual ambiguity about “informal” or semi-commercial calling practices. Even where a broker believes they are engaging in permissible outreach, the call must still comply with strict procedural standards. This includes ensuring the consumer is properly informed of the caller’s identity and the commercial purpose of the communication at the outset of the interaction.

The effect of this framework is to eliminate the viability of casual outbound mortgage solicitation. Telemarketing is not simply regulated in terms of outcome; it is regulated in terms of structure, disclosure, and timing.

Why Cold Calling is Functionally Prohibited

When the four regimes introduced earlier are read together, the legal position becomes clear even in the absence of a single explicit “ban on cold calling” clause.

The NCCP Act reframes unsolicited engagement as a compliance-sensitive pathway into credit advice, attaching consequences to credit assistance delivered as a result of unsolicited contact. The Do Not Call Register Act directly prohibits unsolicited telemarketing calls to protected consumers. The Privacy Act restricts the lawful acquisition and secondary use of the very datasets commonly used to construct cold calling lists. The Telecommunications Standard imposes procedural constraints that assume prior lawful consent and regulate the conduct of any permitted call.

The combined effect is not a prohibition in form but a prohibition in function. Cold calling as a business model for mortgage origination becomes legally unstable at every stage: data acquisition, contact initiation, communication execution, and advisory conversion. The regulatory system does not need to state explicitly that “mortgage cold calling is banned,” because each layer independently removes one of the essential conditions required for it to operate at scale in a compliant manner.

In practice, this produces a consent-centric distribution model, where permissible engagement arises from consumer initiation, explicit opt-in mechanisms, or pre-existing advisory relationships rather than outbound solicitation.

Does Section 155 on Harassment Play a Part?

Section 155 of the National Consumer Credit Protection Act 2009 is part of the general conduct provisions dealing with harassment in the context of credit activities. It provides that a credit provider or supplier must not harass a person in attempting to induce them to apply for credit or enter into a credit contract or related transaction.

This is materially different from telemarketing-specific prohibitions. Section 155 is not structured as a communications rule; it is a behavioural constraint on pressure-based conduct in the credit inducement process. The legal test is not whether contact was initiated by telephone, email, or in person, but whether the conduct rises to the level of “harassment” in attempting to procure credit entry.

Section 155, Harrassment: Section 155 is relevant to cold calling only in a secondary and escalation sense. It does not prohibit unsolicited contact itself, nor does it define telemarketing boundaries. Instead, it provides a civil and criminal sanction where credit-related inducement becomes harassing in nature. In a properly structured compliance analysis, it should be positioned as the behavioural enforcement backstop within credit inducement activities, rather than a primary source of prohibition on outbound calling.

Where Section 155 does play a part is when calls originate from offshore call centres that will relentlessly call you despite ongoing objections to the call. These organisations are often connected to lead generation companies that operate unethically and irresponsibly to coerce borrowers into a meeting on the basis of a fabricated interest rate.

Why Section 155 Is Not a Cold Calling Provision

Although section 155 can capture certain aggressive outbound calling practices, it does not prohibit cold calling per se. The critical distinction is that the provision requires a threshold of harassment, which implies persistent, coercive, or oppressive conduct rather than mere unsolicited contact. A single unsolicited call offering mortgage services would not automatically meet this threshold.

For section 155 to be engaged, the conduct typically needs to demonstrate a pattern such as repeated contact after refusal, high-pressure inducement, or behaviour that objectively crosses into intimidation or undue persistence in attempting to secure credit acceptance.

This is why section 155 operates as a backstop provision, not a primary telemarketing rule. It polices how far conduct can escalate once contact has occurred, rather than regulating the legitimacy of initiating contact itself.

Interaction With Cold Calling Practices

In the context of outbound mortgage solicitation, section 155 becomes relevant only at the point where cold calling shifts from marketing into pressure-based inducement. For example, a compliant but unsolicited call introducing mortgage services would more properly be analysed under the telemarketing regime in the Do Not Call Register Act 2006, the privacy constraints under the Privacy Act 1988, and the credit assistance conduct framework within the NCCP Act. However, if a broker or credit provider escalates from unsolicited outreach into repeated insistence, refusal avoidance, or persistent pressure to apply for credit, section 155 becomes engaged as a civil and criminal enforcement mechanism.

In this sense, it is not the “cold call” that triggers liability, but the behavioural intensity of the post-contact interaction.

How Section 155 Complements Telemarketing Rules

Section 155 operates alongside, rather than instead of, the telemarketing and unsolicited contact regimes. The Do Not Call and telecommunications framework governs whether the call can be made. Privacy law governs whether the contact data can be used. The NCCP unsolicited contact and conduct provisions govern whether credit assistance can be provided as a result of that engagement. Section 155 then sits at the final layer, regulating whether the manner of persuasion becomes unlawfully coercive.

In regulatory terms, it functions as a conduct severity threshold, not a communication permission rule.

Social Media and LinkedIn Direct Messaging

The migration of mortgage prospecting from the telephone to social media platforms has not altered the underlying regulatory concern. It has merely changed the medium through which unsolicited commercial influence is exercised. LinkedIn messages, Facebook direct messages, Instagram conversations and other private social communications represent, in many respects, the digital reincarnation of the traditional cold call. The fact that the consumer may read the message asynchronously does not fundamentally alter the fact that the communication originated not from consumer demand, but from intermediary initiative.

Modern financial regulation has increasingly shifted its focus away from the technical characteristics of communication channels and toward the behavioural circumstances in which financial influence is exerted. The Hayne Royal Commission repeatedly emphasised that the source of consumer detriment frequently lies not in the product itself, but in the distribution model through which that product is sold. From this perspective, an unsolicited LinkedIn message offering refinancing assistance differs from a cold telephone call only in the manner of delivery. In both cases, the intermediary identifies a prospective borrower, initiates the engagement, and attempts to create commercial demand where none had previously existed.

The psychological architecture of social media prospecting further compounds these concerns. Direct messaging platforms create a perception of personal relationship, social familiarity, and professional affinity. Consumers frequently interpret messages received through professional networks as carrying an implied endorsement or legitimacy that exceeds conventional advertising. The personalised nature of direct messaging therefore possesses a persuasive capacity that extends beyond passive marketing and moves toward individualised solicitation. Where the communication specifically references employment, property ownership, investment activity, or other personal characteristics gleaned from online profiles, the interaction begins to resemble targeted financial canvassing rather than general advertising.

Privacy principles also assume particular significance within social media environments. The collection, analysis and use of personal information obtained through social profiles for the purpose of identifying mortgage prospects may constitute a secondary use of information beyond the consumer's reasonable expectations. A consumer who establishes a professional networking profile does not necessarily anticipate that the information disclosed will be used to facilitate unsolicited approaches regarding credit products. Consequently, the legitimacy of the contact cannot be divorced from the legitimacy of the data acquisition process that enabled it.

Perhaps most importantly, unsolicited social media contact sits uneasily alongside the contemporary philosophy underpinning the best interests duty. The legislative intent of the mortgage reforms was to move the industry away from product distribution models driven by intermediary incentives and toward models driven by consumer need and consumer initiation. Direct messaging campaigns invert this relationship. Rather than responding to expressed demand, the intermediary manufactures demand through targeted outreach. The consumer becomes the object of a prospecting exercise rather than the initiator of a financial enquiry.

Accordingly, while Australian legislation does not presently contain an explicit prohibition on unsolicited social media messaging by mortgage brokers, the practice remains difficult to reconcile with the broader policy objectives of consent-based distribution, consumer autonomy, and best interests obligations. The absence of a specific prohibition should not be interpreted as regulatory endorsement. Rather, it reflects the reality that digital communication technologies have evolved more rapidly than the legislative frameworks designed to regulate them. In substance, the unsolicited mortgage direct message may differ little from the unsolicited telephone call that contemporary financial regulation has sought increasingly to discourage.

ASIC ratify their position by way of RG38 with the relevant passages relating to "real-time interaction in the nature of a conversation or discussion ", and these snippets are reproduced below.

RG 38.36: The hawking prohibition is technology neutral. This means that, in addition to telephone calls and face-to-face meetings, the hawking prohibition also extends to other real-time interactions that are in the nature of a discussion or conversation, including instant messages, as well as through media that use artificial intelligence such as chat-bots: see s992A(4)(a)(iii).

RG 38.37: The hawking prohibition cannot be circumvented by engaging a third party to make offers on a person’s behalf (as their representative or agent): see paragraph 5.31 of the Explanatory Memorandum. We consider that this includes where third parties are contracted to develop artificial intelligence sales tools, such as chat-bots. In such cases, the person commissioning the chat-bot’s use, or under whose licence it operates will be responsible for any offer, request or invitation made by the chat-bot.

RG 38.38: Real-time interactions are ones where the offeror and consumer respond to each other continuously in real time, or where an expectation exists that both parties will provide an immediate response to each other: see paragraph 5.59 of the Explanatory Memorandum. This includes both verbal and written communication. As a result, whether forms of contact, such as text messages, constitute real-time interactions for the purposes of s992A(4) depends on the circumstances. Some messages may create an expectation of an immediate response, while others may not.

These provisions have heavily guided the implementation of our BeNet AI which is capable of taking and receiving calls. We regularly advise clients that an AI phone call used for the purpose of following up on leads is tickling the thin green line that bilocates legal conduct and non-compliant practices, and it's for this reason we encourage that the first phone call to be made by a human, with general updates themselves delivered via AI (with human contact options).

The Open Home Register [ Property Enquiry to Financial Solicitation ]

The practice of contacting individuals whose details have been collected at property inspections presents one of the most misunderstood areas of modern mortgage prospecting. At first glance, the commercial logic appears compelling. A consumer has attended an open home, demonstrated an interest in purchasing property, and voluntarily supplied their personal details. To many, the subsequent introduction of mortgage services may appear not only reasonable, but commercially intuitive. Yet the regulatory and ethical considerations reveal a considerably more complex picture.

The central issue is not whether the consumer is likely to require finance. In most cases, they almost certainly will. The issue instead concerns the purpose for which the information was collected and the reasonable expectations of the individual providing it. An attendee who writes their name, telephone number and email address on an inspection register ordinarily does so to facilitate the administration of the property inspection, receive information regarding the property, or communicate with the selling agent. The relationship established at that moment is fundamentally one between the consumer and the real estate agency, not between the consumer and an unrelated credit intermediary.

From a privacy perspective, the distinction between primary and secondary purpose becomes particularly significant. The information supplied by the consumer was collected within a specific transactional context. The subsequent use of that information by a mortgage broker for the purpose of initiating unsolicited financial discussions may represent an entirely different commercial objective. Unless the consumer has been adequately informed and has expressly consented to such disclosure and subsequent contact, the use of inspection data for mortgage prospecting risks exceeding the reasonable expectations that existed when the information was originally collected,and this underlying consent is something our brokers and property partners understand and implement into their register practice.

Perhaps more importantly, the practice sits uneasily alongside the contemporary philosophy underpinning the best interests duty. The consumer has not sought financial assistance. They have not requested information regarding lending options. They have not initiated a discussion regarding borrowing capacity or credit requirements. The intermediary, rather than responding to expressed need, instead identifies the consumer as a prospective sales opportunity by virtue of their attendance at a property inspection. The relationship therefore begins not with advice, but with prospecting.

There is also an important psychological dimension to the open home environment itself. Property inspections frequently occur during periods of heightened emotional engagement. Prospective purchasers may be experiencing excitement, anxiety, uncertainty, financial stress, or competitive pressure. The consumer is evaluating one of the largest financial commitments of their lives. Introducing unsolicited credit discussions into this environment risks exploiting precisely those moments of emotional vulnerability that contemporary consumer protection frameworks seek to avoid.

The distinction between consent and assumption is therefore critical. A consumer's decision to inspect a property should not automatically be interpreted as an invitation to receive financial marketing. Interest in real estate does not necessarily constitute consent to discuss credit products, just as visiting a motor vehicle dealership does not inherently authorise unsolicited approaches from insurers, investment advisers or personal loan providers. The mere existence of a potential financial need cannot itself become the legal or ethical justification for initiating contact.

This does not mean that legitimate referral relationships cannot exist between real estate professionals and mortgage brokers. Where consumers are clearly informed that their details may be shared with finance partners, where genuine and informed consent is obtained, and where consumers actively elect to receive assistance, the relationship becomes fundamentally different. In such circumstances, the broker responds to a permission-based introduction rather than engaging in unsolicited solicitation. The consumer retains control over the engagement, and the intermediary operates within a framework of transparency and informed choice.

How to Make Referral Arrangements Compliant: An article titled "How to Make Referral Arrangements Compliant" introduces the complexity of the referral framework, and how brokers can ensure that appropriate adherence to legislation is maintained.

The Compliance Implications of Third Party Forms: In a slightly related article titled "The Compliance Implications of Third-Party Forms and Automatic Referrals" introduces the compliance issues associated with having auto/equipment/business, and other forms alongside residential lending, and when the automatic referral to another party becomes problematic.

Ultimately, the open home visitor register should not be viewed as a prospecting database waiting to be harvested, but as a collection of personal information entrusted for a particular purpose. The ethical broker recognises that the existence of a financing need does not itself create a right to initiate contact. The most sustainable opportunities arise not from identifying consumers who may require credit, but from creating environments in which consumers voluntarily seek assistance when they are ready to receive it.

Conclusion: Compliance as a Competitive Advantage

The modern mortgage industry stands at a remarkable inflection point. Never before have brokers possessed such extraordinary access to technology, consumer data, digital marketing platforms, referral ecosystems, automation tools, and scalable communication channels. The opportunities available to contemporary intermediaries are unprecedented. Yet the very abundance of these opportunities renders the persistence of cold-contact practices increasingly difficult to justify. Where prior generations of financial distribution may have relied upon interruption, intrusion, and unsolicited persuasion, the contemporary marketplace offers something infinitely more valuable: consent.

The regulatory architecture that now surrounds mortgage distribution should not be interpreted as an obstacle to commercial growth. Rather, it represents a deliberate attempt to elevate the profession beyond the transactional sales methodologies that historically undermined public confidence in financial services. The best interests duty, the responsible lending obligations, the privacy framework, and the emerging emphasis upon consumer-initiated engagement collectively establish a distribution model founded upon trust rather than pressure. They encourage brokers to become advisers, educators, advocates and strategic partners rather than product distributors seeking to manufacture demand.

In this respect, the best interests duty operates not merely as a legal obligation, but as a protective shield for the profession itself. It insulates ethical brokers from the competitive pressures created by aggressive prospecting models and discourages the race to the bottom that has historically characterised commission-driven sales environments. By requiring that the consumer's interests occupy the centre of the relationship, the duty simultaneously protects borrowers, elevates professional standards, and enhances the long-term reputation of the industry as a whole.

Importantly, compliance should never be viewed as the enemy of growth. The most successful mortgage businesses increasingly derive their opportunities not from interruption, but from attraction. Educational content, referral partnerships, consumer advocacy, social proof, digital communities, strategic alliances, first home buyer education, professional networking, and value-based marketing all create environments in which consumers actively seek assistance rather than resist it. These approaches produce stronger relationships, greater trust, higher conversion rates, improved retention, and more sustainable businesses.

Cold contact, by contrast, often reflects not innovation but desperation. It is a business model predicated upon the assumption that consumers must be pursued because insufficient value exists to attract them voluntarily. The intermediary who relies upon unsolicited approaches risks far more than regulatory scrutiny. They risk eroding trust, damaging reputation, alienating consumers, and undermining the very professional standing that the modern mortgage industry has worked so diligently to establish. In an era defined by transparency, consent and consumer empowerment, cold prospecting increasingly appears not merely outdated, but strategically self-destructive.

The future of mortgage distribution belongs to those who recognise that compliance is not a constraint upon opportunity, but its foundation. Ethical distribution models scale more effectively, retain clients more successfully, withstand regulatory scrutiny more comfortably, and generate businesses of enduring value. The industry's extraordinary growth over recent decades has been built not upon the ability to interrupt consumers, but upon the ability to serve them. The broker who embraces this philosophy discovers that the greatest commercial opportunities arise not despite compliance, but because of it.

Ultimately, the question is no longer whether mortgage businesses can survive without cold calling. The overwhelming evidence suggests that they can thrive without it. The more important question is whether any modern brokerage can afford the reputational, regulatory, and commercial risks associated with practices that increasingly belong to a previous era of financial distribution. In a profession built upon trust, the most valuable lead will always be the consumer who arrives willingly, engages voluntarily, and remains because the advice provided genuinely serves their interests.

in 1968. The branch was merged into ANZ in 1970, and the branch remains in the same location today as a 'Specialise Lending Hub. [ View Image ]

{kind=link}

{kind=link}

{kind=link}

{kind=link}