The advertising of mortgage interest rates occupies a unique position within consumer protection law. Unlike most forms of commercial advertising, the promotion of credit products is subject to an unusually prescriptive legislative framework that attempts to reconcile two competing realities. On one hand, consumers require simple and accessible indicators by which to compare competing mortgage products, and on the other, the true cost of credit is inherently multidimensional, incorporating not merely interest charges but also establishment fees, ongoing fees, discharge fees, package costs, offset account structures, redraw conditions, and numerous contingent expenses.

Not Legal Advice: Nothing in this article is legal advice of any kind. Legislation and Financial Marketing enjoy significant overlap, so this article deals with the legal position of general advertising. Seek your own independent legal advice for all financial marketing compliance matters.

The Deception Funnels in Financial Advertising: This article follows on from one titled "The Deception Funnels in Financial Advertising Used to Deceive Consumers Needs to Stop", and it's in a series of compliance related discussions. Another article deals with website footer compliance, and another scheduled article, titled "How We Multiplied the Results of Broker Grow Advertising by 10X" talks about the low-performing and nom-compliant programs delivered to market (so bad that we offered a 2 million 3X guarantee against their results). The latter article - supported by a large number of client videos - is published simply to distance our long-established Broker Growth program with somebody that is leveraging our product brand to deliver a far inferior product.

Rescue Program: Last year was defined by our Rescue Program: we triple results or give you a million dollars. This year we increased it to 2 million, and we're currently looking at a 5 million dollar program. The rescue program includes those that claim a specialty in the industry when their reality is defined by non-compliance, poor performance, AI video and graphics, and deceptive funnels. Rescue includes Bizleads, Broker Grow, Marketing Transformers, Sunbear, King Kong, wereU, and a number of others. One defining feature of all of those in Rescue is that they are not compliant solutions. As an example of how your own efforts can outperform any paid representation in minutes, read "How to Publish a High Yield First Home Buyer Advertisement in 10 Minutes".

The legislative response to this 'rate tension' was the creation of the comparison rate regime under the National Credit Code. The comparison rate was intended to function as a corrective mechanism against the behavioural tendency of consumers to focus exclusively upon headline interest rates. In psychological terms, legislators sought to counteract the cognitive bias known as anchoring, whereby consumers disproportionately weight the first numerical value encountered during decision making. The comparison rate regime therefore attempts to force advertisers to present a more comprehensive measure of borrowing cost alongside the headline rate.

The Foundational Prohibition: The Foundational Prohibition in financial advertising as defined in Consumer and Financial legislation is clear: "A person must not, in trade or commerce, engage in conduct that is misleading or deceptive or is likely to mislead or deceive". Competition and Consumer Act 2010 (Cth), Schedule 2, especially Section 18 - misleading or deceptive conduct, and Section 29 - false or misleading representations, and in the ASIC Act 2001 (Cth), particularly Section 12DA and Section 12DB prohibits the engagement in misleading conduct. Legally, the contravention occurs at the time the misleading representation is communicated, published, displayed, broadcast, or otherwise conveyed to consumers. In other words, the breach crystallises upon publication or exposure, and you cannot retrospectively erase the original contravention.

Despite the apparent simplicity of the legislative framework, widespread non-compliance remains observable throughout the mortgage broking industry. Some breaches are technical. Others are substantive. Others are deliberate. Many arise not from deliberate misconduct but from a profound misunderstanding of how legislation interacts with broader prohibitions against misleading and deceptive conduct.

APR, Comparison, and Quantitative Compliance Infractions are Ubiquitous: Of the 18000+ advertisements currenting run by over 3200 brokers (as of the date of publication), not a single advert published that includes a rate or other numeric or quantitative statement is compliant (outside our own compliant clients). Not one.

Compliance is one thing you can control, and technology should work for finance businesses. That's our focus. We focus on the results through broker education, and we build everything around us in terms of technology to support better commercial outcomes. Nobody else can say the same.

This article examines common aspects of rate advertising within the mortgage market and establishes a framework for best-practice compliance.

Infographic Advertising: You're going to see a number of 'infographic'-style advertising  in this article - a format we used for years until it was adopted by others (none of the linked ads are compliant, but we'll come to that later). First, usage of this format is created by AI in seconds so it is commonly used, but the information returned has to be property scrutinised for basic legislated compliance. Ogilvy's "The More You Tell, The More You Sell" (directed at copy - not creative) seems to have migrated to the creative field in the last few years, and this has given rise to a range of expressions we coined internally, such as "The More You Claim, The More You Must Explain" and "The More You Quantify, The More You Must Justify". Infographics are based on larger amounts of information, so ensure you don't tickle the thin green line. Second, because infographics play a larger industry role - especially in advertising - we've created a free 'Finance Infographic Generator' with results returned, or a series of prompts for various engines in JSON format.

in this article - a format we used for years until it was adopted by others (none of the linked ads are compliant, but we'll come to that later). First, usage of this format is created by AI in seconds so it is commonly used, but the information returned has to be property scrutinised for basic legislated compliance. Ogilvy's "The More You Tell, The More You Sell" (directed at copy - not creative) seems to have migrated to the creative field in the last few years, and this has given rise to a range of expressions we coined internally, such as "The More You Claim, The More You Must Explain" and "The More You Quantify, The More You Must Justify". Infographics are based on larger amounts of information, so ensure you don't tickle the thin green line. Second, because infographics play a larger industry role - especially in advertising - we've created a free 'Finance Infographic Generator' with results returned, or a series of prompts for various engines in JSON format.

You Will See Changes: We're quite public with our criticism of the quality of advertising, and each time we record reviews or publish information you'll see a scurry of activity as those that follow our lead try desperately to catch up - all of which we heavily document. To those agencies that are delivering a known mediocre experience to brokers - which includes anyone using High Levell or Calendly - we suggest you find yourself an industry that doesn't require a regulated experience. We and other great agencies we deal with every day outperform you with creative, conversions, and tech, so consider vacating the industry and allow brokers to engage with an experience that is free from the technical debt that defines your 'product'. Let mortgage brokers engage with a compliant experience that'll deliver them better results.

A Note on the Example Screenshots

The examples contained throughout this article are not published for the purpose of ridicule, humiliation, or public shaming. The overwhelming majority of brokers and financial professionals genuinely want to operate ethically and in the best interests of consumers, yet many are unknowingly exposed to significant compliance risk through shonky marketing advice, flawed advertising systems, templated lead-generation funnels, or clueless third-party agencies that prioritise conversion metrics over regulatory integrity. The purpose of this analysis is therefore educational rather than punitive. By examining real-world advertising practices in their unedited form, it becomes possible to illustrate how misleading impressions are actually created in practice, how regulators are likely to interpret those experiences, and where seemingly minor wording or design decisions can produce substantial legal consequences under Australian consumer and financial services law.

Importantly, many of the issues identified in this article arise not from deliberate dishonesty, but from a broader industry culture in which behavioural manipulation, exaggerated savings claims, artificial urgency, fake personalisation, fabricated testimonials, and misleading “AI-powered” experiences have become increasingly normalised within digital marketing ecosystems. Over time, these practices can begin to appear commercially acceptable simply because they are widespread. The fact that a particular tactic is commonly used, however, does not make it compliant. Financial services operate within one of the most heavily regulated advertising environments in Australia precisely because consumers are making decisions involving large financial commitments, information asymmetry, and long-term economic consequences. Compliance therefore cannot be treated as a superficial legal formality appended after the marketing process - it must form part of the architecture of the consumer experience itself.

If your advertisement, landing page, or funnel appears within this article, we invite you to view that inclusion not as criticism, but as an opportunity to strengthen both your compliance position and your commercial performance. Any broker featured in this analysis will receive a 25% discount on our Broker Growth program. The reason for that offer is simple: the overwhelming majority of the issues identified throughout this article were entirely avoidable, and your conversions were compromised by poor ads and offensive technology. More importantly, many of these same practices are not merely compliance liabilities - they are commercially inefficient. Misleading funnels of any type and weak disclosure structures frequently damage long-term trust, reduce conversion quality, increase consumer scepticism, and ultimately produce lower-value relationships. Ethical and transparent marketing is not merely safer - it performs better.

Our framework is built upon a fundamentally different philosophy: genuine value creation through truthful representation, transparent communication, psychologically intelligent user experience design, and the delivery of real, visible consumer outcomes. Rather than manufacturing the illusion of analysis, savings, or personalisation, we believe financial marketing should substantively deliver what it promises. In our experience, when brokers operate with a higher standard of honesty, clarity, and disclosure from the very beginning of the customer journey, consumers respond with greater trust, stronger engagement, improved lead quality, and higher long-term conversion performance. The objective is not merely to avoid regulatory scrutiny but it is used to build a business capable of sustaining public confidence in an industry where trust has become one of the most commercially valuable assets of all.

Insights API: Insights records every single advertisement from every single broker in the country every single day. What has resulted is the most complete archive of broker advertising in existence. AI integration reads text from images, measures the advert in its entirety against our compliance benchmarks, and assigns a score based on compliance, sentiment commonality (and copy overlap), and effectiveness. The API itself is available to those that are required to provide advertising oversight.

Rates & Numbers Play a Valuable Role in Marketing

There has emerged a somewhat simplistic tendency to equate any consumer-facing use of interest rates with “rate-driven” broking or reductive financial marketing. Such a characterisation fails to recognise both the behavioural realities of consumer decision-making and the legitimate informational role that rates continue to play within the borrowing process. Interest rates are not merely marketing devices imposed upon reluctant consumers by the finance industry; they are among the primary variables through which consumers themselves conceptualise and compare lending products. Extensive behavioural and market research consistently demonstrates that borrowers regard rate as the single most influential product attribute when initially evaluating finance options, often assigning it substantially greater importance than secondary considerations such as product flexibility, structural features or ancillary benefits. To entirely ignore rates within consumer communication would therefore not represent sophistication or ethical restraint, but rather a failure to engage consumers through the financial language they most readily recognise and understand.

This behavioural reality is reinforced by the broader media and economic environment within which consumers form their financial perceptions. Public discourse surrounding mortgages is overwhelmingly rate-centric. RBA announcements, monetary policy commentary, mainstream news coverage and comparison platforms routinely frame the mortgage market through the lens of percentage movements, pricing cycles and repayment impacts. Consumers are therefore conditioned to interpret lending products initially through numerical pricing signals, even where those signals may ultimately represent only one component of a far more complex borrowing decision. In this sense, the use of rates within advertising functions not merely as promotion, but as a form of communicative alignment with the vocabulary already dominating public financial consciousness. Rates provide an accessible cognitive entry point through which consumers begin engaging with otherwise highly technical financial products.

Importantly, the ethical use of rates does not require that rates become the sole or dominant basis upon which lending recommendations are ultimately made. There is a fundamental distinction between using rates as an initial engagement mechanism and constructing an entire advisory framework around simplistic price competition. A consumer may first respond to an advertisement because of a rate representation, yet the subsequent advisory process may appropriately expand the discussion toward loan structure, repayment flexibility, offset functionality, cash-flow management, investment strategy, risk tolerance, long-term financial objectives and broader suitability considerations. In practice, sophisticated consumer engagement often involves precisely this progression: the rate captures attention because it aligns with the consumer's existing financial frame of reference, while the advisory conversation itself introduces the deeper structural and strategic considerations necessary for informed decision-making.

The regulatory framework itself implicitly recognises the legitimacy of rate-based advertising, provided that such representations are used transparently, accurately and in conjunction with the disclosures necessary to contextualise them appropriately. The National Credit Code does not prohibit the advertisement of rates; rather, it regulates the manner in which rates are presented so as to minimise the risk of consumers forming misleading impressions regarding cost, availability or suitability. Similarly, ASIC's Regulatory Guide 234 does not advocate for the elimination of pricing representations from financial advertising. Instead, it emphasises balance, substantiation and the avoidance of selective emphasis that distorts consumer understanding. Ethical rate advertising therefore does not involve abandoning rates altogether, but using them within a disclosure framework that respects both consumer psychology and consumer protection principles.

Accordingly, the mere presence of rates within advertising should not be mistaken for evidence of a “rate-driven” philosophy. To the contrary, refusing to acknowledge the persuasive and informational power of rates may itself represent a failure to appreciate how consumers actually navigate financial decision-making. Effective and ethical advertising does not ignore consumer behaviour; it recognises it, engages with it transparently, and then responsibly broadens the conversation beyond the initial numerical trigger. When used with appropriate disclosures, contextual explanations and a genuinely client-focused advisory process, rates can serve as a legitimate and highly effective gateway into more sophisticated financial discussions rather than as an endpoint in themselves.

From a practical perspective, this approach is also reflected in our own commercial outcomes. Ethical engagement frameworks that responsibly utilise rate-based messaging while subsequently educating consumers on broader structural considerations consistently demonstrate strong engagement and conversion performance because they align persuasive communication with informed advisory conduct rather than placing the two in opposition. The objective is not to manipulate consumers through isolated numerical representations, but to use familiar financial reference points as the beginning of a more comprehensive and strategically informed lending conversation. In this sense, properly contextualised rate advertising does not undermine ethical finance practice; it facilitates consumer engagement with it.

We Use Lender Data Everywhere: We use lender and rate data in a large number of locations, from our website framework and comparison engine (and Comparison API) through to placeholders in email autoresponders. When rates are a language and metric that borrowers understand and consider more important than any other mortgage attribute, we ensure that we communicate using a shared and common language. We support this data with large amounts of information and video. It's in the discussion you have with clients that you educate them on structure, capacity, eligibility, serviceability, and other big-picture considerations.

The Legislative Purpose of Comparison Rates

The National Credit Code requires comparison rates because legislators recognised a fundamental economic reality: interest rates alone rarely communicate the "true cost of borrowing".

ASIC explains that comparison rates are intended to incorporate interest charges, most fees and charges, the term, and a standardised calculation methodology, thereby allowing consumers to make more informed comparisons between competing credit products. The policy objective is therefore not merely disclosure. It is behavioural intervention. The comparison rate regime seeks to mitigate anchoring bias, framing effects, salience bias, presentational distortion, and information asymmetry. From a consumer psychology perspective, comparison rates represent one of Australia's earliest attempts to use disclosure law as a form of behavioural regulation.

The True Cost of Credit or Borrowing: Although neither the National Credit Code nor the National Consumer Credit Protection Regulations expressly employ the phrase "true cost of credit", the comparison-rate regime is founded upon that underlying concept. The legislative scheme proceeds from the recognition that an annual percentage rate represents only one component of a borrower's financial obligation and may therefore provide an incomplete basis for product comparison. By requiring the disclosure of a comparison rate whenever an annual percentage rate is advertised, Parliament has effectively acknowledged that the economic cost of credit extends beyond interest charges alone. The comparison rate serves as a statutory approximation of that broader cost, incorporating prescribed fees and charges into a standardised disclosure intended to provide consumers with a more accurate understanding of the financial consequences of borrowing. When read alongside the prohibitions against misleading or deceptive conduct contained in the ASIC Act and Australian Consumer Law, the comparison-rate provisions reveal a clear legislative objective: consumers should not merely be informed of the interest payable under a credit contract, but should be placed in a position to understand, as accurately as reasonably practicable, the overall cost implications of the credit being offered. In short, the comparison rate requires disclosures that includes the interest rate, and the rate itself triggers comparison obligations - that's the interpretation established by law, and brokers should never lean on rates or "rate bait" in order to unduly coerce a conversion of any type.

When Must a Comparison Rate Be Displayed?

The most misunderstood provision in Australian credit advertising is Section 160 of the National Credit Code. Section 160(1) states that "[a] credit advertisement must contain the relevant comparison rate in accordance with this Part if it contains an annual percentage rate" (and, discussed shortly, if the repayment amount is stated in the advertisement). The practical consequence is profound. If an advertisement contains any numeric rate figure, such as 5.49%, 5.84% p.a. variable rate 5.69%, fixed rate 5.39%, rates between 5.69% and 6.02%, or any other annual percentage rate representation, the comparison rate is required as prescribed in legislation.

Many marketers and brokers incorrectly assume that the obligation arises only for lenders. The legislation instead focuses upon publication of the advertisement itself. Mortgage brokers are therefore not exempt merely because they are intermediaries.

An equally important, yet frequently overlooked, aspect of the comparison rate regime is that the legislative obligation operates asymmetrically. Section 160 of the National Credit Code creates a one-way trigger: the publication of an annual percentage rate compels the inclusion of a comparison rate... but the converse is not expressly mandated. That is, the legislation does not state that the publication of a comparison rate automatically requires the publication of the corresponding interest rate. This distinction has occasionally led some advertisers to conclude that a comparison rate may be presented in isolation as a means of avoiding the broader compliance obligations associated with rate advertising. Such an interpretation is inconsistent with both the purpose and structure of the legislation - the exclusion does not represent the 'true cost of credit', so usage of the comparison rate subsequently requires an Annual Percentage Rate (APR).

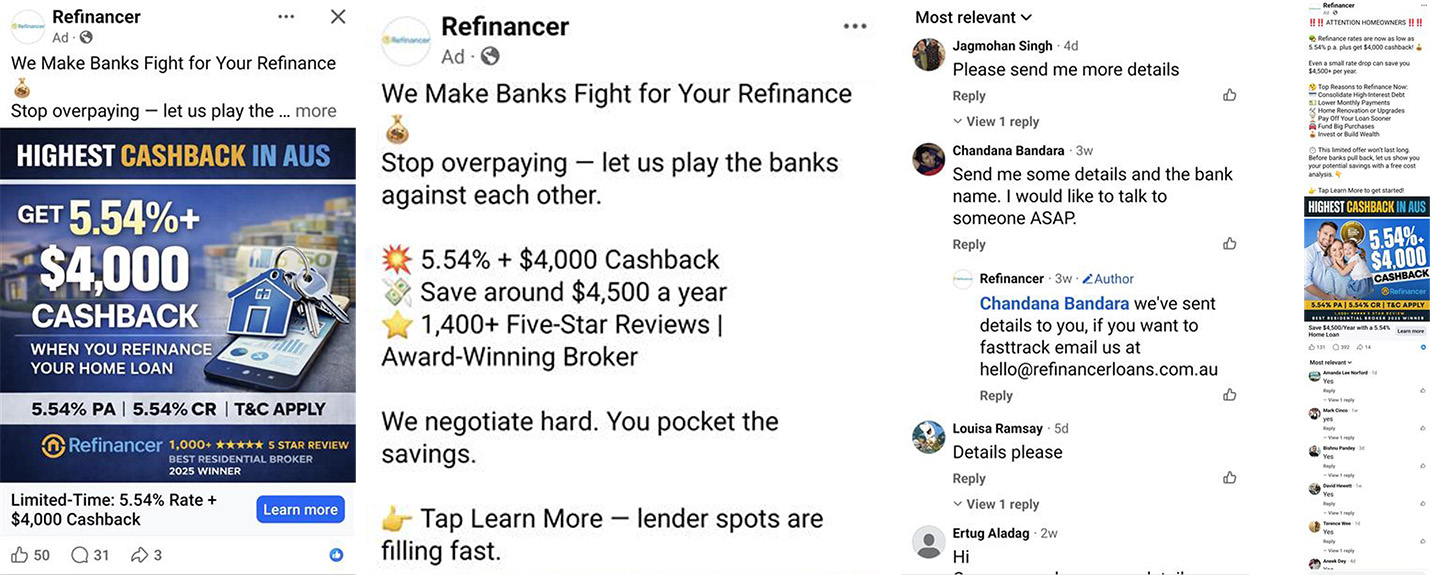

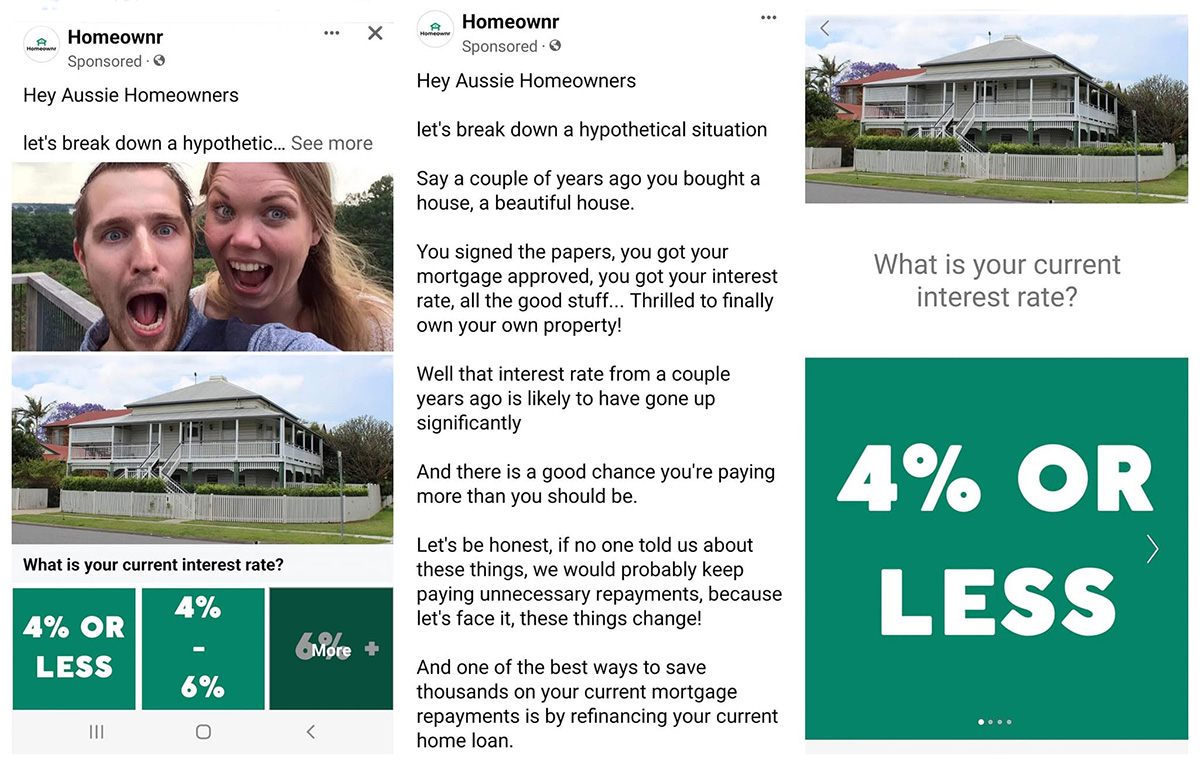

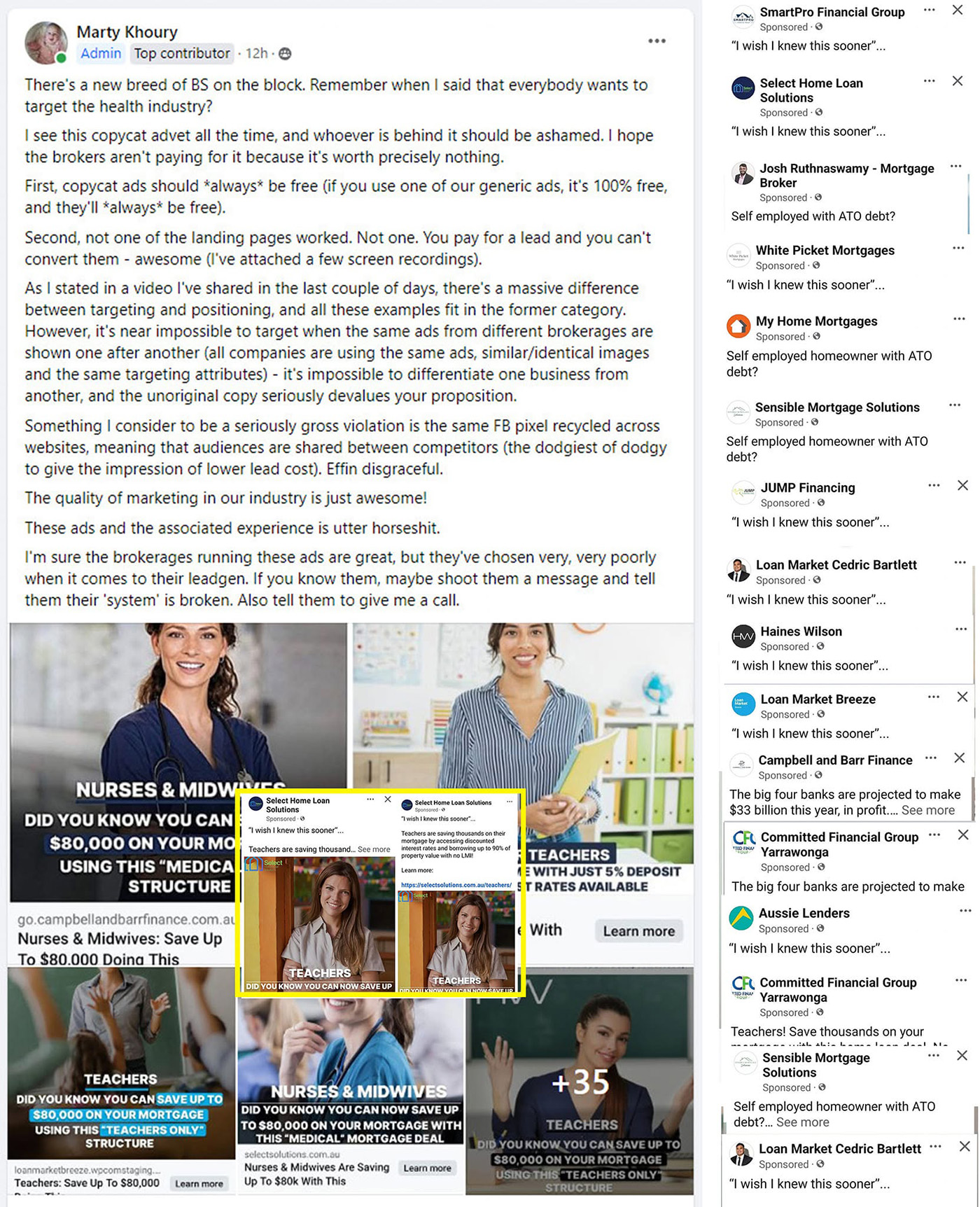

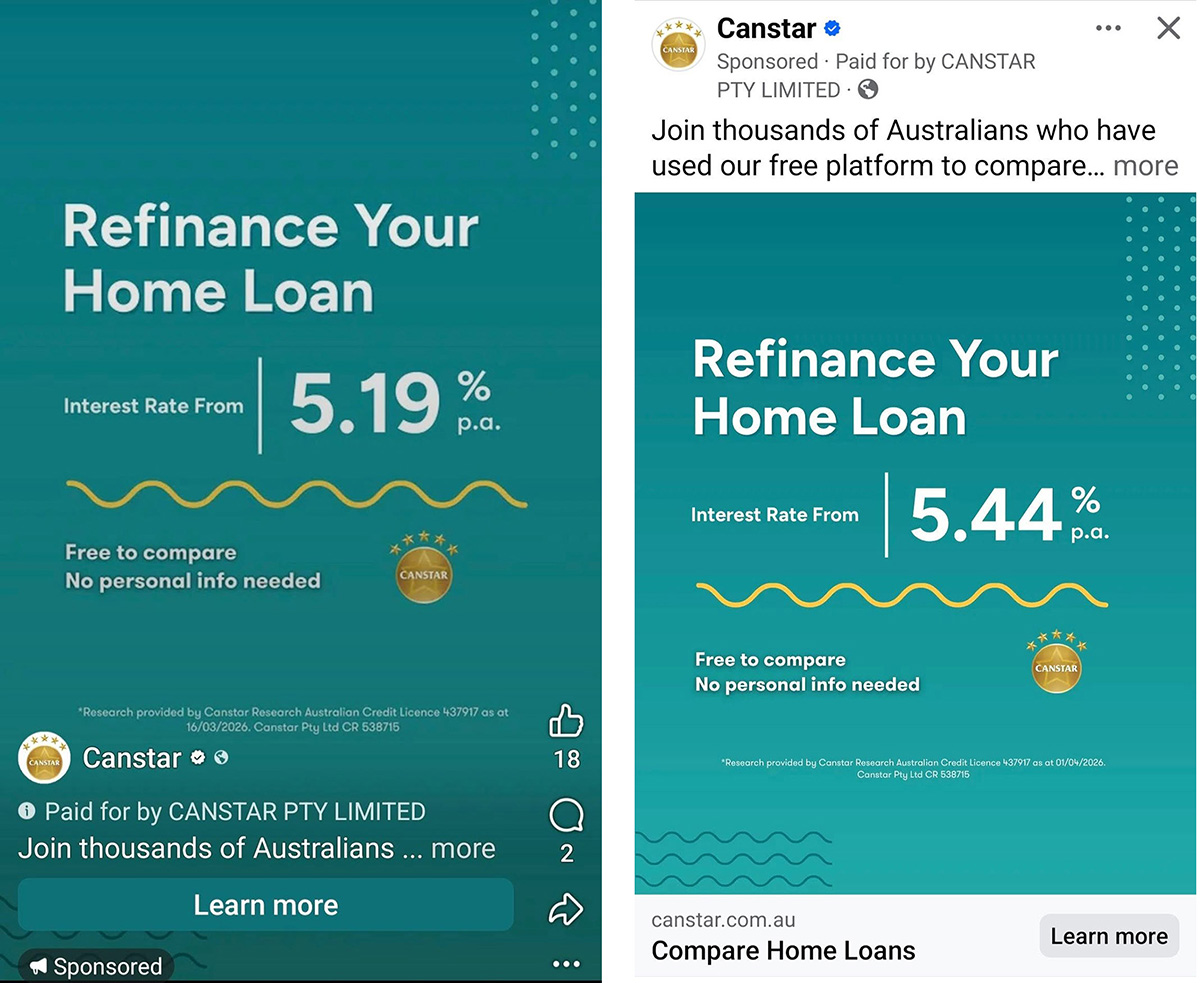

Pictured: The advertisements above were chosen in a pool of several thousand simply because they were shown in the few hours before this article was published - so they're current. None are compliant, and a few of them - such as Refinancier - is of particular concern because of the clear deception funnel that follows (they're also not responding to requests for the lender - required in the missing disclaimer - as a matter of choice, and this breach is discussed shortly).

The comparison rate was never intended to function as a standalone representation of credit pricing. Rather, it was introduced as a supplementary disclosure mechanism designed to provide consumers with a more complete understanding of borrowing costs than could be achieved through the publication of an annual percentage rate alone. Section 160 operates on the assumption that consumers will ordinarily encounter both figures together, allowing them to understand not merely the nominal interest component of a loan, but also the extent to which fees and charges influence the overall (shorter-term) cost of credit. To present a comparison rate in isolation deprives consumers of the very contextual information that the comparison rate was designed to supplement.

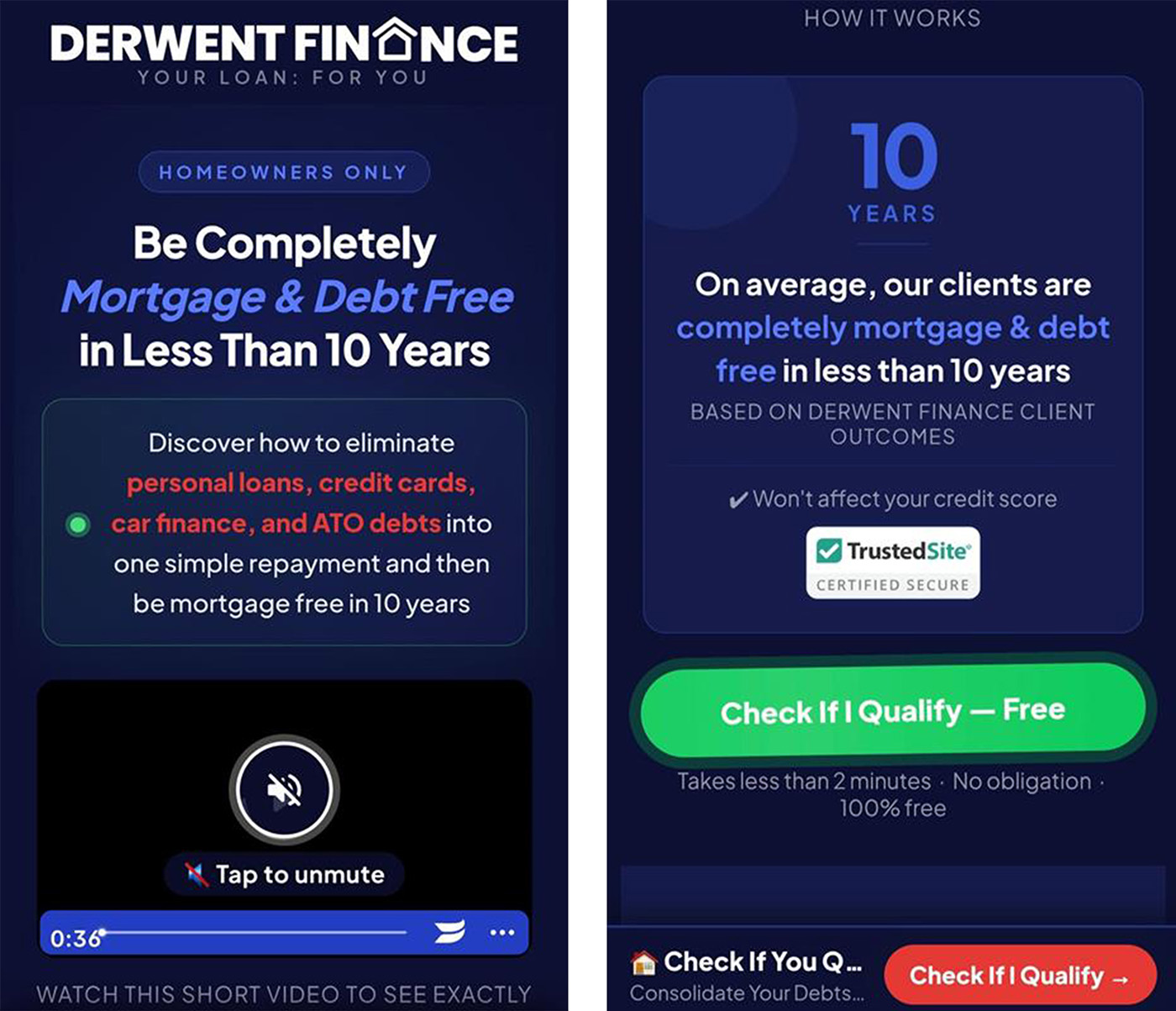

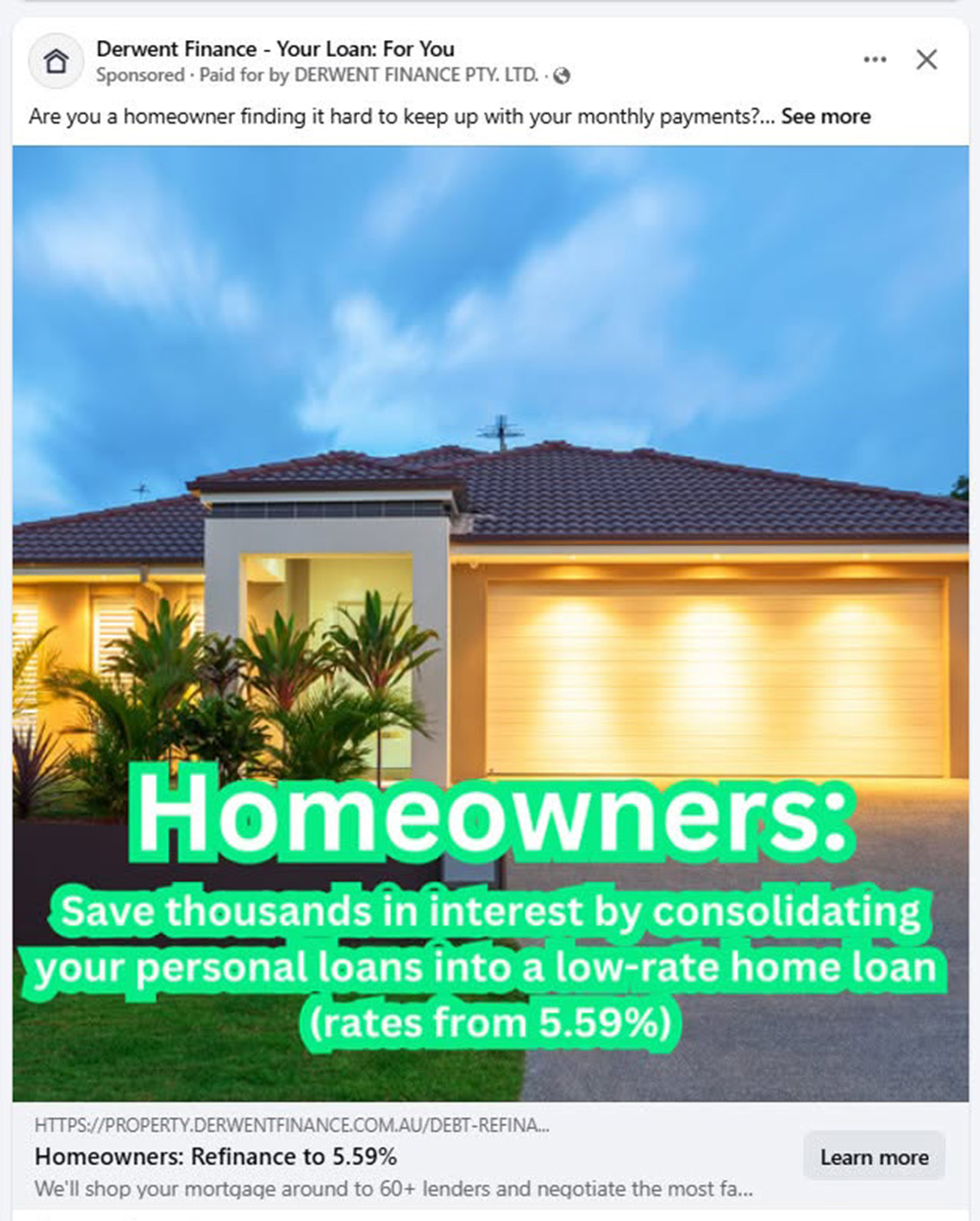

Pictured: This advertisement was indiscriminately selected from a pool of thousands. The "Rate as Low as" is an issue we discuss shortly, but the arbitrary and nonsensical figure doesn't absolve you of legislated compliance sins. The comparison is required, as is the warning, term, conditions, fees, lender, and other disclosures. The issue is compounded by the quantitative "Save $300 a month" statement which also requires full qualification and substantive and accurately resolved statements. If this advert were a horse, you'd shoot it. Sadly, most digital representation is flawed or downright illegal, and this is evident by the fact that no advert outside our own client base that discloses numeric values is presented in a compliant manner - not one.

This principle becomes particularly apparent when the broader legislative framework is considered. Section 163 of the National Credit Code requires that a comparison rate be accompanied by the prescribed warning, while Section 164 imposes strict requirements regarding the prominence and presentation of comparison rates. Most significantly, the prescribed warning itself acknowledges the inherent limitations of comparison rates, stating that different amounts and terms will result in different comparison rates and that certain costs, including redraw fees and early repayment fees, are not included in the calculation. Legislators therefore recognised that a comparison rate is not, and was never intended to be, a complete representation of the cost of credit. It is merely one component of a broader disclosure framework, so the comparison in isolation - established through case law - is used as a measure against tiers of products when early rate disclosure information was provided. What it is not is a licence to print one (often misleading) figure in isolation of broader cost-disclosure requirements as dictated by legislation.

Pictured: With the exception of Fig Financial, the pictured examples have failed to provide the legally mandated comparison rate. National Consumer Credit Protection Act 2009 states very clearly in s164(a) that "[a] credit advertisement must contain the relevant comparison rate in accordance with this Part if it contains an annual percentage rate", and section 161 states that "The relevant comparison rate for the purposes of section 160 is the comparison rate calculated for whichever of the designated amounts and terms most closely represents the typical amount of credit and term initially provided by the credit provider for the consumer credit product being advertised". Among an array of other requirements, section 163(1) states that "A comparison rate in a credit advertisement must be accompanied by a warning about the accuracy of the comparison rate that is prescribed by a regulation". It's not rocket science. The two figures should be considered as Jerey Lewis and Dean Martin, Abbot and Costello, Ying and Yang, burgers and fries - inseparable and joined at the hip. You can't have one without the other. In many cases, the comparison rate is excluded as a means to intentionally deceive the borrower, and these cases are discussed in the article on the 'Deception Funnel'. Fig Finance includes the comparison rate in the primary creative but fails to include it in the copy, and the comparison warning is missing (as it is in all examples), and this is discussed in the next section.

From both a legal and behavioural perspective, the interest rate and comparison rate should therefore be regarded as inseparable disclosures. One communicates the contractual rate at which interest accrues, while the other communicates a legislatively standardised estimate of the broader cost of borrowing. Each figure derives meaning from the presence of the other. An interest rate without a comparison rate understates, misrepresents, and often hides the true cost of credit. Conversely, a comparison rate without the corresponding interest rate obscures the fundamental pricing structure of the mortgage product itself. The consumer is left with a numerical figure that appears authoritative yet lacks the contextual benchmark necessary for meaningful comparison.

Advertising Comments: You will be called out on your bullshit. While the Simpli Finance efforts might be explained by a DIY oversight or incompetent marketing representation, the illegal Mortgage Magnet message is entirely deliberate and cannot be explained by ignorance - he knows what he's doing. John Kennedy from Tide Financial - the charlatan behind Mortgage Magnet - was a former broker (albeit, not very successful), and his representation in the advertising space has adversely impacted all those that conduct themselves ethically, responsibly, and in the best interests of the consumer, and those consumers that were presented with his advertisements were objectively exposed to broad deception. It's hard to see any broker that buys his leads as anything other than somebody supporting organised crime. Rock My Mortgage has gone a little dark lately but may have emerged as another name to escape past sins (as Broker Grow did with the legion of upset brokers at Karbn), but the brand as it existed was a minefield of compliance issues with the legal framework and honesty seemingly overlooked and ignored on the basis that "dishonesty performs better". We commented on a Mortgage Magnet advert back in 2021 and invited John to our long-stating challenge - he declined (as did John Maxwell from UpTick Marketing - he publicly accepted and privately declined). Don't buy leads!

Pictured: Under previous management, the Joust platform was a fraudulent deceptive lie - both in terms of its consumer-facing advertising and the service provided to brokers. Apart from the clear issues associated with rate misrepresentation and quantification malfeasance, the notion that lenders would 'compete' for submitted deals was absurd, and customers quickly caught onto the lie. For brokers, leads were double-handled, washed against duplicate databases, and of poor quality. They insulted financial legislation but also violated basic Australian Consumer Law expectations in other ways. It's a shame: they could have leveraged decent technology and established the brand in a way that supported borrowers through education and an enhanced service. Certainly, their marketing team - supported by a gentleman by the name of John Maxwell (now selling leads under another brand) - was largely responsible for the brand's demise. The whole platform was a compliance abomination.

This interpretation is further reinforced by the overarching prohibitions against misleading or deceptive conduct contained in section 12DA of the ASIC Act and section 18 of the Australian Consumer Law. The legal test is not whether a disclosure can be defended in isolation, but whether the overall impression conveyed to an ordinary and reasonable consumer is accurate. Where a comparison rate is presented without the accompanying interest rate - an action that is well-established to be a method to mitigate true cost disclosure - there is a substantial risk that consumers may be misled as to the composition of that figure, the assumptions underlying its calculation, or the relationship between interest charges and other borrowing costs. Such an outcome would be fundamentally inconsistent with the consumer-protection objectives that underpin the comparison rate regime.

Pictured: Those lead generation companies that flog off Facebook leads aren't interested in honesty, transparent, ethical conduct, or the legal framework that underpins industry efforts. They're interested in one thing: low-cost leads. And they'll use whatever methods are necessary in order to deliberately bait potential borrowers into a subscription. Your association with these groups is a compliance breach by association - you're breaking the law. No lead generation advertisement has ever introduced the required comparison warnings, disclosures, warnings and relevant information. Not ever.

Pictured: None of the pictured advertisements meet the legal standard. Quite often, the cashback shown is not one associated with the product, and the cashback itself should be disclosed with information to support your claims. The use of disclaimers enhances the experiences and ratifies eligibility. The advertisement from Australian Mortgage Finance Solutions includes the comparison rate in a manner that is specifically regulated against, and they - along with all the other ads - exclude the required disclaimers, warnings, and information. Joel Fitzgerald's should be commended for the DIY effort, but it isn't compliant. Further, Joel returns a masup of non-compliant rates that don't match. Use of rates in video is introduced shortly (disclaimers not present)

In practical terms, compliance professionals should approach the interest rate and comparison rate as a legislatively married pair. While the National Credit Code expressly requires the comparison rate when an annual percentage rate is advertised, the broader purpose of the regime is to ensure that consumers are provided with a balanced and accurate representation of the true cost of credit. Best established legal practice therefore dictates that whenever one figure is displayed, the other should ordinarily accompany it, together with the prescribed warning and all associated disclosures. The objective is not merely technical compliance with the wording of section 160, but faithful, dutiful, transparent, honest, and ethical compliance with the legislative intent, thus enabling consumers to understand the real economic cost of borrowing before making a credit decision, or the decision to interact with an advertisement.

Note: The comparison rate cannot be arbitrarily selected. Section 161 requires the comparison rate to be calculated using the designated amount and term most closely representing the typical credit product being advertised. This requirement prevents advertisers from selectively choosing loan scenarios that artificially improve outcomes. The comparison rate must correspond to the legislatively prescribed methodology.

Mandatory Information Accompanying the Comparison Rate

Section 162 requires the advertisement to clearly states the product name, credit amount, loan term, and whether the loan is secured or unsecured where applicable. Failure to provide this contextual information will render the comparison rate misleading because consumers cannot understand the assumptions underpinning the calculation.

The legislation does not expressly state that the lender's name must appear alongside every comparison rate. However, in many advertising contexts, the lender identity forms part of the "product name" required by section 162 and is necessary to prevent the advertisement from becoming misleading.

The contextual information required by section 162 serves a purpose far broader than mere technical disclosure. Legislators recognised that a comparison rate is not a self-explanatory figure. It derives its meaning from the assumptions upon which it is calculated, including the loan amount, loan term and the particular credit product to which it relates. A comparison rate without context is little more than a number. The legislative requirement to disclose the product details therefore exists to ensure that consumers can identify precisely what is being compared and whether that comparison is relevant to their own circumstances.

Pictured: The comparison rate triggers the comparison rate and full comparison warnings, and the comparison rate triggers the full product disclosure - including the term, rate, comparison rate, product, and other information. It isn't hard.

In practice, this necessarily raises the question of product identification. A mortgage product does not exist in isolation. Every credit product is offered by a particular credit provider operating under its own credit policies, servicing standards, fee structures, eligibility criteria, offset arrangements, redraw conditions and pricing methodology. Two products carrying identical interest rates and identical comparison rates may nevertheless represent materially different consumer propositions. The identity of the lender is therefore not merely a branding exercise - it is an integral component of understanding the nature of the credit product itself.

Pictured: Warning and disclosures add validity and a measure of quality assurance to your business and operation. You'll stand out from the lead generation crowd, and your transparent communications and overt honesty legitimises your operation and forms part of your customer experience. If you need to intentionally advertise on rate in isolation as some sort of bait mechanism without legal disclosures, then you probably shouldn't be a broker.

Although section 162 refers to the "product" rather than the "lender", there are well-established legal arguments and precedent stating in clear terms that a consumer cannot meaningfully identify a product unless the credit provider or lender is also identifiable. The purpose of the provision is to ensure that consumers understand the assumptions underpinning the comparison rate. That purpose is substantially undermined where a comparison rate is advertised without allowing consumers to determine which lender's product is being represented. The practical effect is that consumers are deprived of information necessary to conduct further enquiries, compare alternative products, review credit policies or assess the suitability of the loan being advertised.

The significance of lender identification becomes even more apparent when viewed through the lens of misleading and deceptive conduct. The question under section 12DA of the ASIC Act is not whether individual statements are technically accurate, but whether the overall impression conveyed to an ordinary and reasonable consumer is misleading. An advertisement that prominently displays an attractive interest rate and comparison rate while omitting the identity of the underlying lender may create an information deficit that materially affects a consumer's ability to evaluate the offer, and this is evident by way of the examples below. In some circumstances, the omission of the lender may itself become a material omission capable of misleading consumers by preventing them from understanding the true nature of the product being promoted.

This issue of the legislated product information - and by association, lender name - is particularly relevant in digital and social media advertising. Where consumers respond to an advertisement by asking, "Which lender is this?", the question itself provides clear and indisputable evidence that the advertisement has failed to adequately communicate information that consumers consider necessary to understand the offer. That question asked will indicate that the advertisement has not successfully conveyed the contextual information required for informed consumer decision-making.

Rate of the Week: The Rate of the Week advertisement is a minefield of compliance issues. The screenshots were taken on the 8th of June 2026 at 8.16pm and likely refers to Bendigo Bank's old 'Complete Home Loan' (low LVR and discounted Owner Occupier, Principal & Interest, 2-year fixed rate), but the exact reference isn't known because it wasn't disclosed - we sourced the data from our Comparison Engine archive and this was the only match. It's possible that the rate is a siloed unpublished or green rate... and the fact we couldn't find it illustrates the problem. The rate is used in multiple locations without a comparison rate, the messaging is ambiguous, and the cashback quantification isn't defined. This is both a deception funnel and rate bait and its finest.

The Rate of the Week Rate Bait outwardly appears a little dubious and opens up a can of worms relating to rate accessibility, currency, and the promotion of rates that are inaccessible to most borrowers - such as professional, discounted, promotional, or green products - all of which we'll look at shortly.

Which Bank?: From a behavioural perspective, the questions asked under or alongside an advertisement are unsurprising. Consumers process mortgage advertisements using heuristic shortcuts. The headline rate attracts attention, while contextual disclosures receive significantly less cognitive focus. If a material proportion of consumers are unable to identify the lender after viewing the advertisement, it raises legitimate questions regarding whether the product disclosure has achieved its intended purpose. The fact that consumers are actively seeking fundamental identifying information suggests that the information may not have been presented with sufficient prominence or clarity.

Refinancier Rate Bait & Compliance Abomination: I'm quite comfortable calling our Refinancier because I've called him out for years - there's little chance he'll call us for any help. This is an interesting advert because the comparison rate and APR are the same, but that doesn't negate the need to provide appropriate disclaimers and reinforce the cashback as part of this product. In this case, the product appears to be MB Bank (Budget Home Loan (Variable, Owner Occupier, P&I) with a cashback incentive between $3000 and $4000... but what's the harm in letting people know that? If you can't sell your service on the basis of something other than hiding rate and baiting consumers into contact, you probably shouldn't be a broker. The advert specifies savings of around "$4500 per year" without qualification, and the "lender spots are filling fast" blurb is misleading at best. The advertisement violates a number of pieces of legislation and ethical interest-duty based obligations. The company is obfuscating the lender (which was required in the first place) when specifically asked by those in the comment thread - a serious vocational and compliance-based infraction. The deliberate rate-baiting from Refinancier dates back several years. Update, 13th June 2026: As of this morning, Refinancier are pushing a new ad with an updated and valid rate of 4.79 + $4000 cashback. Changes do not include the required warnings and disclaimers required when using the comparison rate. The change comes in the aftermath of exposing their compliantly flawed experience in our Deception Funnel article. There's hope that we played a part in the change... although the experience requires far, far more work.

Importantly, post-publication clarification (such as replying to the comments in the threads above) does not cure an inadequate advertisement. Compliance obligations attach to the advertisement at the time it is published. The deliberate omission of the lender's identity, followed by a request that consumers contact the broker privately to obtain that information, transforms what should be a disclosure exercise into a lead-generation exercise. Information that is arguably material to the consumer's assessment of the product is withheld from the advertisement and released only after the consumer has engaged with the advertiser. From a behavioural economics perspective, the consumer's desire to identify the lender becomes the mechanism through which engagement is generated. The advertisement is no longer functioning solely as a vehicle for disclosure; it is functioning as a bait-funnel designed to convert curiosity into a sales interaction. The subsequent provision of lender details in response to individual comments does not alter the impression initially conveyed to consumers who viewed the advertisement but did not engage with the comment thread... and a broker that fails to acknowledge the enquiry, or one that responds privately and deliberately withholds legally mandated information, is operating in a manner that is akin to baiting. However, the adequacy of disclosure must therefore be assessed based upon the advertisement itself, not upon information that may later be provided to selected members of the audience.

Pictured: Compliance obligations attach to the advertisement at the time it is published, so if the advertisement is seen by a single consumer, you're in breach. All advertisements should be compliant at the time they're published, but most advertising agencies simply don't understand the complexities, and most DIY courses don't introduce the compliance framework that'll protect you from legal exposure. Our Broker Growth program includes a full session on compliance, and our continued oversight ensures that you're representing yourself in a legal and ethical manner. None of the pictured ads meet basic legals standards.

For this reason, prudent compliance practice dictates that mortgage advertisements should clearly identify not only the interest rate, comparison rate and statutory assumptions, but also the lender or credit provider associated with the advertised product. While this may not be expressly prescribed by section 162 in every circumstance, it is strongly aligned with the legislative objective of ensuring that consumers receive sufficient information to understand the product being promoted and the basis upon which the comparison rate has been calculated.

Bait Advertising on Rate, and Product Accessibility

"Bait advertising" is one of those concepts that sounds intuitive in marketing discussions but is actually quite specific in legislation, and importantly, it sits primarily in the Australian Consumer Law, not the comparison rate regime itself, so while many examples described as 'bait advertisements' do not satisfy the definition in the traditional legal sense, the practice bears similarities to what may be described as digital bait-and-engage advertising. An attractive rate is publicly displayed, while material product information is withheld until the consumer initiates contact. The consumer's inability to identify the lender from the advertisement itself becomes the catalyst for engagement. In effect, the missing disclosure becomes part of the marketing strategy.

Why We're Critical of Refinancier: Of all the groups that'll never call us, Refinancier is probably at the top of the list. We have screenshots and screen recordings dating back to Covid-era rates, and the conduct is consistently not compliant. In 2024 we called them offering compliance support and were kindly told to go and procreate with ourselves. In operating dishonestly, one has to question where the interest of the business lies, and whether Best Interest Duty overlaps with their marketing efforts. Intentional deception (as evidenced by the Facebook comments above) are a metaphorical middle finder to those that they claim to support, and it's an insult to the brokers that represent themselves honestly, ethically, and to legal standards. If your first contact with a consumer is predicated on a lie, the relationship itself is built upon a fraudulent digital handshake.

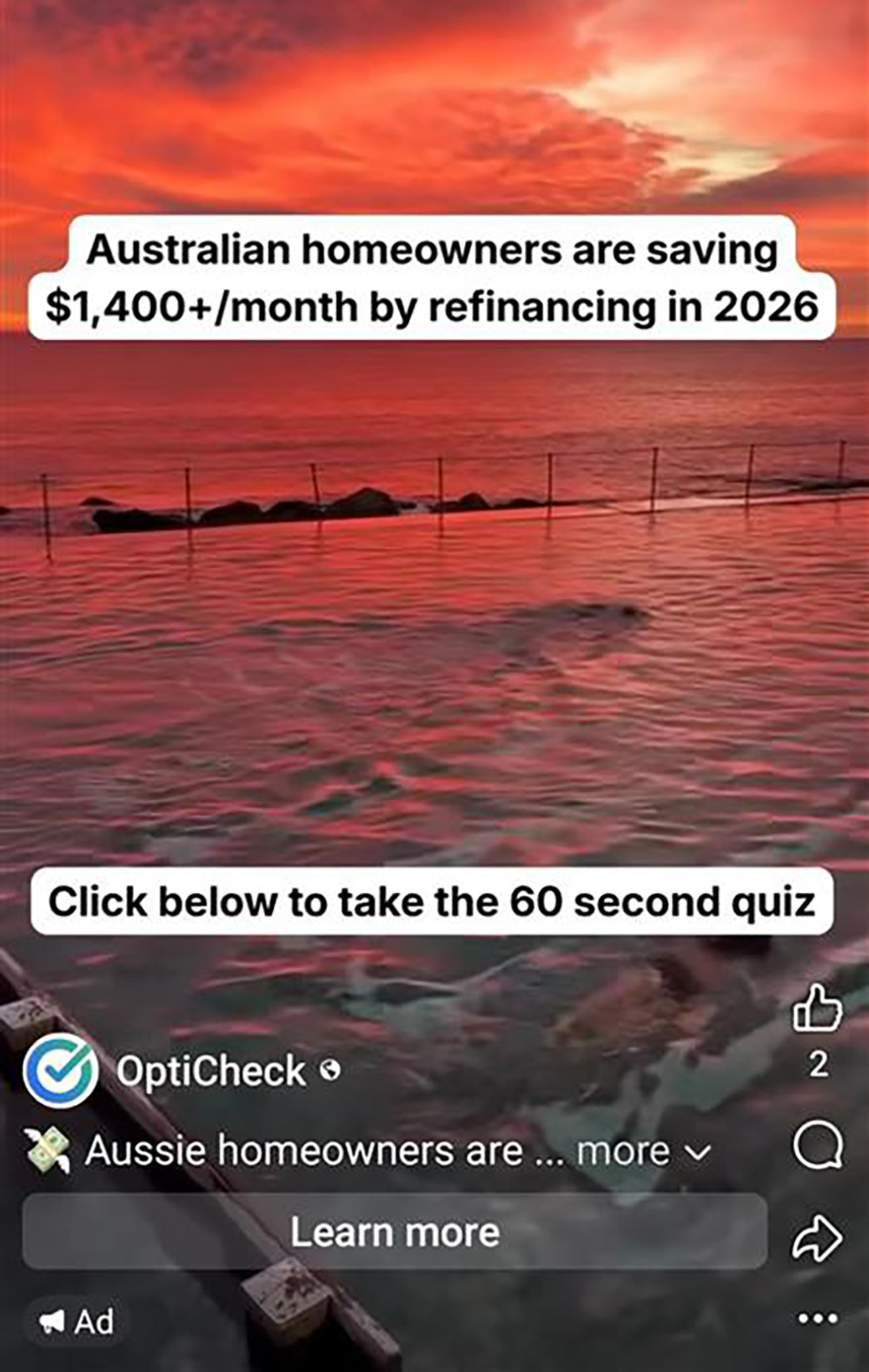

Australian Consumer Law (ACL) in Schedule 2 of the Competition and Consumer Act 2010 (Cth), Section 35(1) states that "[a] person must not, in trade or commerce, advertise goods or services for supply at a specified price if there are reasonable grounds for believing that the person will not be able to supply reasonable quantities of the goods or services at that price for a reasonable period and in reasonable quantities", and its this definition that we rely upon for rate-based marketing. In essence, a low rate is used as a "headline offer" without a reasonable ability or intention to supply it to the majority of the market. Disclaimers seek to ratify this ambiguity along with advertising copy and creative in order to silo a suitable target audience.

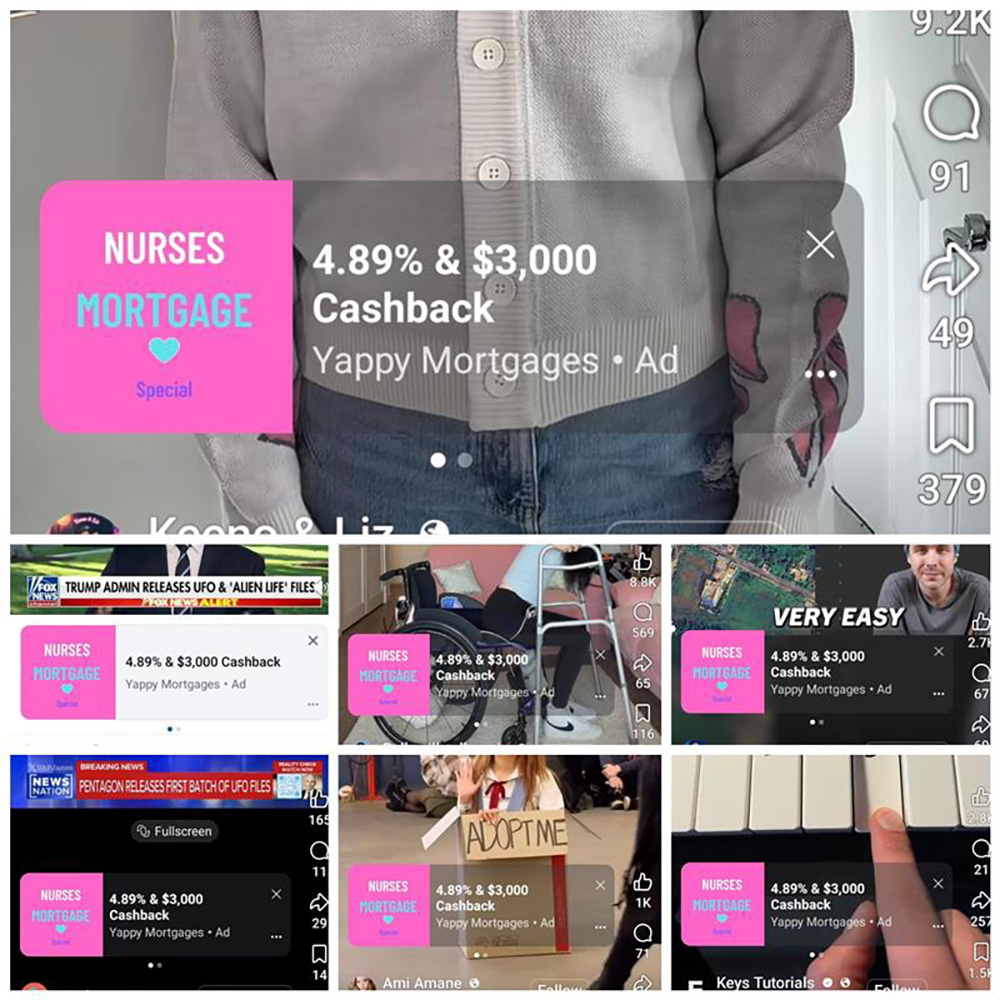

Pictured: Lead generation groups are usually the most non-compliant, and those self-hosted solutions that they introduce to businesses geneeallyt aren't any better. The pictured examples are from 'Finance Group AU' - a ficticious brand created by Biz Focused. Methods used by the likes of Bizleads are grossly non-compliant, and their Deception Funnels should bd understood by any broker that has purchased their poor leads in the past. We've inherited clients from Leadify that spent $8000 for just 50 leads and converted none of them - a serious indictment on their poor process. Most leadgen charlatans lean on rate bait almost exclusively (with fake Deception Funnel qualification) since they have nothing else to offer.

ASIC Regulatory Guide 234 (RG 234) does not redefine bait advertising in a new statutory sense. Instead, it treats it as part of broader prohibitions against misleading or deceptive conduct (ACL s18 / ASIC Act s12DA), false or misleading representations (ACL s29), and overall impression testing of advertisements. It specifically warns that: fine print does not cure a misleading dominant message, partial disclosure can itself be misleading, and prominence (and "headline prominence") matters as much as accuracy. RG 234 - remembering this is ASIC guidance designed specifically for advertising - effectively broadens bait advertising concepts into a general anti-manipulation framework, rather than limiting it to "unavailable stock at advertised price". RG 234’s core principle is that advertising must be assessed by the overall impression created on the ordinary and reasonable consumer.

Our earlier examples from Rate of the Week and Refinancier (two examples taken in the last day from hundreds we've archived) may not fit the definition of classical bait advertising because the rate is usually genuinely available to some borrowers, or at least not "unavailable in reasonable quantity" in the ACL sense, the issue is not supply of the product at the advertised price, so it's a case of information asymmetry and disclosure structure, not 'non-supply'... but the anecdotal 'common language' definition is satisfied without doubt - the rates were used in isolation and without supporting legal information to capture a larger and more reasonable percentage of the market; it's blatant lead capture disguised as product promotion. Remember, consumer perception is more important than marketing intent, and deliberate baiting or deception is usually clearly identified (particularly when supported by way of a pattern or history of a broker's deliberate malfeasance).

Comparison Rate Warnings and Disclosure Presentation

The comparison rate warning occupies a uniquely important position within our advertising framework because it serves as the mechanism through which legislators sought to counteract one of the most persistent behavioural biases exhibited by consumers when evaluating loan products: the tendency to focus almost exclusively on the headline interest rate while overlooking the broader cost structure of the credit contract (or promoted product). The comparison rate regime was introduced to provide a more meaningful basis for product comparison by incorporating both the interest rate, term, and prescribed fees and charges into a single indicative figure. However, legislators recognised that even the comparison rate itself is subject to assumptions, limitations and exclusions. Consequently, the law requires not merely the disclosure of the comparison rate, but also the disclosure of a warning explaining the circumstances in which that comparison rate may not accurately reflect the cost of a particular loan.

Section 163 of the National Credit Code provides that a comparison rate appearing in a credit advertisement must be accompanied by a warning prescribed by the regulations. The prescribed warnings are contained within Regulation 99 of the National Consumer Credit Protection Regulations 2010 and exist in both short-form and long-form variants.

Short Form Warning: "WARNING: This comparison rate is true only for the examples given and may not include all fees and charges. Different terms, fees or other loan amounts might result in a different comparison rate"

Long Form Warning: "WARNING: This comparison rate applies only to the example or examples given. Different amounts and terms will result in different comparison rates. Costs such as redraw fees or early repayment fees, and cost savings such as fee waivers, are not included in the comparison rate but may influence the cost of the loan".

At first glance, these warnings may appear to be little more than technical disclaimers. Such an interpretation would be fundamentally mistaken. The warning requirement is not a peripheral compliance obligation designed merely to satisfy a legislative formality. Rather, it represents a core component of the comparison rate disclosure regime itself. The warning exists because Parliament recognised that consumers frequently attribute a level of certainty and universality to numerical representations that exceeds what the underlying calculation can legitimately support. or convey. In practical terms, the warning functions as a legislative safeguard against the false precision that can arise when complex lending arrangements are reduced to a single numerical figure.

The placement and presentation of the comparison rate warning is therefore among the most tightly regulated disclosure requirements within the entire credit advertising framework. This area is frequently misunderstood by brokers because the legal obligations arise from the combined operation of the National Credit Code and Regulation 99, creating a layered disclosure regime in which the comparison rate and the warning are legally inseparable.

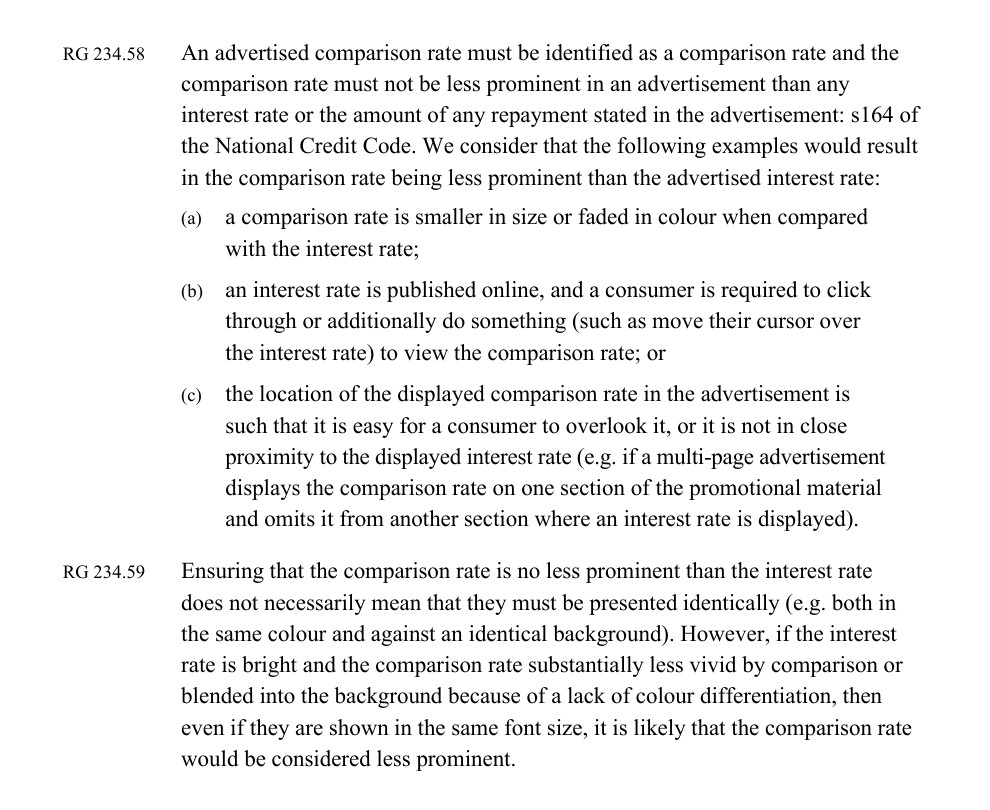

Pictured: The advertisement from Nick Ireland (first two images to the left) is a good example of somebody making an attempt to meet compliance obligations in that they've included the comparison rate... but they've 'invented' a disclaimer that doesn't come close to meeting legislated requirements. Additionally, the use of the rate in isolation at any point - particularly in the title as shown above - presents numerous problems when the abbreviated ad is shown in various other placements (as indicated by way of this advert from Yappy (they have a history of blatant rate-based non-compliance. The advertisement from DS Finance (second two images) also includes the comparison rate, but can you see it? It fails the prominence test, doesn't include any of the required disclaimers, and makes significant attempts to obfuscate the comparison rate itself. The fact the comparison rate in this screenshot is 5.85% doesn't negate the need to include it. Both ads expose the brokers to a range of compliance issues and should be removed from circulation.

The starting point is the requirement contained within section 163 itself. The legislation does not state that a warning should be provided somewhere within the advertisement, nor does it suggest that the warning may be made available upon request or accessed through a separate disclosure document or landing page. Instead, the legislation requires that the comparison rate be accompanied by the prescribed warning. The significance of this language should not be understated. The comparison rate and the warning are intended to operate as a single composite disclosure. The law does not treat them as separate advertising elements capable of independent presentation. Rather, the warning forms part of the comparison rate disclosure itself.

Pictured: None of the pictured advertisements meet the legal standard, and none include the required comparison rate and associated warnings. Legislation does not state that a warning should be provided somewhere within the advertisement, nor does it suggest that the warning may be made available upon request or accessed through a separate disclosure document or landing page. Instead, legislation requires that the comparison rate be accompanied by the prescribed warning. The significance of this language should not be understated. The comparison rate and the warning are intended to operate as a single composite disclosure. The law does not treat them as separate advertising elements capable of independent presentation. Rather, the warning forms part of the comparison rate disclosure itself. There's never an excuse to not publish the comparison rate, and in Meta advertising there's never an excuse to exclude comparison warnings or quantified disclosures within the create and copy.

This distinction has important practical consequences. An advertiser cannot lawfully display a comparison rate as a prominent headline feature while relegating the prescribed warning to an unrelated section of the advertisement, a separate webpage, landing page, a distant footnote or a disclosure accessible only through additional consumer interaction. Such an approach undermines the very purpose of the legislative scheme. The consumer must encounter the warning as part of the same cognitive process through which they encounter the comparison rate. The disclosure regime is designed to ensure that consumers receive both the numerical figure and the contextual limitations of that figure simultaneously.

The Comparison Rate in Facebook (Meta) and Banner Adverising: While the legislative framework establishes a clear expectation that comparison rates be accompanied by the prescribed warning, the practical application of these requirements in digital advertising environments is more nuanced than many advertisers appreciate. This is particularly evident when considering the interaction between the statutory disclosure requirements and ASIC's guidance regarding space-constrained advertising formats. ASIC addresses this issue within Regulatory Guide 234, recognising that certain advertising mediums present genuine physical limitations that may affect the amount of information capable of being displayed. The regulator acknowledges that there may be circumstances in which it is impractical to include every disclosure element within a single advertisement, particularly where the advertisement is restricted by significant space constraints. Examples may include small-format banner advertisements, certain search engine advertisements, display network placements and other highly constrained digital formats where character limits or display dimensions materially restrict the amount of information capable of being communicated. However, this recognition should not be interpreted as a broad exemption from disclosure obligations. ASIC's guidance does not suggest that disclosures become unnecessary merely because an advertisement appears online or because an advertiser wishes to prioritise marketing content over compliance information. Rather, the guidance reflects a practical recognition that disclosure requirements must sometimes be evaluated within the context of the advertising medium itself. The relevant question remains whether the advertisement, viewed as a whole, creates a misleading impression or omits information that a reasonable consumer would require in order to properly understand the representation being made. Importantly, the rationale underpinning these limited exceptions is rooted in genuine space constraints. The policy basis is not that warnings become less important in digital environments, but that certain advertising formats may physically prevent the simultaneous presentation of all required information. In such circumstances, ASIC expects advertisers to carefully consider how consumers will obtain the omitted information and whether the overall communication remains balanced, accurate and not misleading. In practice, this distinction becomes highly relevant when examining modern social media advertising, particularly advertisements distributed through platforms such as Facebook and Instagram via the Meta advertising network. Unlike traditional banner advertisements, Meta advertisements generally provide advertisers with substantial opportunities to communicate information through multiple components of the advertisement. A typical mortgage advertisement may contain a visual creative, primary text, headline text, description text, call-to-action elements and landing page links. Collectively, these elements provide significantly more disclosure capacity than is available within the narrow confines of a traditional display banner. As a result, the practical justification for omitting comparison rate warnings from Meta advertisements is often substantially weaker than advertisers assume. In most circumstances, sufficient space exists to present the advertised interest rate, the comparison rate and the prescribed warning within the overall advertisement structure. The inclusion of the warning rarely creates a meaningful operational burden given the available character limits and content areas. Indeed, across the mortgage and financial services sector it has become common practice for compliant advertisers to incorporate the prescribed comparison rate warning directly within the primary advertisement copy whenever an interest rate and comparison rate are promoted. This reflects both regulatory prudence and commercial reality. Financial services advertisers are acutely aware that ASIC evaluates advertisements according to their overall impression rather than through a purely technical assessment of whether information can be found elsewhere. Where an advertiser has ample opportunity to include the prescribed warning but elects not to do so, it becomes increasingly difficult to argue that any omission was necessitated by genuine space limitations. Instead, the omission may be perceived as a deliberate decision to prioritise promotional messaging over consumer understanding. The issue becomes even more significant when considering consumer behaviour within social media environments. Unlike consumers navigating to a lender's website after conducting independent research, users encountering mortgage advertisements within social media feeds are frequently engaging with content passively and often for only a brief period. The advertisement itself therefore assumes heightened importance as the primary source of information influencing the consumer's initial perception of the product. If a headline interest rate is displayed without the corresponding contextual information required to properly interpret that rate, there is a heightened risk that consumers will form impressions based upon incomplete information before deciding whether to engage further. From a regulatory perspective, this aligns closely with ASIC's repeated emphasis on prominence, balance and overall impression throughout RG 234. The existence of additional information on a landing page does not necessarily neutralise a misleading impression created within the advertisement itself. The regulator's focus remains on the information available to consumers at the point the representation is made. Consequently, where sufficient space exists to include a comparison rate warning, its omission may undermine arguments that the advertisement has been designed to communicate information in a clear, balanced and effective manner. For this reason, the industry norm among sophisticated lenders, aggregators and mortgage brokers has increasingly shifted toward including comparison rate disclosures and prescribed warnings within the body of Meta advertisements whenever rates are promoted. This approach not only reduces compliance risk but also reflects the broader regulatory objective underpinning the comparison rate regime: ensuring that consumers receive both the advertised benefit and the contextual information necessary to properly evaluate that benefit at the same time. While RG 234 recognises that limited exceptions may exist for genuinely space-constrained advertising formats, those exceptions should not be viewed as a general justification for omitting disclosures in environments where adequate disclosure space is readily available. In practical terms, the vast majority of contemporary Meta advertisements possess sufficient capacity in the creative and copy to accommodate comparison rate and other warnings, and industry practice has evolved accordingly. Failure to provide the warnings is measured in degrees of deception, and the 'spirit' of the RG document was aimed at space and functionally limited Google Advertisements.

From a behavioural psychology perspective, this paired comparison and warning requirement is entirely logical. Consumers exhibit a well-documented tendency toward numerical anchoring, whereby prominent numerical values become the primary reference point around which subsequent judgments are formed. A comparison rate displayed without an immediately accompanying warning creates a substantial risk that the consumer will internalise the figure before considering the assumptions and limitations upon which it is based. By requiring the warning to accompany the comparison rate, the legislation seeks to prevent consumers from treating the figure as universally applicable or representative of all borrowing scenarios.

Pictured: Consumers exhibit a well-documented tendency toward numerical anchoring, whereby prominent numerical values become the primary reference point around which subsequent judgments are formed. A comparison rate displayed without an immediately accompanying warning creates a substantial risk that the consumer will internalise the figure before considering the assumptions and limitations upon which it is based. By requiring the warning to accompany the comparison rate, the legislation seeks to prevent consumers from treating the figure as universally applicable or representative of all borrowing scenarios. None of the pictured advertisements come close to meeting a legal standard.

Although the legislation does not prescribe pixel dimensions, font sizes or exact visual layouts, this does not mean that advertisers enjoy unlimited discretion regarding presentation. The absence of prescriptive formatting requirements should not be interpreted as an absence of prominence obligations. Rather, the legislation adopts a functional approach. The relevant question is not whether a warning technically exists within the advertisement, but whether the warning is presented in a manner capable of effectively communicating its intended message to a reasonable consumer.

Prominence Requirements: Although neither the National Credit Code nor the National Consumer Credit Protection Regulations prescribe specific font sizes, colour requirements, pixel dimensions or visual layouts for comparison rate warnings, this should not be interpreted as conferring unlimited discretion upon advertisers. The legislative framework adopts a principles-based approach centred upon prominence, readability and consumer comprehension rather than prescriptive design standards. Section 164 of the National Credit Code introduces an express prominence requirement, while ASIC's Regulatory Guide 234 repeatedly emphasises that disclosures must be sufficiently clear and prominent to effectively communicate their intended message. Consequently, factors such as font size, colour contrast, visual hierarchy, placement and readability become legally relevant not because they are expressly prescribed by legislation, but because they directly influence whether the disclosure is capable of being noticed, read and understood by a reasonable consumer. In practical terms, the compliance question is not whether a warning technically appears within the advertisement, but whether the overall presentation enables the warning to fulfil the consumer protection purpose for which it was mandated. Failure to achieve this outcome may expose the advertisement to scrutiny not only under the National Credit Code but also under the broader misleading and deceptive conduct provisions contained within sections 18 and 29 of the Australian Consumer Law.

Small or Obfuscated Print Fails the Sniff Test: RG 234 repeatedly stresses that disclosures must be sufficiently prominent to be noticed by a reasonable consumer on first viewing. From a psychological perspective, consumers do not process advertisements linearly. Potential borrowers will generally process the headline (and quantifiable statements), imagery, large numerical values, and supporting information - in that order. Disclaimers are typically processed last, if at all, and often ignored if the print is too small - a common and shonky marketing method of evading 'detection'. RG 234.58 and RG 234.59 remedies and ratifies legislation by providing guidance (although given it comes from ASIC it should be considered an instruction) that applies to comparison prominence. It states that they would consider the comparison rate being less prominent than the advertised interest rate if rate is smaller in size or faded in colour when compared with the interest rate, a consumer is required to click through or additionally do something to view the comparison rate, or the location of the displayed comparison rate in the advertisement is such that it is easy for a consumer to overlook it, or it is not in close proximity to the displayed interest rate. The practical takeaway is that while they don't require the two rates to be identical, they do require that they are essentially similar despite their differences.

This principle is reinforced by section 164 of the National Credit Code, which requires that a comparison rate not be given less prominence than the annual percentage rate or repayment amount with which it is associated. More broadly, ASIC's Regulatory Guide 234 emphasises that disclosures must be clear, balanced and sufficiently prominent to ensure that consumers are not misled by the overall impression conveyed by the advertisement. The regulator has repeatedly stressed that qualifications and warnings cannot be used to cure a misleading headline if the overall presentation causes consumers to focus on the benefit while overlooking the associated limitations.

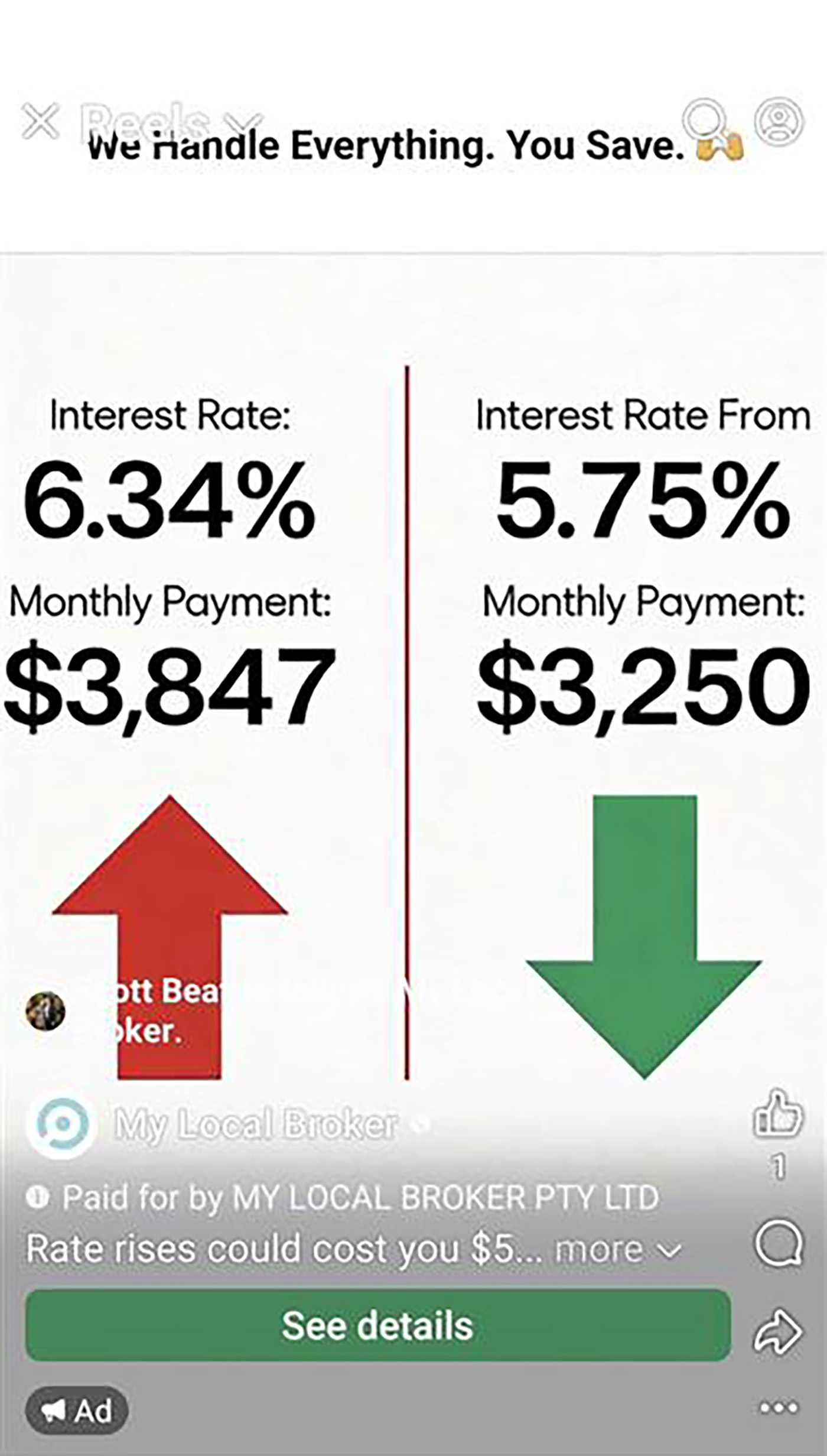

Pictured: Although neither the National Credit Code nor the National Consumer Credit Protection Regulations prescribe specific font sizes, colour requirements, pixel dimensions or visual layouts for comparison rate warnings, this should not be interpreted as conferring unlimited discretion upon advertisers. The legislative framework adopts a principles-based approach centred upon prominence, readability and consumer comprehension rather than prescriptive design standards. RG 234 repeatedly stresses that disclosures must be sufficiently prominent to be noticed by a reasonable consumer on first viewing. From a psychological perspective, consumers do not process advertisements linearly. Potential borrowers will generally process the headline (and quantifiable statements), imagery, large numerical values, and supporting information - in that order. Disclaimers are typically processed last, if at all, and often ignored if the print is too small - a common and shonky marketing method of evading 'detection'. RG 234.58 and RG 234.59 remedies and ratifies legislation by providing guidance (although given it comes from ASIC it should be considered an instruction) that applies to comparison prominence. It states that they would consider the comparison rate being less prominent than the advertised interest rate if rate is smaller in size or faded in colour when compared with the interest rate. While a couple of the pictured advertisements include the comparison rate, they don't pass the test of objective reasonableness. Crown Finance have had some interesting adverts - some extremely poor. In the pictured example, they haven't published the comparison rate, but they're also promoting a commercial product - a space where the comparison rate doesn't necessary apply. However, the inclusion of the rate is predicated on both the environment in which you operate and whether residential property plays a part in a transaction, so in this case, a full disclosure, warning and disclaimer should be shown, and it was not shown on the advert or continued experience. The advertisement from Murual Bank is an interesting one because they've shown just the comparison rate - not expressively prohibited by law, but the inclusion of the comparison rate triggers immediate and inline warnings which includes the rate, term, product, comparison rate, comparison warning, and other information. In practical terms, there's no valid reason to ever publish a comparison rate in isolation unless it supports product tiers and variations. Oliey have excluded copy-based warnings and disclaimers but they've also excluded the comparison rate from the advert title. The title is often shown in isolation, and all standard requirements apply. Never show a rate without the accompanying comparison rate. Simple.

Accordingly, compliance cannot be assessed solely by asking whether the prescribed wording appears somewhere within the advertisement. The more substantive question is whether the comparison rate warning is displayed in a manner that allows it to perform the function legislators intended it to perform. A warning hidden within dense fine print, obscured through poor contrast, separated from the comparison rate by substantial visual distance, or otherwise presented in a manner unlikely to attract consumer attention may satisfy the literal wording of the regulation while nevertheless creating significant regulatory risk. Both ASIC and the courts routinely assess advertising by reference to its overall impression rather than through a narrow technical analysis of individual disclosure elements.

The Comparison Warning Must not be less prominent than the comparison rate: The regime requires that the warning be presented: clearly, prominently, and in a way that is not inferior in visibility to the comparison rate itself Practically, this means that it cannot be hidden in a footnote if the comparison rate is in a headline, it cannot be visually de-emphasised (tiny font/low contrast/buried placement), and it must be perceivable in the same field of attention as the rate disclosure. This is reinforced by general consumer law principles under ACL s18, ASIC Act s12DA, and ASIC RG 234 (overall impression test).

Must be “accompanying” in a meaningful sense: “Accompanied” is interpreted functionally, not literally. So regulators assess spatial proximity (is it adjacent or detached?), visual hierarchy (is it subordinate or equivalent?), temporal proximity (in digital ads, is it shown at the same time?), and cognitive association (would a reasonable consumer link them?). If the warning is on a separate page, behind a link, or in expandable disclosure, then it risks being treated as not truly accompanying the comparison rate.

Pictured: The comparison requirements are introduced in the first hour of the first day of mortgage broker Cert IV education courses. There are few industries regulated to the same high standards, and there are very few services that can be accused of predatory behaviour on the basis of their advertising... and mortgage broker services are one of them. Our programs have consistently delivered better results, and we've never inherited a program where we weren't able to triple results - this supports our claim that ethical and legal advertising resonates with borrowers, while those that hide behind numbers and compliant-challenged presentations will always compromise their performance and conversions.

Pictured: Viewed holistically, the comparison rate warning is not simply a disclaimer attached to a rate advertisement. It is an integral component of the comparison rate itself. The warning exists to communicate the assumptions, limitations and exclusions inherent within the comparison rate calculation and to ensure that consumers do not attribute unwarranted certainty to a figure that is necessarily dependent upon a prescribed set of hypothetical circumstances.

Viewed holistically, the comparison rate warning is not simply a disclaimer attached to a rate advertisement. It is an integral component of the comparison rate itself. The warning exists to communicate the assumptions, limitations and exclusions inherent within the comparison rate calculation and to ensure that consumers do not attribute unwarranted certainty to a figure that is necessarily dependent upon a prescribed set of hypothetical circumstances. The legislative framework therefore treats the comparison rate and its accompanying warning as a unified disclosure mechanism, reflecting a broader regulatory objective of promoting informed consumer decision-making and preventing the distortive effects of incomplete financial information.

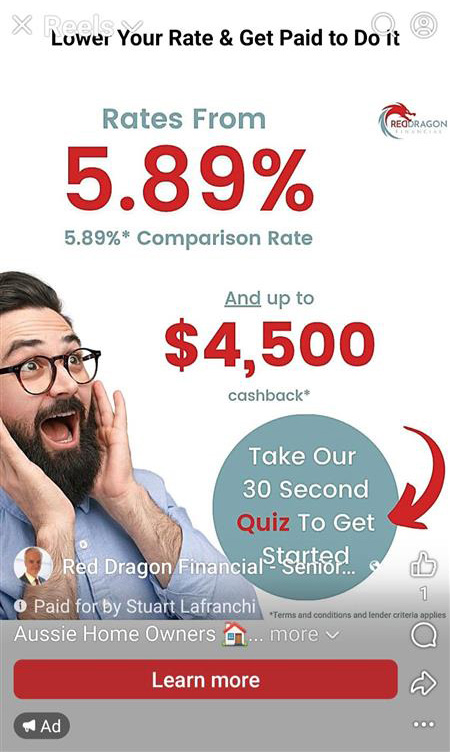

Technical Presentation of Warnings and Disclaimers in Meta and Other Advertisements: Comparison rate warnings should be adapted to the specific technical and behavioural constraints of each advertising format, rather than treated as a static block of text applied uniformly across placements. In Meta environments, this includes 1:1 feed placements (square), 4:5 portrait feed ads, 9:16 vertical Stories and Reels formats, 16:9 landscape placements (often used for in-stream video or link previews), and increasingly responsive placements where creative is dynamically cropped or reflowed across devices. The compliance risk is not merely whether the warning exists, but whether it is actually visible in the delivered ad unit as experienced by the end user. This requires designing disclosure placement to survive platform compression, UI overlays (such as profile icons, captions, CTA buttons, and “Sponsored” labels), and safe-zone cropping - particularly in 9:16 formats where lower-screen UI elements frequently obscure text. In practical terms, warnings should be embedded within the visual safe area of each aspect ratio, sized with sufficient contrast and padding to remain legible across mobile scaling, and duplicated where necessary across creative variants to ensure persistence across placements. Critically, advertisers should avoid relying solely on platform auto-cropping or dynamic text rendering, as these can reposition or truncate disclosures unpredictably; instead, compliance-critical warnings must be anchored within the creative itself in a fixed and visually controlled position so that the comparison rate warning is consistently presented to the consumer in the same form in which it was approved and intended to be viewed. We disusss this again in the section on Video Advertising.

Comparison and Other Disclosures in Video