One of the most overlooked requirements in Australian financial advertising is the prohibition on creating a misleading "overall impression" in advertising or during the top-of-funnel subscription experience - even when every individual statement in the ad is technically true... and there's thousands of ads playing out right now that are technically (and usually clearly) illegal. At a time when we're engaged in silent war with lenders and AI, right now is a time when we should be more mindful of the serious consequences of blatantly breaking the law... or even testing legal limits. The problem is that most of the subscription funnels introduced to brokers are deliberately deceptive as a means to improve upon lead flow. While there are clear ways to improve the conversion rate, lying and deception are not two of them.

Broker Booking Funnel: We give away the ideal and extremely high-performing format for a mortgage broker calendar booking funnel in an article titled The Basic Mortgage Broker Booking Funnel. The funnel shows you how to accomplish in one page that takes others three, and it provides the best-practice framework that consistently delivers betters, higher-quality, compliant leads. The funnel architecture we describe on this page is diametrically opposed to anything resembling best practice.

Broker Growth Program: In the two decades we've run our well-established Broker Growth Program, the number of brokers we've lost to others is less than 5, and we've inherited that number from others in the last week alone. We deliver a webinar product to brokers that includes landing pages and technology... and then teach you how to use it. We hold a webinar series that teaches you directly how to get better results that those introduced to you via dodgy marketing agencies, and you'll have a better knowledge of financial advertising than those that claim to provide a service. Nobody knows your business better than you do, and we simply teach you how to promote it in a very short period of time. We still provide a managed service, but we want brokers to have control over their marketing. The program is discussed in an article titled "The Mortgage Broker Growth Webinar Program". Stop playing games with your lead generation and introduce a bullet-proof, scalable, compliant, and high-performing solution that you own. Those that hijacked our Broker Growth name are the single reason we introduced our early 1 million 3X guarantee as we needed to ensure that the non-compliant, usually broken, and mediocre performance of the 'other' program didn't damage our established reputation for high-performing experiences.

CARE Program: Our CARE (Compliance and Regulatory Education) program was designed as a program that we'd deliver to aggregation groups, with most of our efforts applied by way of speaking gigs at Professional Development days. The program was modified quite recently and is now part of the 'Broker Growth' webinar stack. We've run this standalone webinar a couple of times in the few weeks before publishing this article, and we now run it as a free webinar on the first Wednesday of every month.

Comparison API: Reference is made in this article to the presumption that results will be returned to a page based on user input. It should be noted that even our most basic experiences on landing pages includes the facility to retrieve accurate comparison results. The redirect to a calendar page that I also discuss is also included within the primary form (thus negating the compliance issues associated with linking off-site). The Comparison API and Lender API are generally freely available, and both are essentially ingredients in a high-performing funnel.

When regulators or prudent aggregators assess your advertising or any consumer-facing assets, they'll consider the dominant message conveyed to an ordinary consumer, not just literal accuracy, and in terms of prosecution, courts will primarily refer to s12DA ASIC Act and ACL s18 to shape the "false and misleading representation provisions" that determine how our advertising is manufactured. It is the misleading representation that is utterly ubiquitous and somewhat normalised in financial advertising, and the seedy and deliberately deceptive methods used by anybody that crafts out a landing page or advert simply need to come to an end.

Rescue Program: Our results are evidence that you will see better conversions through honesty, transparency, and ethical practices. As a means of exposing the performance of poor funnel design and advertising mediocrity, we ran a $1-million guarantee against tripling the results of those in our 'Rescue Program' (we're currently running at $2 million program for a limited number until the end of August). Rescue is focused on performance and effectiveness rather than compliance, but those that we inherit from others are always grossly non-compliant. Those in Rescue include the likes of Bizleads, Broker Grow, Marketing Transformers, Sunbear, virtually all pay-per-lead services, and a large number of others that claim an expertise in the mortgage market. The most recent batch of incoming candidates for the $2m program generally aren't always suitable since we've 'fixed' their problem in minutes. Right now, there's a ton of ads linking to adult content, some are linking to the calendar of another broker (a massive number, in fact), and all are plagued with fundamental advertising errors. The fact we were able to insure our results in the first place - an Australian first - gives you an indication of how others operate, and why many brokers fail to see a satisfactory ROAS (Return on Ad Spend).

Of the thousands of adverts that make their way onto social media each day, there's barely a handful that are compliant, and while unintentional exclusions in messaging might be 'generally' forgiven or temporarily overlooked by our legislative overloads, the deception that I'll look at in this article is the overt and deliberate deception that is used in order to manipulate lead flow through intentional - and one might argue, fraudulent - funnel practices. The article looks at the most common methods of consumer deception (common to almost all of those in our Rescue Program), and why that deception is regarded as criminal conduct that will potentially expose you to litigation from various regulatory bodies. The article is by no means exhaustive when it comes to consumer manipulation of pathway deception, but it's a start.

What if I Fix Compliance Issues?: Decades of court interpretation and regulator enforcement practice makes it clear that it does not matter if the error was corrected - it's that it was shown to consumers in the first place. Competition and Consumer Act 2010 (Cth), Schedule 2, especially Section 18 - misleading or deceptive conduct, and Section 29 - false or misleading representations, and in the ASIC Act 2001 (Cth), particularly Section 12DA and Section 12DB prohibits the engagement in misleading conduct. Legally, the contravention occurs at the time the misleading representation is communicated, published, displayed, broadcast, or otherwise conveyed to consumers. In other words, the breach crystallises upon publication or exposure, and you cannot retrospectively erase the original contravention. This principle is deeply embedded in Australian misleading advertising jurisprudence because the law focuses on the impression created when consumers encountered the material, and not whether the advertiser later changed its mind. The closest formal articulation from regulators is found in ACCC and ASIC guidance emphasising "overall impression", "first viewing", and the effect on consumers at the time of exposure. For example, the ACCC states that misleading conduct occurs where claims create a false impression for consumers, regardless of intention. Similarly, courts repeatedly assess what consumers saw, what impression was conveyed, and whether the conduct was misleading at that moment. Subsequent correction may often mitigate penalties, demonstrate cooperation, reduce ongoing damage, or affect enforcement discretion, but a self-declaration is usually required - this acknowledges your malfeasance and provides full transparency (don't hide behind your errors)... but even self-reporting does not extinguish the fact that consumers were already exposed to the misleading representation.

What I Don't Discuss: There's a minefield of information that I'll address is subsequent articles, with each post accompanied by real-world examples. For example, we introduced widespread malfeasance to one particular aggregator a few years ago that would have prevented very high-profile negative attention. Those brokers associated with the specific operations were engaged in fraud, offshore telephone canvassing, robocalls, and other illegal activities. Our information was ignored, and Amtrac now occupy a special place in their head office.

Not Legal Advice: Nothing in this article constitutes legal advice. My advice to you is to have your financial solicitor review any consumer-facing content for potential compliance issues. Almost all of the displayed experiences would never have made their way into a live environment if they were property scrutinised. I suggest that you don't rely on aggregation-level compliance teams as they often lack the applicable knowledge. The small investment for a legal opinion is a means of sensible risk management - protect your business.

Hundred of Meta Advert Reviews

We occasionally record reviews of compliance-challenged social media adverts and post them into a Facebook Group  for brokers that are interested in improving their marketing efforts and lead flow. What's resulted is thousands of video and image reviews designed to illustrate poor performing experiences, deceptive funnels, non-compliance, and deliberate deceit. A few of those reviews will be useful for article context, and just a few of the most basic compliance reviews are shown below (click to launch the YouTube modal).

for brokers that are interested in improving their marketing efforts and lead flow. What's resulted is thousands of video and image reviews designed to illustrate poor performing experiences, deceptive funnels, non-compliance, and deliberate deceit. A few of those reviews will be useful for article context, and just a few of the most basic compliance reviews are shown below (click to launch the YouTube modal).

We've called out the non-compliance and deception for years, and we've reviewed thousands of ads that we categories in the abomination basket. In years past, we'd create the SHAD, or "Shit Advert of the Day" which we canned only because there's too many of them and we found ourselves repeating the same thing over and over. You'll find several hundred SHAD Reviews in our Social Library.

[image] shortcode. FAQ: "How to Display YouTube Modal Thumbnail Images with Image Shortcode".Compliant Finance Advertising for Mortgage Brokers

We don't enjoy calling out the marketing mediocrity in the market. However, as the leading agency that provides a financial digital service, we felt an obligation to provide brokers with the education that they need in order to make informed decisions, and we felt it necessary to expose experiences that may introduce potential litigation, compromised accreditations, lender interference, or some other form of nastiness to their operation. We have an old article on this subject - mainly as it relates to dodgy leadgen services - in an article titled "Compliant Finance Advertising Explained".

We shouldn't diminish the role of our digital presence or assign a lesser importance to compliance in the marketing space. Digital is every bit as important as your internal business compliance... but it's often a weak point in your business armour that potentially leaves you liable to prosecution. If ASIC, the ACCC, or anybody else, ever decides to pursue marketing non-compliance with any vigour we'll likely see a large number of brokers before the chopping block. At the heart of this problem is pay-per-lead services, and we discuss the hideous methods used by leadgen charlatans in an older article titled "Ethical and Legal Financial Advertising".

Comparison sites, lead generators, affiliates, publishers, and other unlicensed entities are subject to Australian misleading advertising laws, even if they do not hold an Australian Credit Licence (ACL), Australian Financial Services Licence (AFSL), or operate under one of the mentioned licences. A business does not need to be licensed to breach the ASIC Act, Australian Consumer Law, or attract ASIC/ACCC enforcement. The single question that determines exposure is this: are they engaging in conduct "in trade or commerce" relating to financial services or credit activities? An article titled "Misrepresentation of Interest Rates (Rate Bait) in Search Results" looks at how just a few comparison websites  are making what can only be construed as deliberate consumer-facing representations in order to garnish traffic.

are making what can only be construed as deliberate consumer-facing representations in order to garnish traffic.

ASIC Act 2001 (Cth), Section 12DA clearly states that “[a] person must not, in trade or commerce, engage in conduct in relation to financial services that is misleading or deceptive or is likely to mislead or deceive". Note that the text says "person" and not licensee, AFSL holder, or credit licensee - it is deliberately broad to include anybody that touches the industry. ASIC Act Section 12DB is similarly broad in that is prohibits false or misleading representations concerning financial services; again, applying to "a person" and not merely licensed entities. Australian Credit Law (ACL) Section 18 also states that "[a] person must not, in trade or commerce, engage in conduct that is misleading or deceptive or is likely to mislead or deceive".

The National Consumer Credit Protection Act 2009 (NCCP) regulates credit activities, credit assistance, referrals, representations, and some dodgy lead generators attempt to avoid licensing by claiming they merely "introduce" (some use the underly cautious word "refer"...), but there are clear limits, and the NCCP broadly defines conduct involving suggesting, assisting, arranging, recommending, or intermediary conduct, so it is very easy for marketing companies to drift into credit assistance, credit representation, or regulated activity (for example, you should never use silly words such as 'qualify', 'eligibility', and others, and you should never permit a marketing company to call a lead for this reason). From a marketing perspective - and certainly, for those that operate anything that resembles a comparison engine - that act of ranking or recommended products, applying personalised filtering (by way of a conditional form), returning biased results or any form of qualification whatsoever, those entities are likely to steer outcomes for the consumers, so they are in clear breach. Again, any language or action that has a consumer reasonable believe that the information presented to them is truthful and unbiased when the opposite applies is a clear breach of virtually every piece of consumer legislation ever written.

On the back of what I've just introduced, most digital agencies are introducing clear non-compliance to brokers, and the litigious consequences can threaten the continued operation of a financial business. As is demonstrated by the examples below, ASIC aren't particularly vigilant when it comes to putting an end to the disastrous industry representation (they're busy and under-resourced), but I know they'll read this, and I know that this and other articles will form part of their internal discussions when it comes time to put appropriate measures in place.

The Use of Rates in Mortgage Broker Advertising

We wrote an article in very early January titled "A Look at the Compliance and Performance of Financial Advertising in 2025", and in light of the fact it has remain unpublished, we've renamed it as "The Use of Rates in Mortgage Broker Advertising". The use of rates in advertising can be extremely persuasive, but the current usage by almost all brokers is always non-compliant.

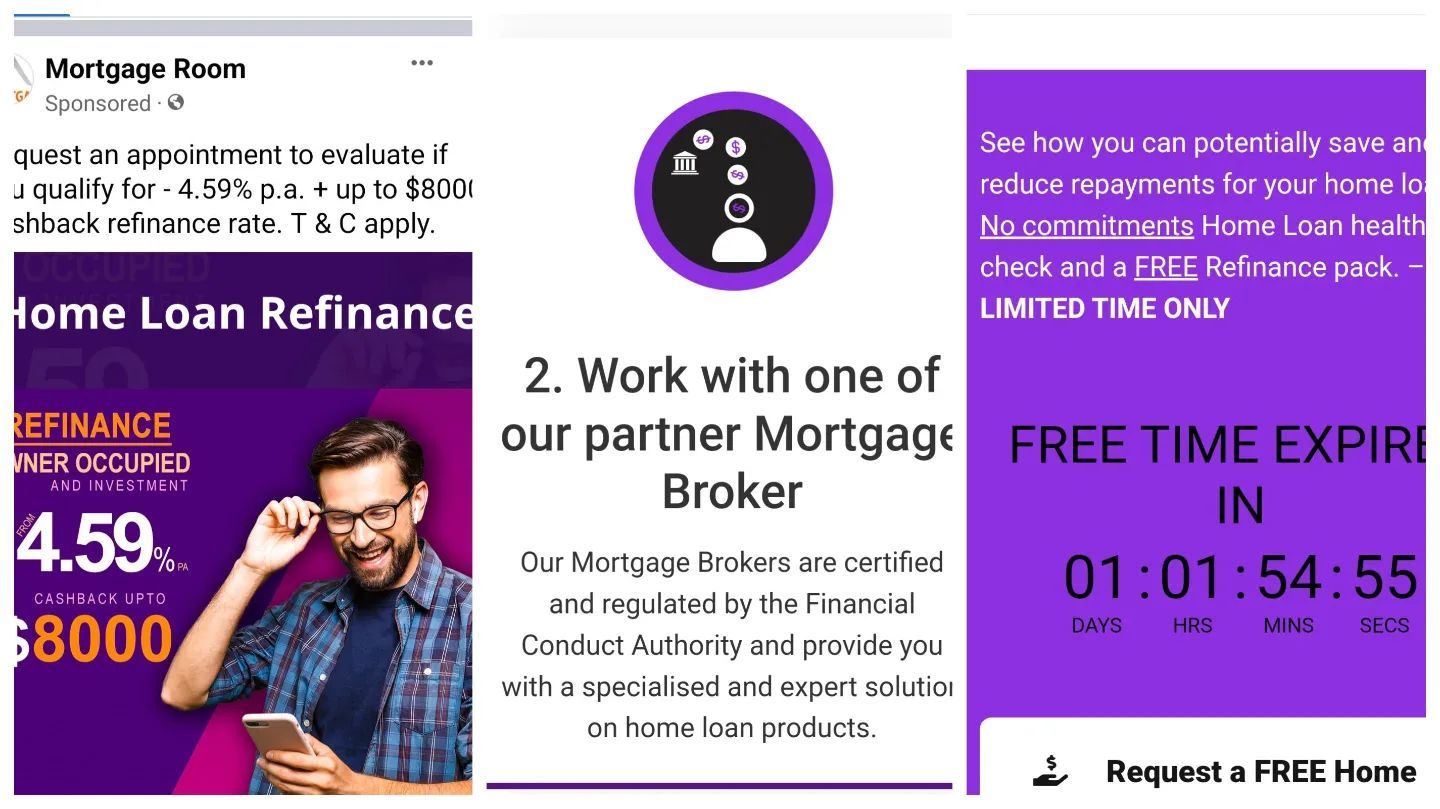

In short, while legislation permits the use of a standalone comparison rate, the rate itself is still required as the true cost of credit. The use of the comparison rate then requires the full APR, comparison warning, appropriate fees and charges, the product and lender name, and a range of other disclosures - so the reality is that both the APR and Comparison Rate are married and almost always shown with the proximity described in legislation. These disclosures and warnings must be printed in the ad copy, the image, and the landing page. As detailed shortly, any quantifiable claim also requires the same rate-based representation with up-to-date and real-world calculations showing how the savings or claims were resolved.

With the exception of our own clients, there isn't a single advert outside of the lenders themselves that represent rates in a compliant manner - not one. It's this oversight on a massive scale that caused us to discuss this single elementary requirement in a standalone article.

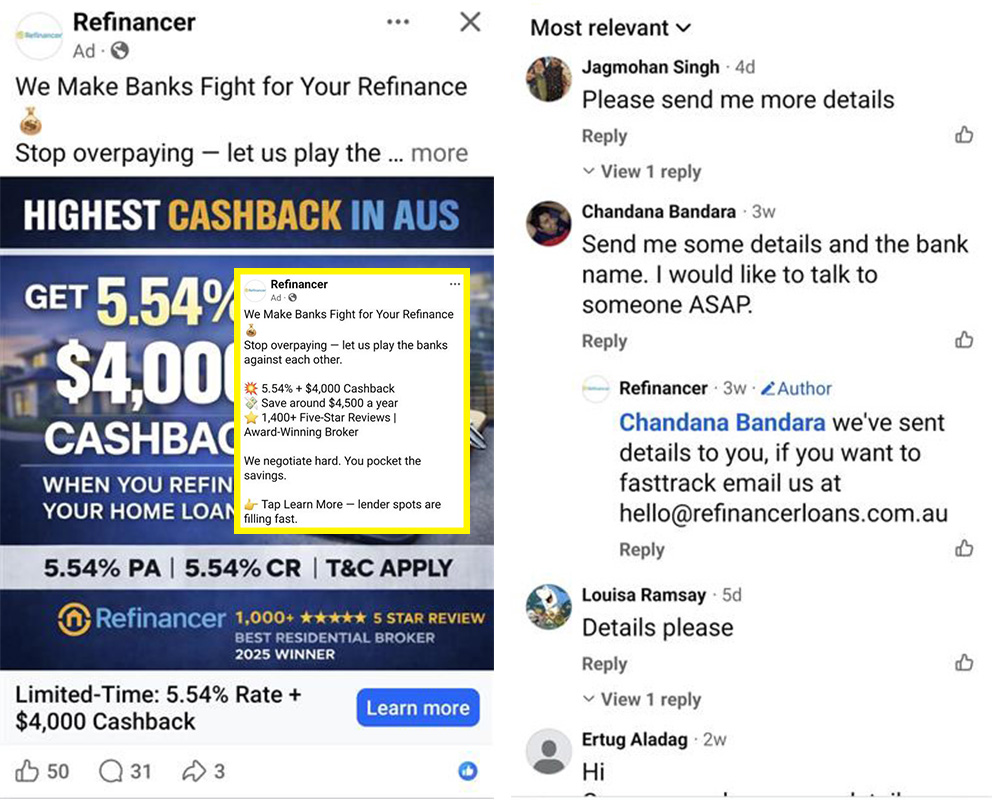

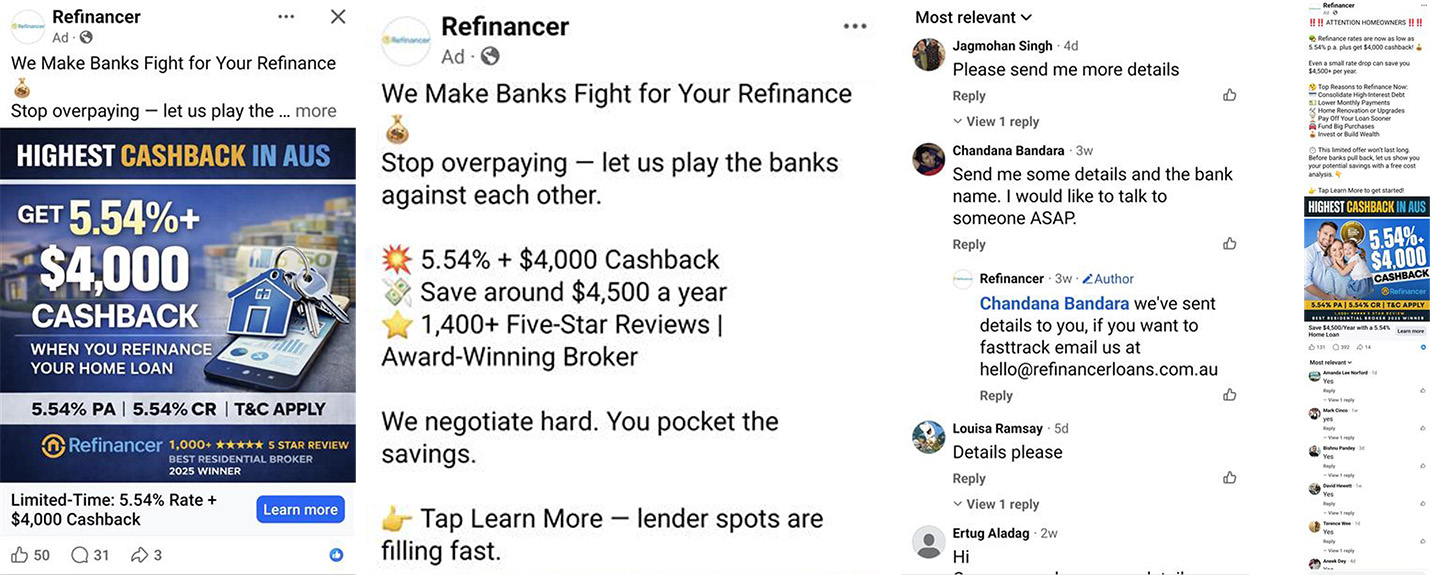

Lack of Industry Education: Refinancier have consistently delivered some of the more non-compliant advertising in the industry, and they've profited enormously off the back of adverts that wouldn't withstand the sniff test if regulatory enforcement was ever applied. Apart from the clear rate and comparison rate issues (lack of everything that's required), they even dodge providing the referenced lender when asked directly - something that is required in the image disclaimer (and wasn't provided in the resulting Facebook lead form). This implies that there is a clear lack of knowledge and education provided to the industry (or its just deliberate rate-baiting malfeasance).

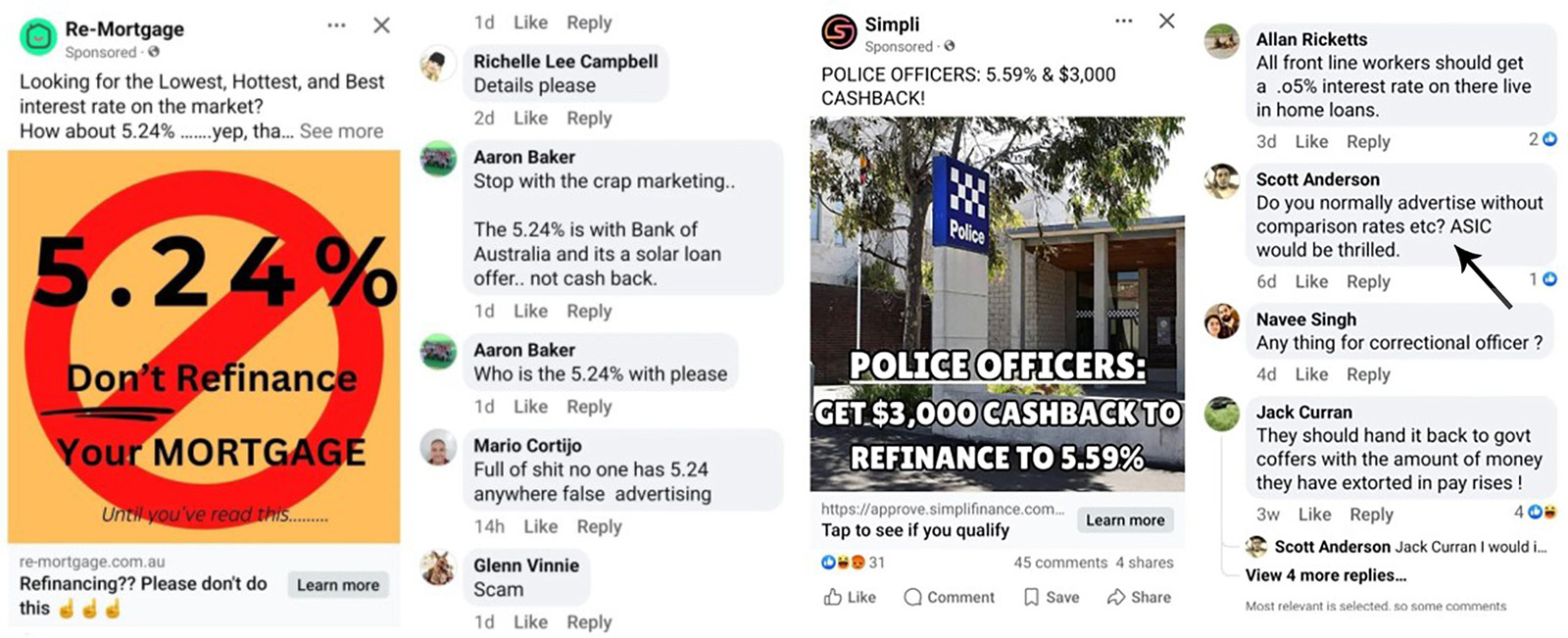

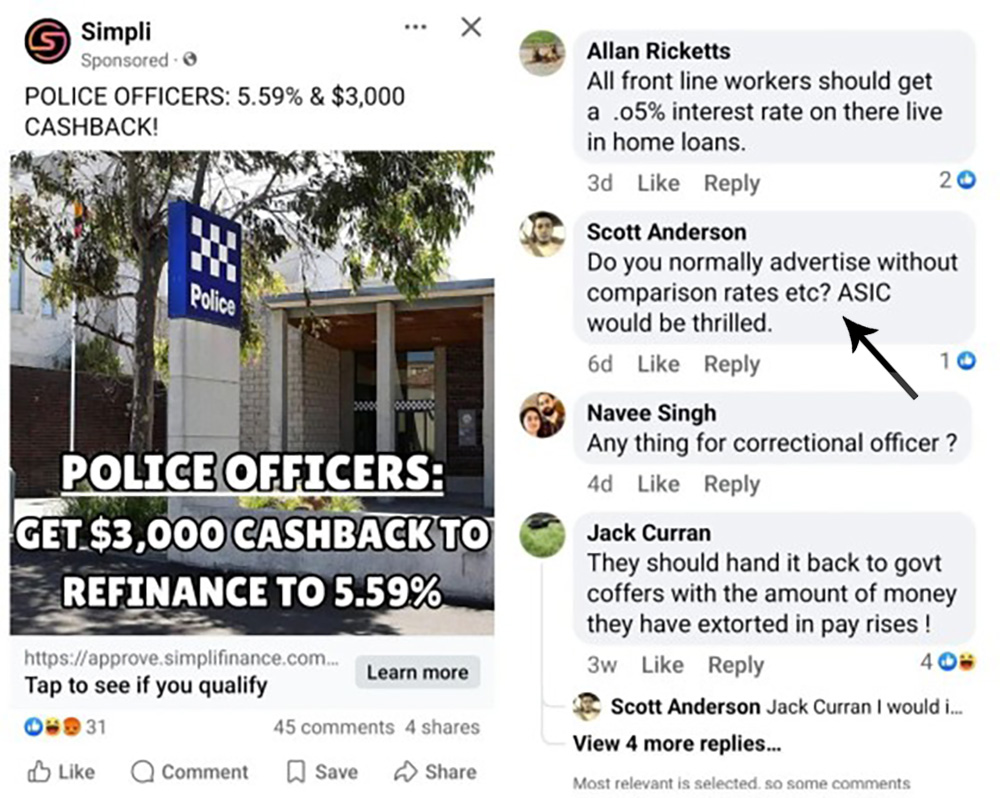

You Will Be Called Out For Your Dodgy Conduct: We have dozens of examples where the comment thread associated with an advert do nothing to contribute towards its legitimacy... and usually has the exact opposite effect .

[image] shortcode. FAQ: "YouTube Modal Thumbnail Images with Image Shortcode".

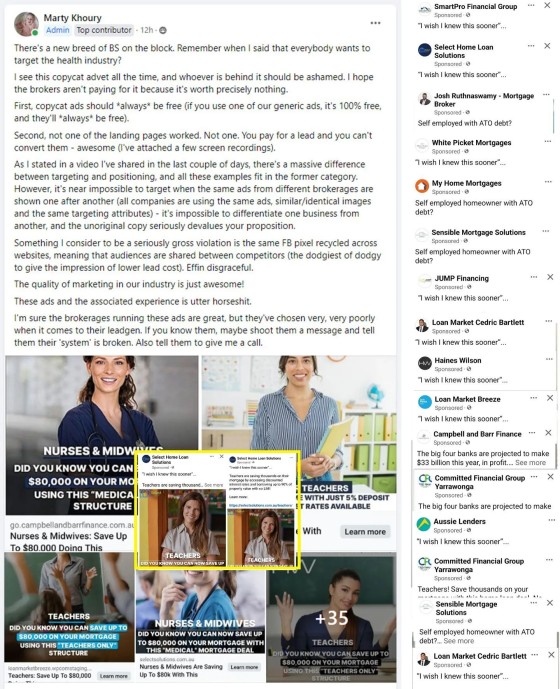

Pictured: The advertisements above were chosen in a pool of several thousand simply because they were shown in the few hours before this article was published - so they're current. None are compliant, and a few of them - such as Refinancier - is of particular concern because of the clear deception funnel that follows (they're also not responding to requests for the lender - required in the missing disclaimer - as a matter of choice, and this breach is discussed shortly).

The article on rates and numeric statements introduces a few hundred Meta advertising screenshots.

As introduced in our various advert reviews (above), there's a segment of the market that is clearly using non-compliant rate-bait to manipulate consumers and have them jump through the dark patters that will have them engage with a form.

Quantitative Statements Need to be Qualified

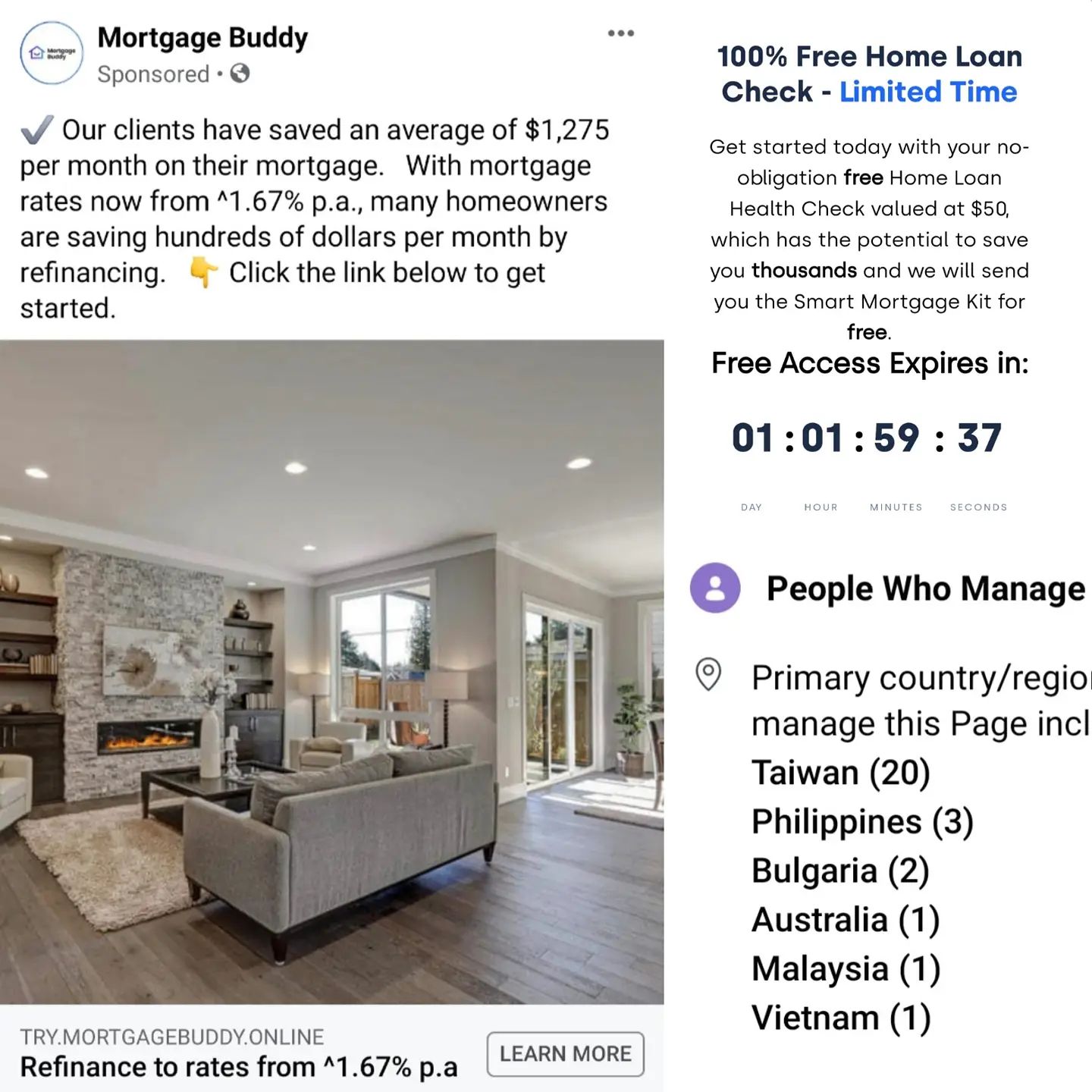

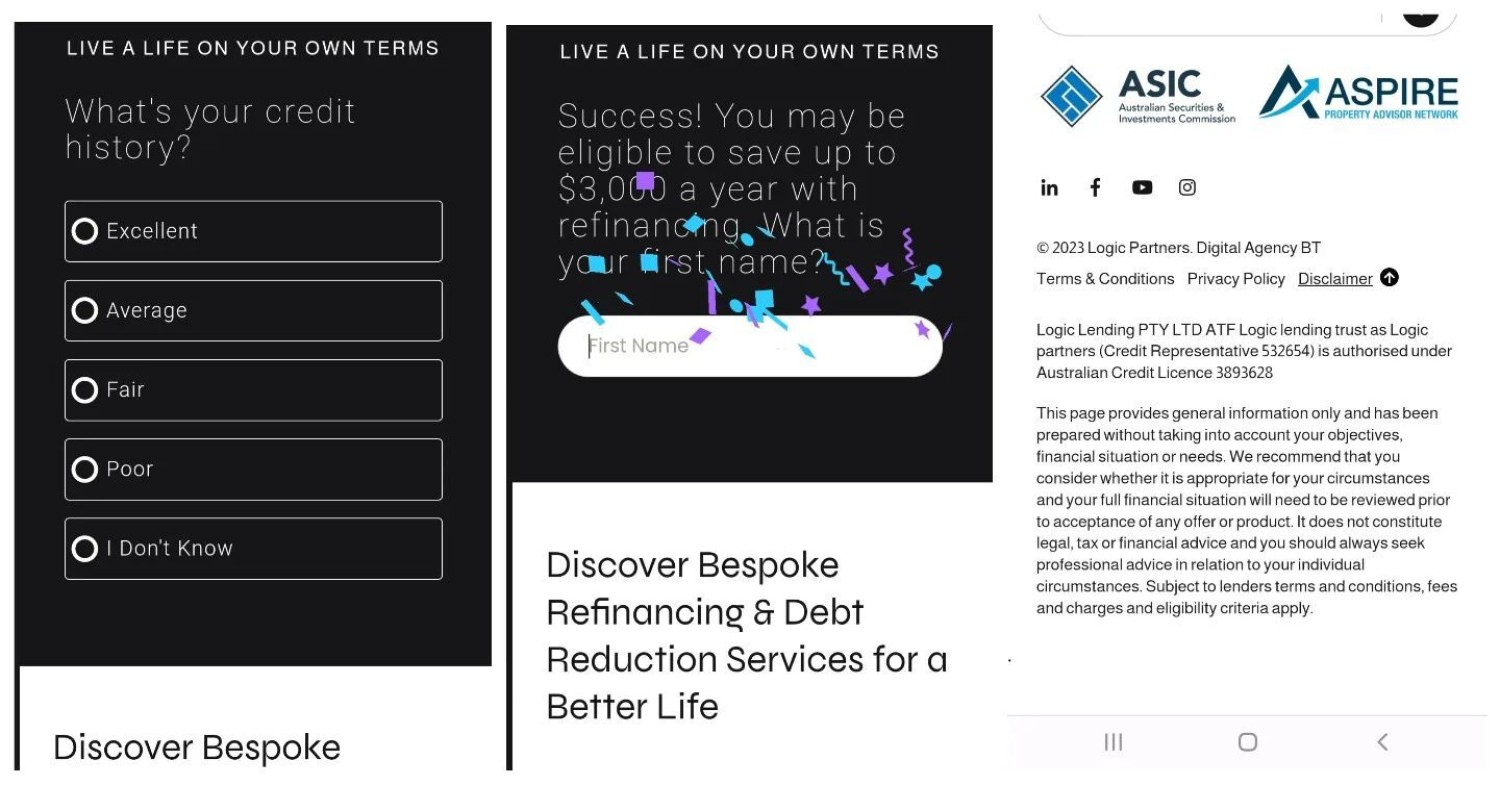

The use of quantitative savings claims in advertising occupies a particularly sensitive position within financial regulation because such claims are not merely promotional statements; they are mathematical representations that necessarily imply the existence of an underlying financial comparison. When an advertiser states that a consumer could "Save $90,000", "Save $1,000 per month", "Reduce your repayments by $500 per month", or similar, the claim is fundamentally different from a subjective statement of opinion or a general marketing slogan. A quantified savings representation communicates to the ordinary consumer that a calculable financial benefit exists and that the advertiser has performed, or is capable of performing, a comparative analysis capable of substantiating that figure. The legal significance of this distinction cannot be overstated. A quantitative claim is not merely a statement about possibility; it is an implied representation derived via real-world and accurate arithmetic.

From a regulatory perspective, a savings claim necessarily raises the question: compared to what? Savings cannot exist in a vacuum. A statement that a borrower can save $90,000 requires the existence of at least two financial positions: the consumer's current position and an alternative position against which the claimed benefit is measured. This comparative framework inevitably imports interest rates, fees, charges, loan terms, repayment assumptions, and other credit variables into the representation, whether or not those variables are expressly disclosed in the advertisement. Consequently, many quantitative savings claims are, in substance, indirect interest rate comparisons. The consumer may not see the underlying rates, but the advertiser has necessarily relied upon them to generate the savings figure. The legal challenge arises because the numerical outcome often becomes the dominant message of the advertisement while the assumptions that generated it remain obscured or built on the back of outdated or flawed numbers.

This is where the National Consumer Credit Protection framework becomes particularly relevant. The National Credit Code recognises that interest rates possess extraordinary persuasive power in consumer decision-making and therefore imposes specific obligations regarding the disclosure of annual percentage rates, comparison rates, prescribed warnings, prominence requirements, and associated assumptions. The rationale underlying these provisions is that consumers should not be induced by numerical credit representations without sufficient contextual information to understand their significance, and this reference must be included within the advertisement itself (and not hidden in the footer of a landing page in isolation). Although an advertisement may attempt to avoid direct reference to a rate by focusing solely on a savings figure, the economic reality is that the savings figure is itself a derivative of one or more interest rate assumptions. The numerical claim cannot exist independently of the credit calculation that produced it. In practical terms, an advertiser cannot honestly assert that a borrower may save $90,000 without having first selected a replacement interest rate, repayment profile, loan term, fee structure, and other variables capable of generating that outcome.

How We Do It: A quantitative statement will change over time, and the arithmetic used to calculate results will vary since the rate, comparison rate, and fees used to resolve the savings will change. We use live data, our LMI API, and up-to-date lender product data sourced via the lowest rate from those that support the implied policy exemption (such as Nurses, Doctors, or Police), and we build out the calculation in real time (sourcing the product, lender, fees and associated charges). The number is rounded down and will be represented appropriately in the advert. When you have a hundred landing pages, there's a clear technical debt associated with hard-coded information, so dynamic calculations in your footer and on landing pages are the only suitable method of staying compliant). The API used to return the above information based on any claimed 'saving' is freely available. Your calculations should never be outdated or determined based on old information. Read more about disclaimer functionality in an article with the working title of "The Landing Page Module is Updated to Adventus".

The legal risk therefore extends beyond the mere accuracy of the headline figure. A savings claim implicitly communicates that the advertiser has undertaken a real-world and entirely accurate comparative assessment using assumptions that are reasonable, representative, and capable of substantiation. Under section 18 of the Australian Consumer Law and section 12DA of the ASIC Act 2001 (Cth), misleading or deceptive conduct is assessed not by technical parsing of individual words but by reference to the overall impression conveyed to an ordinary consumer. The dominant message communicated by a headline savings figure is often far more powerful than any accompanying disclaimer. Consumers do not naturally interpret a claim such as "Save $90,000" as a highly conditional mathematical possibility applicable only to a narrow subset of borrowers. Rather, they interpret it as evidence of a substantial and realistic financial opportunity. Behavioural economics and consumer psychology demonstrate that large numerical claims operate as cognitive anchors, establishing expectations before consumers engage with qualifications or assumptions. Once a consumer has internalised a large savings figure, subsequent disclosures exert limited or nil corrective influence.

The psychological phenomenon described above is one of the principal reasons financial advertising attracts heightened regulatory scrutiny. Numerical claims are uniquely persuasive because they create an impression of objectivity, while statements such as "great rates" or "competitive loans" are understood by consumers as promotional language, a claim that a borrower can save a specific dollar amount carries an implied aura of precision, calculation, and factual certainty. Consumers tend to assume that quantified statements have been derived through rigorous analysis. The specificity of the figure itself functions as a credibility signal. A claim of $90,000 appears less like advertising rhetoric and more like a mathematical conclusion. Regulators recognise that this perceived precision increases the risk of consumer reliance and therefore increases the importance of transparency regarding the assumptions underpinning the calculation.

The interaction between savings claims and comparison rate legislation becomes particularly significant where the savings outcome is derived from an advertised credit product. If the savings calculation relies upon a particular interest rate or loan structure, the advertiser may struggle to argue that the rate itself is not part of the representation being made to consumers. The savings figure is merely the visible manifestation of the underlying rate differential. In substance, the advertisement is communicating the economic consequences of a particular credit product's pricing structure. To permit advertisers to promote substantial quantified savings while withholding the underlying rate assumptions would undermine the policy objectives of the comparison rate regime, which seeks to ensure that consumers receive sufficient information to evaluate the true cost of credit. Although the legal analysis will depend on the precise wording and structure of the advertisement, there is a strong argument that any quantitative savings claims effectively communicate rate-based benefits while attempting to avoid the disclosure obligations that would ordinarily accompany direct rate advertising.

There is also a broader integrity issue embedded within these representations. Financial services regulation increasingly recognises that consumers engage with advertising through behavioural cues rather than legal analysis. The law therefore focuses not merely on literal compliance but on the substance of the consumer experience. Where an advertiser prominently displays a large savings figure while obscuring the assumptions, rates, fees, loan terms, eligibility criteria, or comparative basis necessary to evaluate the claim, the risk is that consumers are influenced by the outcome without understanding the inputs that generated it. This asymmetry of information undermines informed decision-making and strikes at the core rationale underpinning Australia's consumer protection framework.

Ultimately, quantitative savings claims occupy a unique regulatory category because they are simultaneously marketing statements and mathematical assertions. Every dollar-saving representation is the product of an underlying credit analysis, whether disclosed or not. The larger and more prominent the claimed saving, the greater the need for transparency regarding the assumptions that produced it. To permit large numerical benefits to be advertised without corresponding scrutiny of the rates, fees, loan terms, and comparison methodology that generated those figures would allow advertisers to communicate the most persuasive component of a credit comparison while withholding the information necessary for consumers to assess its validity. The regulatory framework, viewed as a whole, is designed precisely to prevent this outcome. Its focus on comparison rates, prominence requirements, prescribed warnings, and misleading conduct principles reflects a recognition that consumers are often influenced less by the mechanics of a financial calculation than by the headline number itself, and that meaningful consumer protection requires scrutiny of both.

"See if You Qualify" and Similar in Advertising

Those common phrases in finance ads - such as "See if you qualify", "Check Eligibility", "See how much you can save" - all sit in a very interesting and problematic zone in financial advertising because they rely heavily on implied outcomes rather than explicit promises. What matters, legally and psychologically, is not the literal wording, but the expectation they create in a reasonable consumer's mind at the moment of interaction. As I've said hundreds of times, if no immediate assessment is made, use alternate wording, and steer well clear of any phrase that'll land you in a world or litigious pain.

Qualification, Suitability, Eligibility, and other similar words, imply there is a defined set of criteria, the system will assess the user against those criteria, and a meaningful tailored outcome will be provided - exasperate by the fact you're asking questions that should return a result.

See how much you qualify for: While sentence-final prepositions are a natural and well-established feature of English, the sentence of "See how much you qualify for" sounds incomplete and awkward, yet it is on hundreds of adverts. To give you an idea of how others try and polish their turd by way of our advice, see how long it takes before that non-compliant sentence is removed from your form. Calls-to-action such as "See how much you qualify for" or "Find out what you're eligible for" can often sound more conversational and accessible than grammatically restructured alternatives, and the language may reduce cognitive effort for readers and improve message comprehension... but the cited examples aren't two of them. The reason for this rant? The use of the words 'qualify' or 'eligible' (in company with others) are bogus - don't use them.

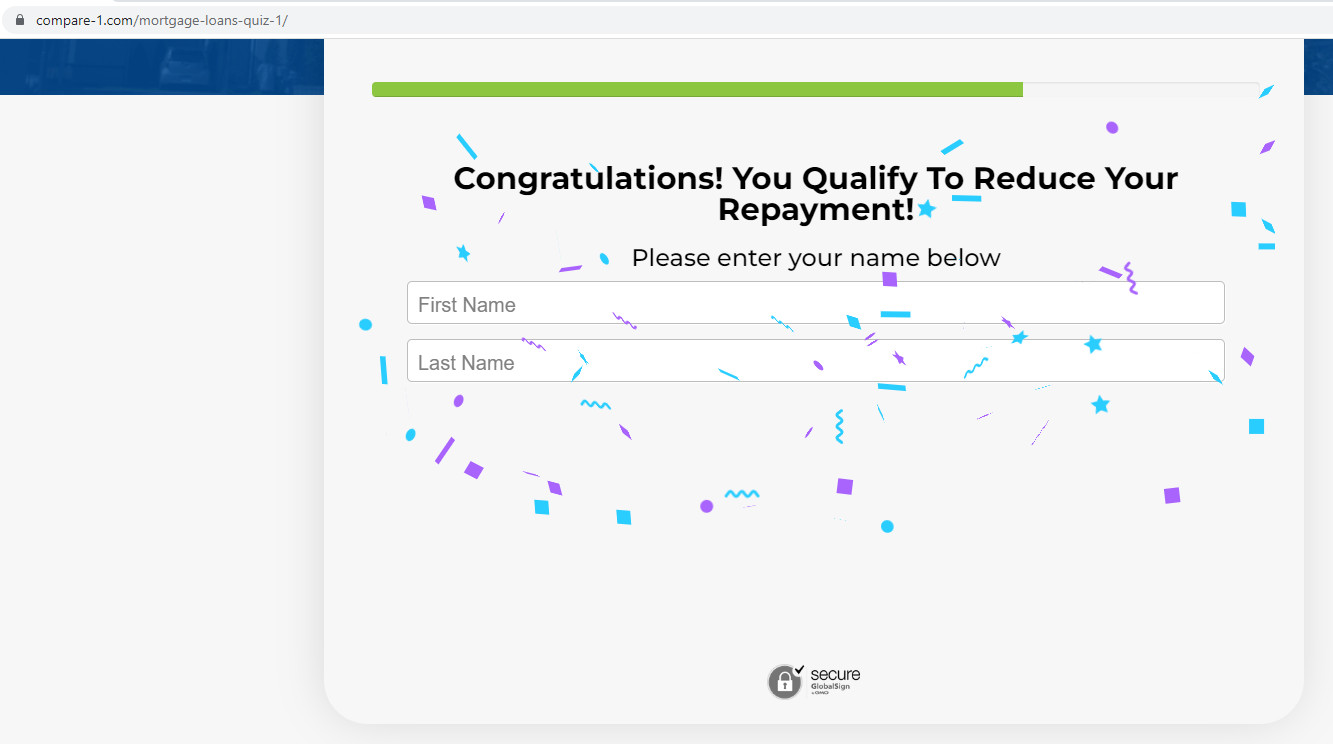

If a result is returned, the wording and subscription experience itself is highly effective in a value-based booking funnel because it leverages authority bias (there is a "judge" of eligibility), reduction of uncertainty, and it provides a service-based low-friction curiosity ("I’ll just check"). If any expectation for results were created and you simply send a user to a calendar, you have based your entire experience on a fraudulent claim - not the ideal first digital handshake. What I've just described is not compliant if there is no real eligibility assessment, outcomes are not actually determined by inputs, the result is always a contact asset, or the “qualification” is purely a lead capture threshold or gate. If the initial claim isn't supported, you're not providing a service-based result, your initial claim translates to "we will collect your details and contact you". This gap is what regulators focus on under the ACL s18 and ASIC Act s12DA principles (overall impression and implied meaning).

We Accept Responsibility for the Current Flow: We introduced a stepped compliance form around 2010 (at a time when Facebook leads cost 40c), and we've had multiple versions of various Fact Find Reports since then. However, our forms were designed on Page 2 of the subscription funnel, and they were value based in that they would send the user a customised report upon completion - they weren't designed to somehow gamify through inconvenience or garnish user data that wasn't entirely relevant. A form should only be used if it adds value back to the user. The Purpose of the subscription funnel is to qualify you - not the client... and lead capture masquerading as result-driven experiences erode any early established trust.

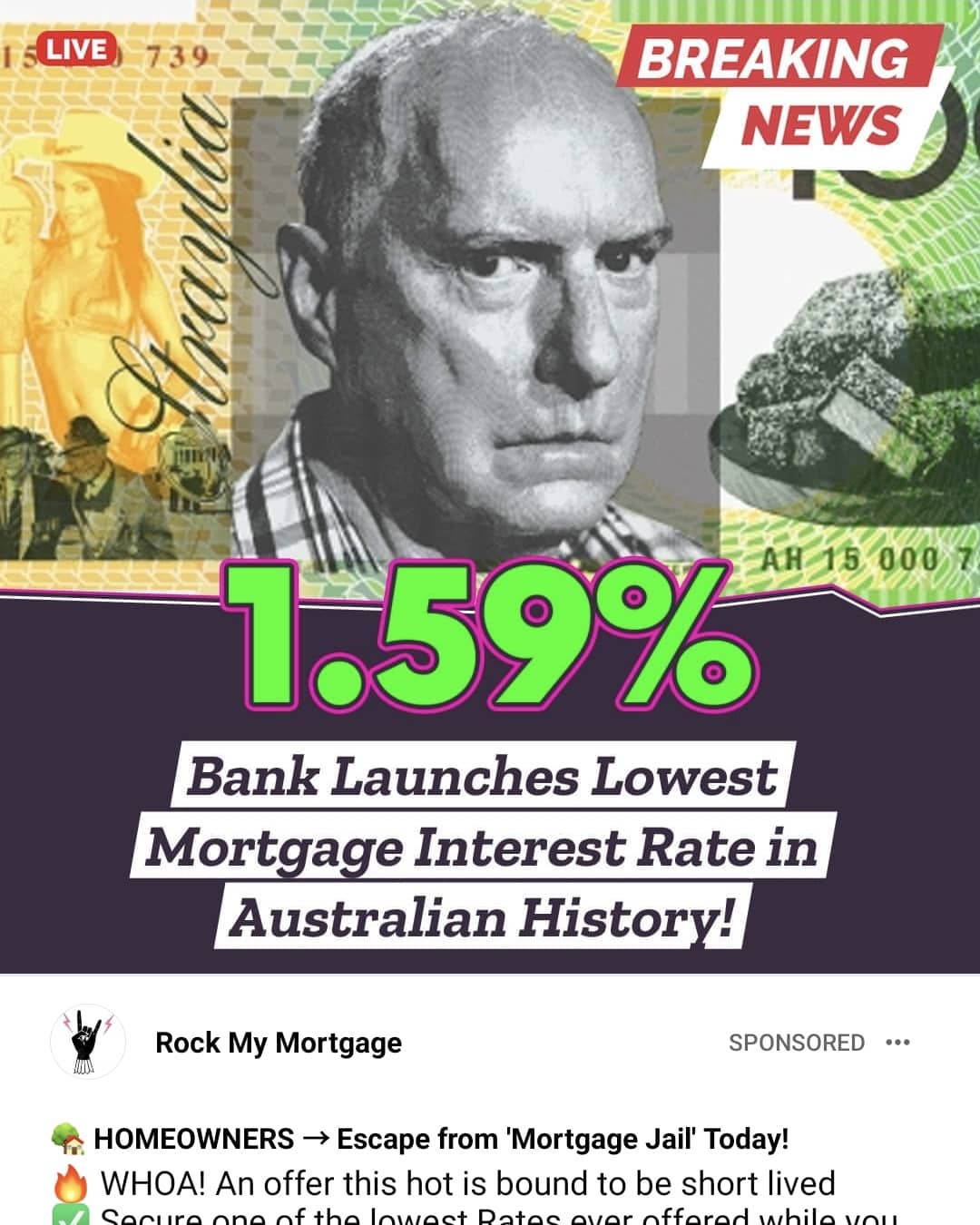

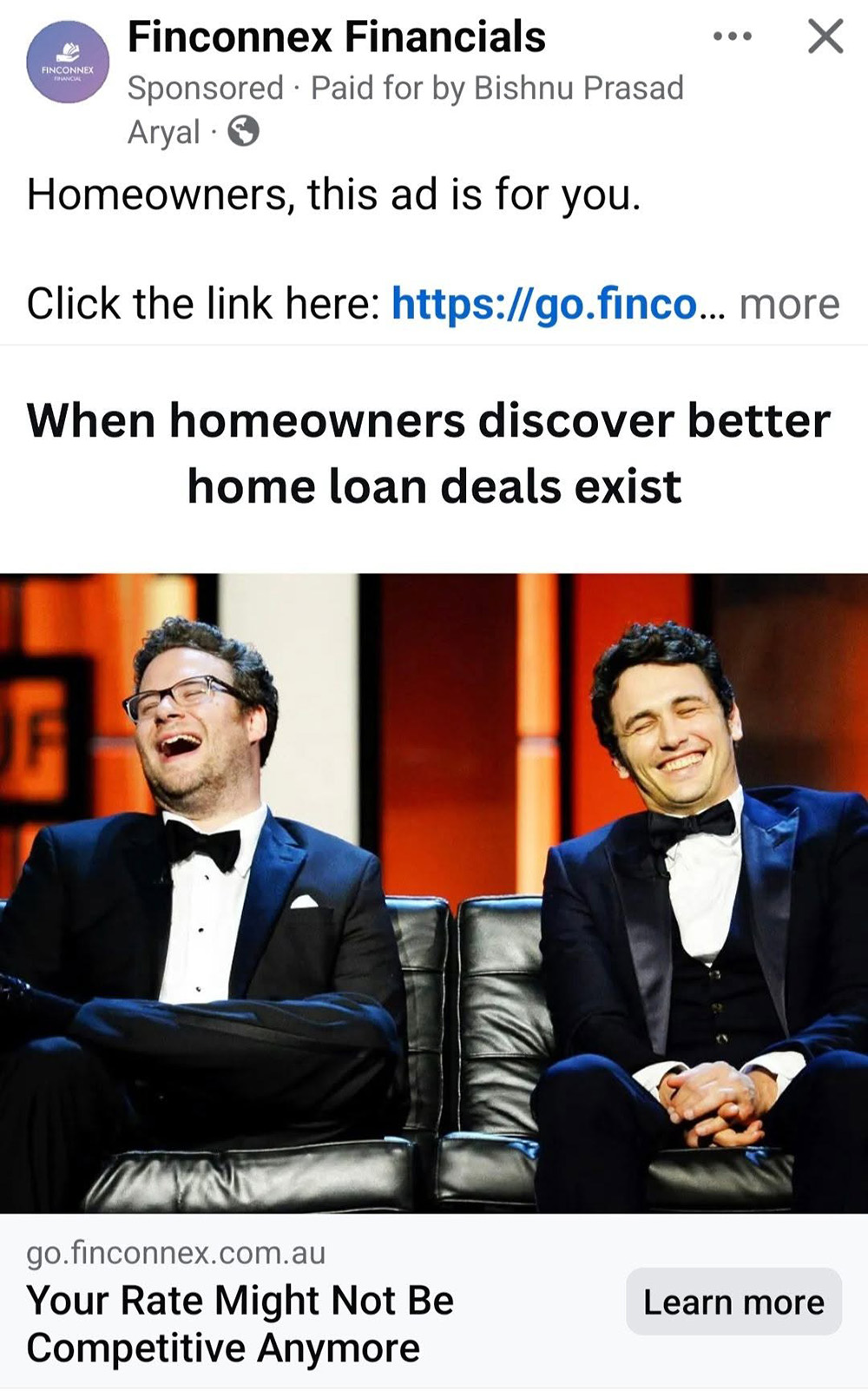

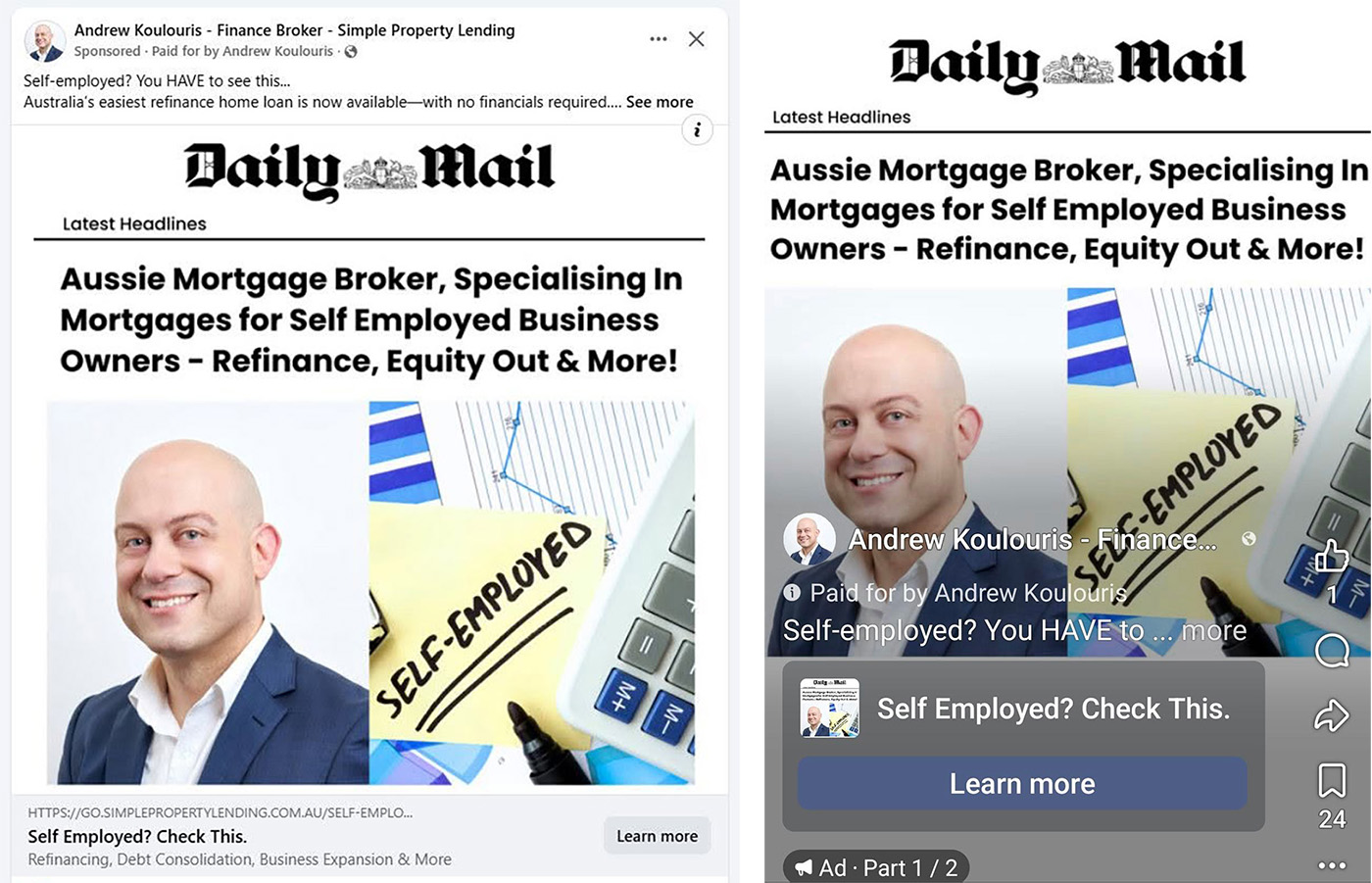

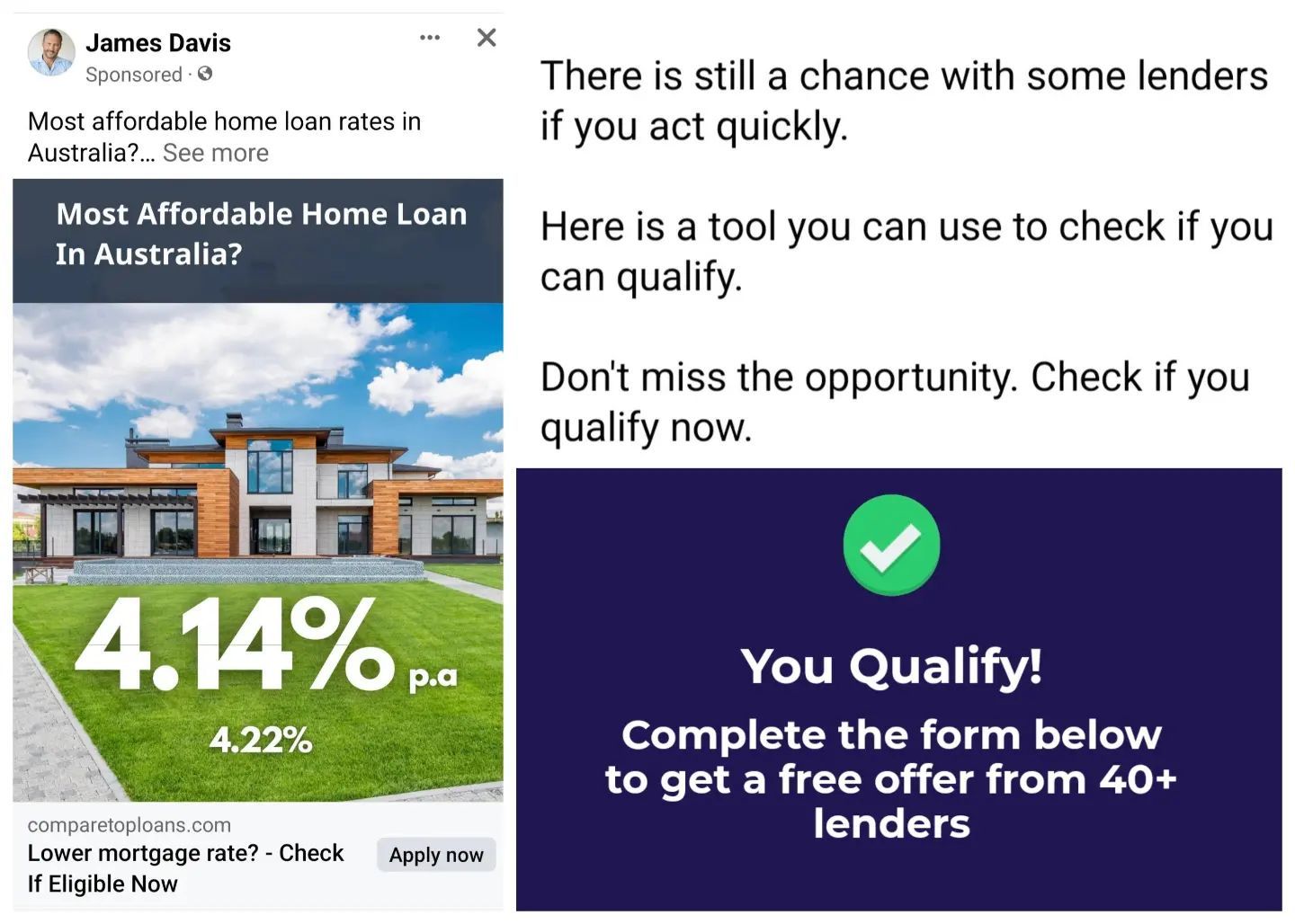

Pictured: The ads pictured are examples sourced form several thousand where an implied quiz would return qualification information. This is lead capture disguised as value There are very clear issues associated with these ads, such as the 'Breaking News' used in one of them - the issue is not the phrase itself, but whether its use contributes to a misleading overall impression in contravention of the ASIC Act and Corporations Act (is it really breaking news?). Fake news-style ads are introduced later (in brief). The latter two forms are from Broker Grow - he uses a fake "quiz" qualification or 'eligibility' to drive users into a form (pages coming from BG are some of the most non-compliant in the industry). As described in the next section, it's ads from Bizleads and other like-minded ignoramuses - and those brokers that use their service - that are deliberately lying to customers.

Australian Consumer Law (ACL), the ASIC Act, and the National Consumer Credit Protection regime are enforced largely on what is implied, what a reasonable consumer believes will happen,

how the funnel is designed psychologically, and whether the "results" claim materially influences behaviour. The crucial issue is not merely whether the statement is literally false; the real legal test is the overall impression is conveyed to an ordinary consumer. If a user is asked for mortgage balance, interest rate, property value, repayment amount, income, lender details, loan term, or postcode - and the funnel entry implied results in any way whatsoever - there's a clear expectation that results will follow. The UX and applied language usually states that you are calculating something, results are being generated, personalised savings are about to appear, or you are receiving a personal analysis.

The three short advert reviews introduced earlier are more offensive than most since they return fake results and qualification - thus reinforcing their experience as nothing more than fraud disguised as lead capture. They break about every finance regulation ever written.

The Term "Quiz" and "Survey" to Describe the Lie

Many adverts use the disingenuous term of "quiz" or "survey" to describe the nature of the questions presented to consumers. The problem? It's a lie. Used in the creative, copy, or landing page, the use of the terms is legally problematic in cases where those descriptors create an implied representation that the user is engaging in a genuine evaluative or analytical process, when in substance no such process exists. As stated a few times, under section 18 of the Australian Consumer Law (Competition and Consumer Act 2010 (Cth), Schedule 2) and section 12DA of the ASIC Act 2001 (Cth), liability turns not on literal wording but on the overall impression conveyed to a reasonable consumer, including implied meaning arising from structure, sequencing, and interface design. In this context, “quiz” implies scoring, classification, or diagnostic output, while "survey" implies meaningful aggregation and analysis of responses; both therefore carry a strong expectation that user inputs—particularly sensitive financial data and will be processed into a discernible result. Bottom line: When a financial funnel is framed as a “quiz” or “survey”, it carries with it a set of well-understood consumer expectations grounded in ordinary language use... so use language that is actually consistent with the funnel experience.

Where the above expectations are reinforced by UX patterns suggesting calculation or personalisation, but no substantive result is ultimately produced - absolutely ubiquitous in the 'systems' introduced by poor funnel architects - and the primary function is instead the capture contact details or lead qualification, the terminology becomes part of a misleading representation as to the nature and purpose of the service itself.

Video: 'A General Introduction to Belief's Stepped Comparison Mortgage Forms': The video above shows the significant difference between the utter mediocrity pushed to market disguised as a "system", and we show just how powerful and persuasive a stepped form can be when functional, gamified, and lender comparison elements are applied. The linked video looks at stepped forms within your website, and a scheduled article shows how the conditional forms, conditional redirections, and single-page transactions are applied on landing pages, and how any why our experience outperforms others in seriously significant ways. A distinguishing characteristic of the Better Funnel Method is its rejection of the increasingly common tendency for digital experiences to be dictated by the limitations, preferences, or convenience of the underlying technology stack. In many contemporary implementations, the development process becomes an exercise in adapting consumer behaviour to fit the constraints of software platforms, customer relationship management systems, automation workflows, or analytics frameworks. The result is a form of technological determinism in which the architecture of the funnel is shaped not by how human beings naturally evaluate information, build trust, manage cognitive load, or make decisions, but rather by what is easiest and 'cheapest' to implement, measure, or automate. This represents what may be described as a "tail wagging the dog" phenomenon, whereby the enabling technology assumes primacy over the psychological and behavioural objectives it was intended to serve. The Better Funnel Method inverts this relationship entirely. It begins with a detailed examination of human cognition, behavioural economics, decision science, and consumer psychology, recognising that successful conversion pathways are fundamentally human systems rather than technical systems. Every stage of the experience is therefore constructed around the way individuals process uncertainty, seek reassurance, establish credibility, compare alternatives, and progressively develop commitment. Technology is viewed not as the architect of the customer journey, but as a subordinate mechanism whose sole purpose is to facilitate a psychologically coherent and behaviourally optimised experience. This distinction is critical because mortgage conversions are managed with compliant perceptions, emotions, expectations, and mental models. Consequently, the effectiveness of a funnel is not determined by the sophistication of its underlying technology, but by the extent to which that technology unobtrusively supports the natural processes through which borrowers evaluate risk, establish trust, and arrive at decisions. By placing seamless and effortless behavioural function ahead of best-practice technical implementation - all of which functions out of the box - the Better Funnel Method seeks to create conversion environments that are aligned with the realities of borrower decision-making rather than the operational preferences of software systems, resulting in experiences that are simultaneously more intuitive, more persuasive, and ultimately more effective. Bottom line: what we've described converts far more clients. Read an article titled "Stepped Mortgage Forms That Deliver Comparative Lender Results" with other information available in our FAQs.

Regulators have consistently treated such divergences between perceived functionality and actual operation as capable of constituting misleading or deceptive conduct, particularly in financial services contexts where reliance on implied analytical integrity is high and disclaimers or downstream explanations cannot cure a dominant contrary impression created at the point of engagement.

Do not use the terms "quiz", "survey", or similar, if your experience dees not return results. We have thousands of examples of this practice in our public Facebook Group.

Overlap with the Privacy Act (1988)

The Privacy Act (1988) is focused primarily on how personal information is collected, whether collection is fair and lawful, whether people are told what it’s for, and how it is used and disclosed. The key rule for lead capture is that an organisation must only collect personal information if it is reasonably necessary for its functions or activities, and the collection is lawful and fair (or honest and transparent), and it is the latter point where the Privacy Act overlaps with other financial legislation. The dual-risk scenario occurs when users are misled about the nature of the service and personal financial data is collected under that misrepresentation and the privacy disclosure does not clearly explain the true purpose. In company with ACL and other breaches, the regulators may view collection as misleading conduct (primary issue) or unfair or non-transparent data collection (secondary issue). Bottom line: if a user expects results and you redirect to a calendar, you've broken the law. Of course, I've never actually seen a clear disclaimer on why the data is collected or how the sensitive information is handled.

Where the collection of any financial data becomes legally significant is in scenarios where the UX presents a structured input flow - such as income, property value, existing mortgage balance, interest rate - combined with language implying that a computational assessment is actively occurring, but where no meaningful calculation is ultimately performed, or where the output is withheld and replaced with a lead capture mechanism. In such circumstances, the legal risk does not arise from the mere collection of data itself, but from the inducement under which that data is provided. If a reasonable consumer is led to believe that they are engaging with a functional analytical tool that will return personalised financial insights, yet the true operational purpose is primarily or exclusively lead generation, then the conduct may be characterised as misleading as to the nature of the service being supplied. This is particularly relevant in financial services contexts, where ASIC regulatory guidance (including RG 234) and general case law. What I've just described is the primary method that underpins dodgy lead generation websites, and your mere association with a known criminal undertaking exposes you to potential legal consequences.

Using AI Supported Comparisons In Advertising

Claims that an “AI comparison,” “AI analysis,” or “AI-powered assessment” is being performed, but the outputs are in reality generic, repetitive, non-personalised, or not meaningfully generated through artificial intelligence at all, the legal exposure can become substantial under parent legislation. The issue is not merely technological exaggeration; it is the potential misrepresentation of the nature, sophistication, and functionality of the service being offered to consumers. Under section 18 of the Australian Consumer Law and section 12DA of the ASIC Act 2001 (Cth), a business must not engage in conduct that is misleading or deceptive or likely to mislead or deceive. Importantly, these provisions apply not only to explicit factual falsehoods, but also to implied representations created through terminology, branding, interface design, and technological framing. The use of the term “AI” carries a powerful implied representation that a genuine computational process is occurring - namely that user-specific inputs are being analysed dynamically, algorithmically, and intelligently to generate tailored comparative outcomes.

Where that representation is false in substance, regulators may characterise the conduct as misleading as to the nature, characteristics, or capabilities of the service itself. If consumers are induced to provide detailed financial information under the impression that an advanced analytical system is evaluating their circumstances, but the outputs are effectively pre-scripted, generic, or materially disconnected from the inputs provided, then the “AI” claim risks becoming a form of technological misrepresentation. The legal significance is heightened where the AI framing is central to the consumer’s decision to engage, because the sophistication implied by artificial intelligence can materially influence perceptions of accuracy, objectivity, personalisation, and trustworthiness. In financial services contexts, those implications are especially sensitive because consumers may reasonably assume that AI-driven comparisons are more comprehensive, data-informed, or unbiased than ordinary marketing funnels.

Regulators globally, including ASIC and the ACCC, are increasingly attentive to what is often described as “AI washing” — the practice of overstating, fabricating, or mischaracterising the use of artificial intelligence in commercial products and services. The concern is not whether a business uses some form of software automation, but whether the overall impression created by the “AI” claim matches the actual operational reality. If identical “personalised” savings estimates, rankings, or eligibility outcomes are repeatedly returned irrespective of materially different consumer inputs, that pattern may become evidentiary support for the proposition that no meaningful AI-driven analysis is occurring at all. In such circumstances, the representation is no longer merely aspirational marketing language; it may constitute a misleading statement about the functional capability of the product.

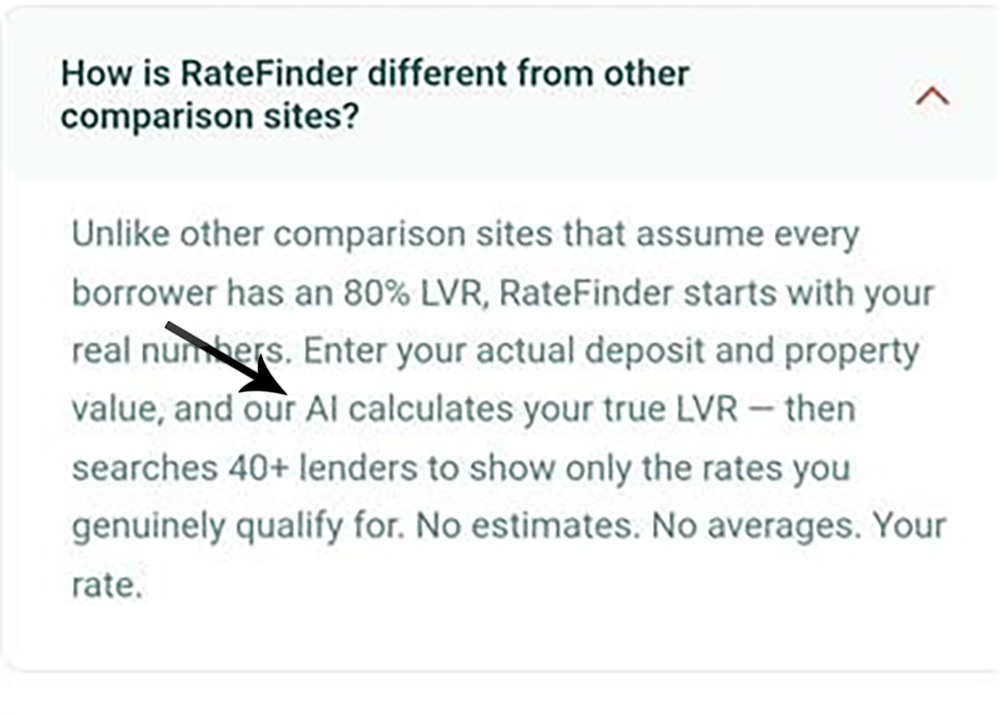

Rate Finder AI: Rate Finder make some bold and featured claims in multiple locations regarding the use of AI in their 'quiz'. They claim their "Advanced" AI is Australia's "Number 1" AI Search Engine, and then go on to compare their results with 'traditional platform'. Their AI claim is the calculation of an LVR - something my middle daughter does in year 5 math. We jumped through the hoops multiple times with the same results returned over and over, and there was no evidence whatsoever that AI played a part. To the best of my knowledge, our BeNet AI Comparison Engine (Version 4) is the only AI-supported platform in the market. In order to return AI results, one must determine a range of borrower attributes before returning a result, such as their renumeration in localised currency, their principal country of work (and residency), their occupation, and dozens of other pieces of information that can be supplied in plain text as a description, and the engine itself needs to resolve that data and return results washed against comprehensive policy information. The calculation of LVR is as far removed from AI as Donals Trump is from the sexiest man alive. This is one of dozens of examples where AI is claimed but played no part whatsoever. The use of the phrase "genuinely qualify for" and unsupported rate data is a concern that is - as described earlier - a minefield of compliance headaches.

Legally, one of the most dangerous aspects of unsupported AI claims is that they often amplify the seriousness of the underlying conduct. A misleading “AI comparison” representation does not merely suggest that consumers are receiving a result; it suggests that they are receiving an advanced, data-driven, technologically sophisticated result generated through computational AI-based intelligence. The AI claim can deepen the consumer’s reliance on the output and strengthen arguments that the conduct materially influenced decision-making. Courts assessing misleading conduct look at the overall impression conveyed to an ordinary consumer, and in the current technological climate, references to AI carry extraordinary persuasive weight. They imply innovation, objectivity, analytical depth, and computational legitimacy. If those qualities are absent, the disparity between represented capability and actual functionality can become legally significant.

Marketing AI Claims: Many marketing companies claim that their service includes AI elements that do not exist, and we've created an extensive analysis of those claims that we'll publish soon in an article titled "Your Marketing Company is Lying to You". In a standard form used on most websites, and the standard flow used by almost all brokers, no AI is employed.

The fact that some form of backend logic or automation exists is not necessarily sufficient to neutralise the risk. The legal question is not whether any software process occurs, but whether the representation reasonably conveyed by the term “AI comparison” is substantively true. A basic rules-based form, static lead-routing script, or generic conditional output may fall far short of what ordinary consumers understand “AI-powered comparison” to mean. As regulators increasingly focus on digital manipulation, behavioural advertising, and technological representations, unsupported AI claims in financial marketing are likely to attract escalating scrutiny, particularly where they are used to legitimise the collection of sensitive financial information or to create an illusion of personalised analytical sophistication that does not genuinely exist.

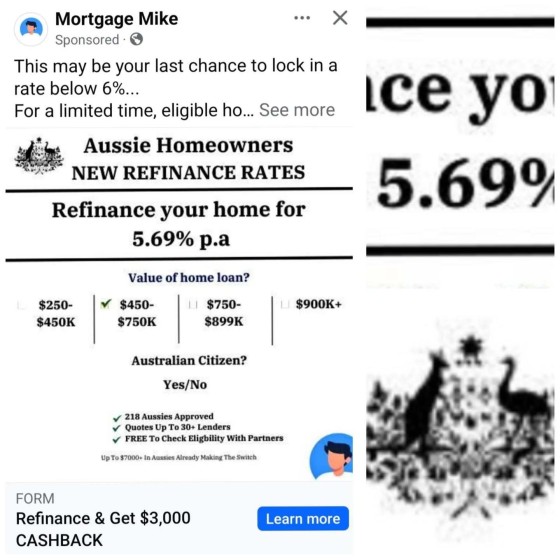

Is Your Rate Under 6%, and Rates from 5.XX%

Statements such as “Is your rate over 6%?” or “Rates from 5.XX%” appear deceptively simple, yet in financial advertising they raise a number of significant legal and regulatory concerns because of the way consumers interpret numerical claims in mortgage contexts. Under section 18 of the Australian Consumer Law and section 12DA of the ASIC Act 2001 (Cth), the critical issue is not merely whether the wording is technically defensible, but whether the overall impression conveyed to an ordinary consumer is misleading or likely to mislead. In mortgage advertising, even seemingly small ambiguities around rates can materially influence consumer behaviour because interest rates operate as the dominant decision-making signal within the advertisement.

The phrase “Is your rate over 6%?” is often used to induce anxiety, urgency, or perceived overpayment by implying that rates materially below 6% are realistically available to the consumer. Legally, the risk emerges where the advertisement creates a broad impression that consumers are likely to qualify for significantly lower rates when, in reality, only a narrow subset of borrowers could access such products, or where the comparison basis is unclear. If the ad omits critical contextual qualifiers - such as owner-occupier status, loan-to-value ratio requirements, green loan restrictions, introductory periods, offset conditions, or refinancing assumptions - the overall impression may become misleading because consumers are encouraged to benchmark themselves against a rate environment that may not genuinely apply to their circumstances. Courts and regulators have repeatedly emphasised that advertisers cannot rely on technical qualifications buried elsewhere if the dominant headline message conveys a stronger or more favourable impression.

The wording “Rates from 5.XX%” introduces a different but equally important issue: indefiniteness and implied attainability. In financial advertising, the word “from” carries an implied representation that the stated rate is genuinely available, attainable, and representative of at least some meaningful portion of customers. However, if the “6.XX%” figure is intentionally vague, undefined, or used merely as a placeholder to psychologically anchor consumers to the perception of low rates, regulators may question whether the advertisement is communicating sufficiently clear and accurate pricing information at all. The use of “XX” in particular can become problematic because it suggests precision without actually providing it. Consumers interpret mortgage rates numerically and comparatively; replacing part of the figure with an undefined placeholder can create an impression of certainty or competitiveness while avoiding commitment to an actual rate.

Numerical rate-anchored ambiguity is especially dangerous because interest rates are heavily regulated representations. For consumer credit products, comparison rate obligations under the National Consumer Credit Protection framework require that advertised rates be presented with corresponding comparison rates in prescribed circumstances, and that disclosures be sufficiently prominent to avoid distorting the consumer’s understanding of the true cost of credit. Regulators are particularly concerned with “headline rate” advertising that creates a misleadingly optimistic impression about likely borrowing costs while obscuring qualifications, fees, or realistic eligibility constraints. A vague “6.XX%” representation may therefore attract scrutiny not merely because it lacks specificity, but because it can function as a behavioural anchoring device designed to shape consumer expectations without delivering a concrete, verifiable offer.

There is also a broader psychological and behavioural concern underpinning these representations. Mortgage consumers interpret rates heuristically; they rarely perform detailed legal analysis of disclosures before forming impressions. A headline asking whether the consumer’s rate is “over 6%” immediately frames the consumer as potentially overpaying, while an undefined “from 6.XX%” implicitly positions the advertiser as capable of delivering materially better outcomes. Regulators assess these advertisements through the lens of ordinary consumer psychology, not hyper-technical legal parsing. If the net impression created is that lower rates are broadly accessible or realistically achievable when they are not, the advertisement may be considered misleading even if some technical pathway exists by which a small number of borrowers could theoretically obtain the advertised figure.

Ultimately, the legal problem with these forms of wording is not their simplicity but their capacity to create imprecise yet powerful financial impressions while avoiding concrete accountability. In a highly regulated sector such as mortgage finance, ambiguity itself can become misleading where it materially shapes consumer expectations about pricing, eligibility, or savings potential.

Landing Page Design and the UX

Australian Consumer and Financial legislation does not only prohibit explicit falsehoods. it also prohibits implied misrepresentations, misleading conduct by omission, deceptive overall impressions, and misleading interface design - this is extremely important in terms of funnel architecture, flow, information, and design. Silly things like progress bars, loading animations, "calculating savings..." screens, pseudo-assessment flows, "checking lender eligibility", and other common nonsense (as shown in our examples) will all imply substantive backend analysis is occurring. If it is mostly theatrical UX intended to increase completion rates, compliance risk increases significantly.

Again, any language used to imply qualification, eligibility, suitability is both grossly non-compliant when results are expected, and there's significant legal exposure because the consumer was induced to disclose sensitive financial data based on an implied benefit that never genuinely existed. The industry bozos will tell you that "we never explicitly said that results would be returned", but that erroneous and self=serving claim is made because they don't have the technical literacy to provide a compliant experience. As we've discussed, the impression made to the consumer is what matters most.

Courts and ASIC will examine the dominant message, net impression, behavioural takeaway, and implied meanings made by advert creatives, copy, and landing page text. A claim can and will be misleading even if every sentence throughout your experience is technically defensible, but the experience is not matched by the experience itself. Content exclusion is not a defence. Sending a suer to a calendar rather than a results page when the results are reasonably expected is the most common and egregious method of deception. It has to end.

Regulators are increasingly targeting "dark patterns" on websites and landing pages, such as deceptive progress indicators, false interactivity, fake calculations, disguised lead forms, misleading urgency, and forced disclosure sequence - all extremely common in modern day subscription funnels. A mortgage funnel can drift into dark-pattern territory if users believe they are using a tool but are actually entering a sales qualification process, and the calendar redirect is an atrocious breach of consumer trust if the purpose of the information collection wasn't disclosed. This conduct becomes especially problematic where financial vulnerability exists, consumers are under mortgage stress, refinancing urgency is implied, or savings claims are suggested.

To be clear, you don't have to intentional deceive a consumer or print or imply explicit lies - it only matters if this funnel is capable of misleading. This single ASIC truth essentially makes the industry a cesspit of deceptive brokers.

Correcting It Doesn't Fix It

In misleading advertising law, contravention generally crystallises at the moment the misleading representation is published or communicated to consumers. The fact that material is later amended, corrected, or removed does not retrospectively erase the original contravention. This principle appears repeatedly throughout Australian consumer law enforcement and is reflected in both court reasoning and regulator guidance: the legal question is whether consumers were exposed to misleading conduct at the time of publication. Once publication occurs, the contravention is capable of having been completed, even if the content is subsequently altered. Subsequent correction may mitigate penalties, demonstrate cooperation, or reduce ongoing harm, but it does not nullify the existence of the original breach.

This principle is critically important in digital financial marketing because many businesses mistakenly assume that quickly editing a headline, removing a claim, or changing a funnel after complaints arise extinguishes liability. It does not. If consumers were induced to engage with the experience while the misleading representation existed, regulators may still pursue enforcement action based on the period during which the conduct was live. In practice, screenshots, archived pages, ad records, analytics data, session recordings, and consumer testimony can all become evidence of the original representation, even where the interface no longer exists in its original form.

Ultimately, the legal direction of travel is clear: regulators are increasingly unwilling to treat deceptive financial marketing as a peripheral issue divorced from the regulated advice process itself. As digital acquisition systems become more sophisticated and behaviourally engineered, liability is expanding beyond traditional notions of “advertising copy” toward the full architecture of consumer manipulation. In that environment, both brokers and the agencies designing their acquisition ecosystems face growing exposure where lead generation is driven by false expectations, simulated analysis, or implied results that never genuinely materialise.

Who is Liable for Non-Compliance?

In Australian financial services law, liability for misleading or non-compliant marketing is rarely confined to a single actor. Where a marketing agency designs, recommends, deploys, or materially contributes to a misleading mortgage or finance funnel, both the broker and the agency can potentially face regulatory exposure, civil liability, and enforcement action. The critical legal principle is that Australian consumer and financial services legislation is drafted broadly enough to capture any “person” engaging in misleading conduct “in trade or commerce,” not merely the holder of an Australian Credit Licence or Australian Financial Services Licence. Under section 18 of the Australian Consumer Law and section 12DA of the ASIC Act 2001 (Cth), the focus is on participation in the conduct itself. As a result, liability can extend simultaneously to the party publishing the material, the party authoring or engineering the experience, and the party commercially benefiting from it.

In practice, however, brokers and licensees usually carry the greatest regulatory risk because they are the principal financial services provider and owe direct statutory and professional obligations to consumers. A broker cannot generally avoid responsibility by claiming that a third-party marketing agency “handled the advertising.” If the funnel promotes the broker’s services, collects leads for the broker, or forms part of the broker’s acquisition process, regulators will ordinarily treat the broker as responsible for ensuring the experience complies with the law. This is particularly true in mortgage broking, where Best Interests Duty obligations and broader conduct expectations reinforce the principle that consumer-facing representations must be honest, fair, and not misleading at every stage of engagement. From a regulatory perspective, outsourcing the creation of a deceptive experience does not outsource accountability for its consequences.

That said, marketing agencies are far from insulated. Agencies can themselves become direct respondents in litigation or enforcement proceedings where they materially participated in the creation, optimisation, or dissemination of misleading conduct. Australian courts have long recognised “involvement in contravention” principles, meaning a party that knowingly assists, procures, induces, or is knowingly concerned in misleading conduct may itself face liability. If an agency intentionally designs deceptive UX flows, writes misleading copy, scripts false “calculation” sequences, or advises clients to use manipulative lead-capture mechanics while understanding the representations being created, the agency may expose itself to claims of direct participation in contravening conduct. Increasingly, regulators are examining not only who published misleading financial advertising, but who engineered the behavioural architecture underpinning it.

This becomes especially important in the context of modern digital funnels, where the misleading element often arises not from a single express statement, but from the cumulative behavioural effect of interface sequencing, animation, microcopy, progress indicators, implied calculations, and gated “results.” In those cases, the agency may not merely be a passive supplier of creative services; it may be the architect of the conduct itself. If the deception is structurally embedded in the UX design, regulators may view the agency as having played an active role in the contravention rather than merely executing client instructions.

Testimonials and other Compliance Traps

This section deals with various funnel designs and attributes that are designed to compete with our obligation to be honest, ethical, and transparent. Remember, our foundational prohibition as defined in legislation is as follows: "A person must not, in trade or commerce, engage in conduct that is misleading or deceptive or is likely to mislead or deceive". Bottom line: if you can't run advertising ethically, you shouldn't run ads at all.

Honest Testimonials

This section applies primarily to lead generation websites where services are handed off to brokers and not provided directly, although the consequences of inaccurate testimonial representations by brokers are as equally unconscionable. Testimonials refers to user testimonials and the fake (slider popup) 'trust' plugin used by a growing number of brokers.

The use of fabricated testimonials in financial advertising represents one of the clearest examples of conduct capable of undermining consumer trust, distorting market behaviour, and contravening Australia's consumer protection framework. Testimonials occupy a unique position within advertising because they derive their persuasive force not from the advertiser itself, but from the perceived experience of an independent third party. Consumers generally interpret testimonials as evidence that a real individual has interacted with a product or service and achieved the stated outcome. Consequently, a fabricated testimonial is not merely an inaccurate statement; it is a false representation about the existence of an underlying customer experience. The deception operates at two levels simultaneously: first, by misrepresenting that a particular person provided the endorsement, and second, by implying that the claimed experience or outcome has been independently verified through actual consumer use.

Australian law treats this form of conduct with particular seriousness. Under the Australian Consumer Law, contained in Schedule 2 of the Competition and Consumer Act 2010 (Cth), section 18 prohibits conduct that is misleading or deceptive or likely to mislead or deceive, while section 29 prohibits false or misleading representations concerning goods or services. More specifically, section 29(1)(e) prohibits false or misleading representations that purport to be testimonials by persons relating to goods or services, and section 29(1)(f) prohibits representations that concern a testimonial by any person if the representation is false or misleading. These provisions reflect a legislative recognition that consumers place significant weight on peer experiences when making purchasing decisions. A fabricated testimonial is therefore not regarded as a minor advertising embellishment but as a direct interference with the consumer's ability to assess a service based on genuine market feedback.

The legal significance of testimonials is amplified in financial services because consumers are frequently making decisions involving substantial long-term financial commitments under conditions of information asymmetry. Mortgage products, refinancing arrangements, debt consolidation services, and other forms of consumer credit are inherently complex. Consumers often lack the expertise required to independently evaluate every aspect of a proposed financial solution and therefore rely heavily on social proof as a decision-making shortcut. Behavioural economics has consistently demonstrated that individuals place disproportionate trust in the experiences of perceived peers, particularly when faced with uncertainty. Testimonials function as heuristic devices that reduce perceived risk and increase confidence in the decision-making process. A fabricated testimonial exploits precisely this cognitive tendency by creating the illusion of independent validation where none exists.

Fake Endorsements and Unlicenced Likeness: Other articles can be referenced to the plethora of ads that use fake , unlicenced, and unapproved celebrity endorsements , likeness , or images . Don't do it.

The regulatory concern extends beyond entirely fictitious testimonials. Misleading conduct may also arise where genuine customer statements are selectively edited, materially altered, attributed to outcomes that did not occur, or presented in a manner that creates a misleading impression regarding typical consumer experiences. Australian courts and regulators have repeatedly emphasised that the assessment of misleading conduct focuses on the overall impression conveyed to an ordinary consumer. Consequently, even a testimonial based loosely on a real customer interaction may become problematic if the manner of presentation exaggerates the benefits achieved or implies a level of success that is not representative of the underlying facts. The legal question is not merely whether some element of the statement is technically true, but whether the testimonial as a whole communicates an accurate and balanced impression of the consumer experience.

In financial advertising, fabricated testimonials frequently intersect with other forms of misleading representation. A testimonial claiming that a consumer saved a particular amount, secured a dramatically lower interest rate, or achieved a specific financial outcome necessarily implies that such results were genuinely experienced by an identifiable customer. If the testimonial is fictitious, then both the existence of the customer and the existence of the claimed outcome may be false. The testimonial therefore functions as a multiplier of deception, reinforcing other advertising claims through the apparent authority of personal experience. Regulators are particularly concerned by this phenomenon because consumers often perceive testimonials as more trustworthy than statements made directly by the advertiser itself. The fabricated testimonial effectively disguises advertising as independent evidence.

At a broader level, the prohibition on fake testimonials reflects a foundational principle of consumer protection law: markets function most efficiently when consumers are able to make decisions based upon accurate information. Testimonials are intended to serve as informational signals reflecting genuine consumer experiences. When those signals are falsified, the informational integrity of the market is compromised. Consumers are deprived of the ability to distinguish between businesses that have genuinely earned positive customer sentiment and those that have merely manufactured the appearance of public approval. In this sense, the use of fabricated testimonials is not simply a misrepresentation directed at individual consumers; it is conduct that undermines the reliability of one of the most influential forms of commercial communication. The legislative framework prohibiting fake testimonials therefore serves both an individual consumer protection function and a broader market integrity function, ensuring that trust, reputation, and consumer confidence are earned through genuine performance rather than manufactured endorsement.

A rehearsed, scripted, or role-play discussion or podcast that introduces a casual conversational testimonial or claim is equally offensive that results in the same enforcement action as a written testimonial. That scripted "you saved my friend John $2000 a month" (fake) 'phone call' while you sit there running numbers is a lie, so don't do it.

Presenting as a News Endorsement

Implying that the advert is in some way supported by news services is common, as is the representation of an advert in a news format . RG 234 warns against advertisements that resemble something they are not . If a financial advertisement is presented in a way that causes consumers to believe they are viewing independent editorial content, journalism, analysis, or objective reporting, there is a substantial risk that the overall impression is misleading. This principle stems from the underlying prohibitions in Section 12DA ASIC Act 2001, Section 12DB ASIC Act 2001, and Section 1041H Corporations Act 2001. ASIC's guidance consistently focuses on the dominant message conveyed by the advertisement, including headlines and visual presentation.

As Seen On: The "as seen in" news images with fake news logos violate principles discussed in the same way as testimonials. Further, they invite litigation from those news services when no endorsement was made. It's a method that is common to leadgen but increasingly making its way into DIY ads.

Fake Coundowns

Fake countdown timers in financial services advertising sit in a high-risk category of marketing practice because they are designed to manufacture urgency rather than reflect genuine time-limited conditions. In regulatory terms, the issue is not the visual device itself, but the behavioural effect it produces: pressure, reduced deliberation, and an implied scarcity that may not exist. At the core of the legal analysis in Australia is the prohibition on misleading or deceptive conduct under section 12DA of the ASIC Act 2001 and section 1041H of the Corporations Act 2001, along with prohibitions on false or misleading representations under section 12DB of the ASIC Act. These provisions operate on an “overall impression” test. That means regulators assess not only whether individual statements are technically accurate, but whether the dominant message conveyed to an ordinary consumer is misleading in context. The BS tactic communicates scarcity and urgency as factual conditions when they are, in substance, marketing constructs. Even where fine print clarifies availability, ASIC guidance in Regulatory Guide 234 (RG 234) makes clear that disclaimers cannot cure a dominant misleading impression created by prominent or attention-grabbing elements such as timers, banners, or headline claims.

RG 234 is particularly concerned with advertising techniques that pressure consumers into rapid financial decision-making. Countdown timers are a textbook example of what regulators view as "urgency cues", or those methods or design features that shift attention away from product complexity, risk disclosure, or eligibility criteria and toward immediate action. In financial services - where decisions often involve long-term debt, investment risk, vulnerable customers, or contractual obligations - this distortion of decision timing is especially sensitive. It is an unfair and non-compliant unfair pressure tactic (providing further compliance issues when paired with fake rates, news formats, fake qualification, or general lead capture).

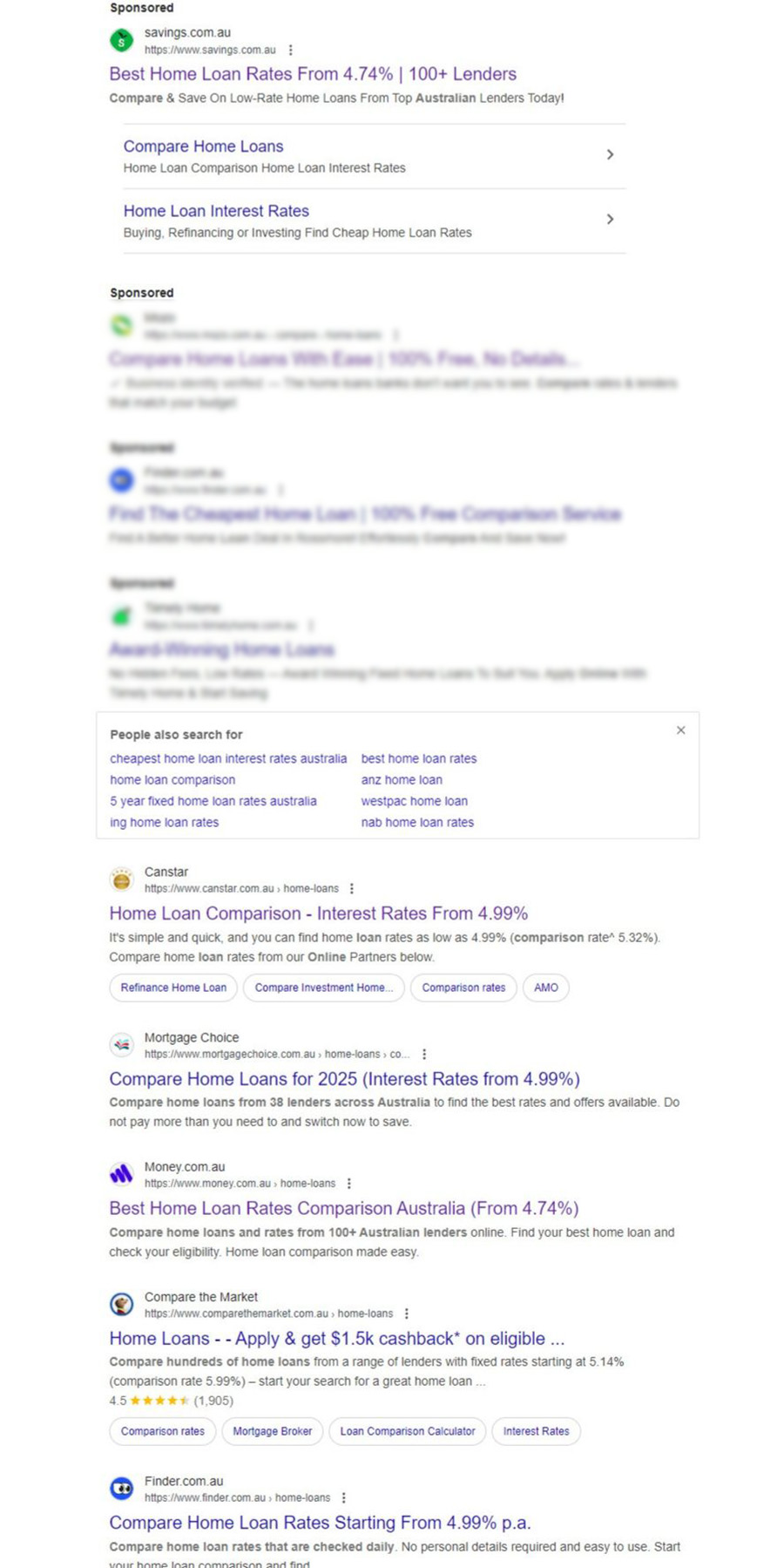

Representation in Search Results

Where a licensee publishes a nominal interest rate in any form likely to be indexed by a search engine, the accompanying comparison rate must be embedded with equal prominence in the same HTML source. Failure to do so is an actionable contravention of the NCCP Act s160 and is likely to breach general prohibitions against misleading conduct under the ASIC Act and ACL. Where a “green” or specialist rate is used to attract general borrowers, the omission of the qualifying context (including eligibility criteria) and the mandated comparison rate exacerbates legal risk and undermines DDO compliance. There is no effective legal defence based on the argument that “Google cuts off the snippet”. The relevant test is whether the representation as made is likely to mislead the average consumer.

Under the Design and Distribution Obligations (DDO) regime, we have a positive obligation to ensure that any financial product is appropriately targeted and not promoted in a way likely to mislead a retail consumer. Using a niche or specialist rate — such as an eco or “green” loan — as a headline grabber without context is legally fraught. A green loan - commonly used right now, and with the practice dating back a number of years - may be relevant for only a fraction of the population, and yet, presented without qualification, it can easily mislead the general audience into believing they qualify for that product when they almost certainly do not. This runs directly counter to both the spirit and letter of the DDO regime and the foundational principles of responsible lending or Best Interest Duty.

Pictured: In an era where 70 to 80% of borrower journeys begin with a digital search query, the obligation to ensure compliance extends to every word that might appear in a search engine results page (SERP) - whether paid (AdWords) or organic (SEO). Pictured is a search for various comparison websites. Those entities that returned rate in their Search title, only a few managed to satisfy the statutory obligation by disclosing a comparison rate alongside the nominal rate. The remaining websites in the same space either omitted the comparison rate altogether or buried it beyond the visible snippet - which, in functional terms, means it does not exist for compliance purposes.

To be clear: under ASIC’s regulatory framework, organic listings can be treated as advertisements. If a search snippet displays an interest rate, that snippet is effectively an extension of the ad or offer. While the probability of enforcement for an isolated organic snippet breach is low, the legal risk of "rate bait" is not zero - especially if there is evidence of systematic intent to highlight a low, unqualified special rate as a means of attracting clicks that the advertiser knows will not be suitable for the general market.

Misrepresentation of Interest Rates (Rate Bait) in Search Results: "Rate Bait" is introduced in an article titled "Misrepresentation of Interest Rates (Rate Bait) in Search Results". Sadly, the practice continues.

What Do We Do?: Given that we provide most of our clients a comparison engine, we'll often require the need to represent rates in search results (supported in a way that is suitable for broad Search and supplemented by the associated snipped). An article titled "How to Add an Interest and Comparison Rate to a Website Title" details how to use Rate Placeholders in a page title with other information supporting how we instruct Google to check the page daily.

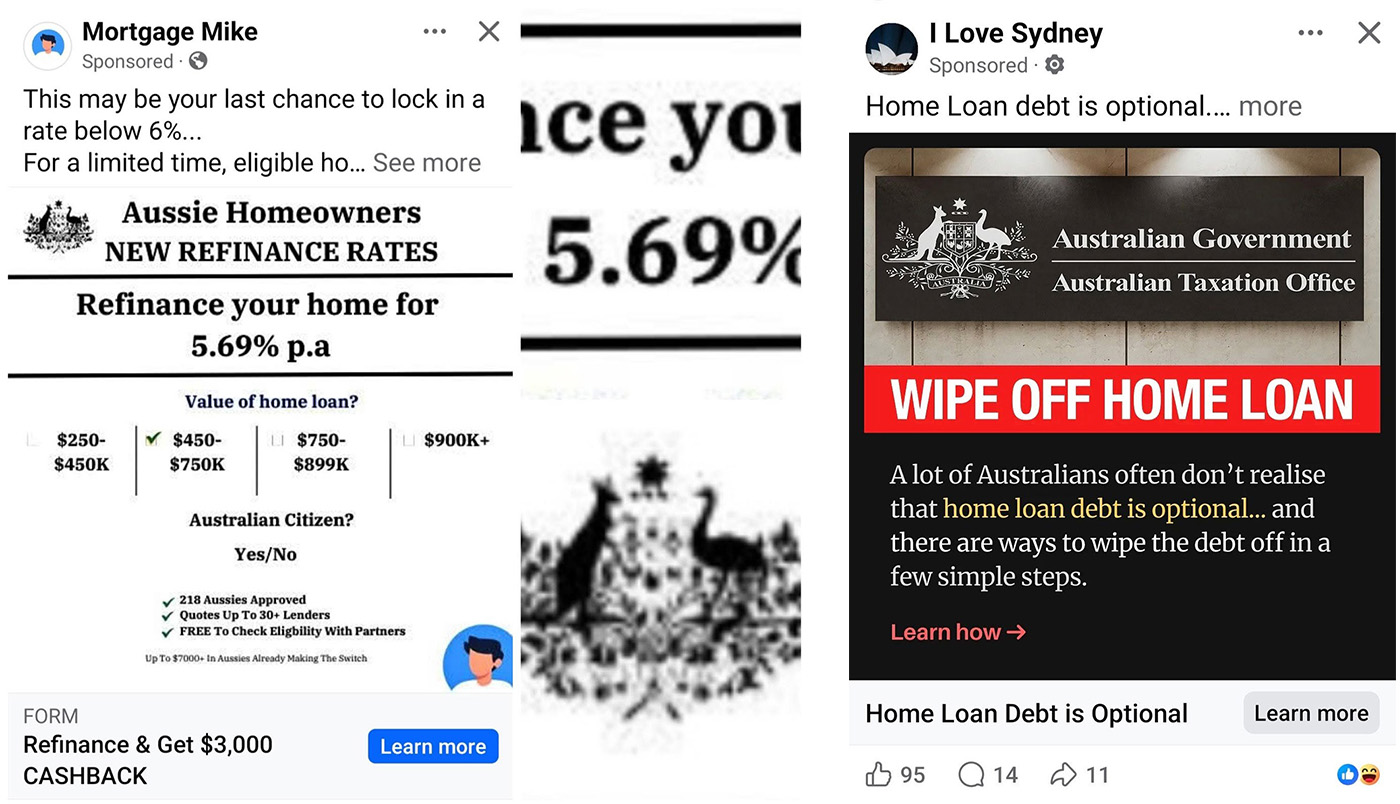

Trademark Law and Government Symbols

Not unlike the celebrity photos shown above (suggesting an affiliation or endorsement), certain symbols cannot be used in ads, such as the Commonwealth Coat of Arms (linked is one of about 30 examples). The use of the mark is regulated under federal law, and its use in any advertising is prohibited unless specific permission is granted (and it never is, particular when used in consumer-facing finance advertising, and certainly not on ad that is natively non-compliant or deceptive).

Let's look at some of the laws relating to usage of just the Coat of Arms . The Crimes Act 1914 (Cth)(Section 73) Prohibits the unauthorized use of the Australian Coat of Arms in a way that suggests a connection to the Australian Government. The Trade Marks Act 1995 (Cth)(Section 39) further states that the Australian Coat of Arms is a protected symbol and cannot be used in trade or commerce without authorisation. Use in advertising is considered a form of trade or commerce, and the Intellectual Property Laws Amendment Act 2015 (Cth) amendment strengthens protections for official government symbols, including the Australian Coat of Arms. The Copyright Act 1968 (Cth) states that The Australian Coat of Arms is not covered by copyright but is protected under laws governing national symbols with misuse leading to enforcement. Adding salt to the wound, the Australian Government Branding Guidelines clarifies appropriate uses of the Australian Coat of Arms and explicitly prohibit its use for commercial purposes, including advertising. Of course, there's basic Consumer Law that prohibits the implication that you have a government endorsement or affiliation, or that the representation is misleading (Schedule 2 of the Competition and Consumer Act 2010, Section 18).