We've created a large number of sliders recently that replace various legacy website features. The slider introduced in this article show selected post type content as sliding panels. The feature may be used anywhere with a drag and drop Elementor widget or shortcode, with the expectation that it will be used on the front page of your website.

The latest slider was designed for content sent to your website social and video archives - both blog-style archives of what is traditionally external content, such as social media posts and video. However, in the light of a little early feedback, we have updated the slider to include virtually all post types.

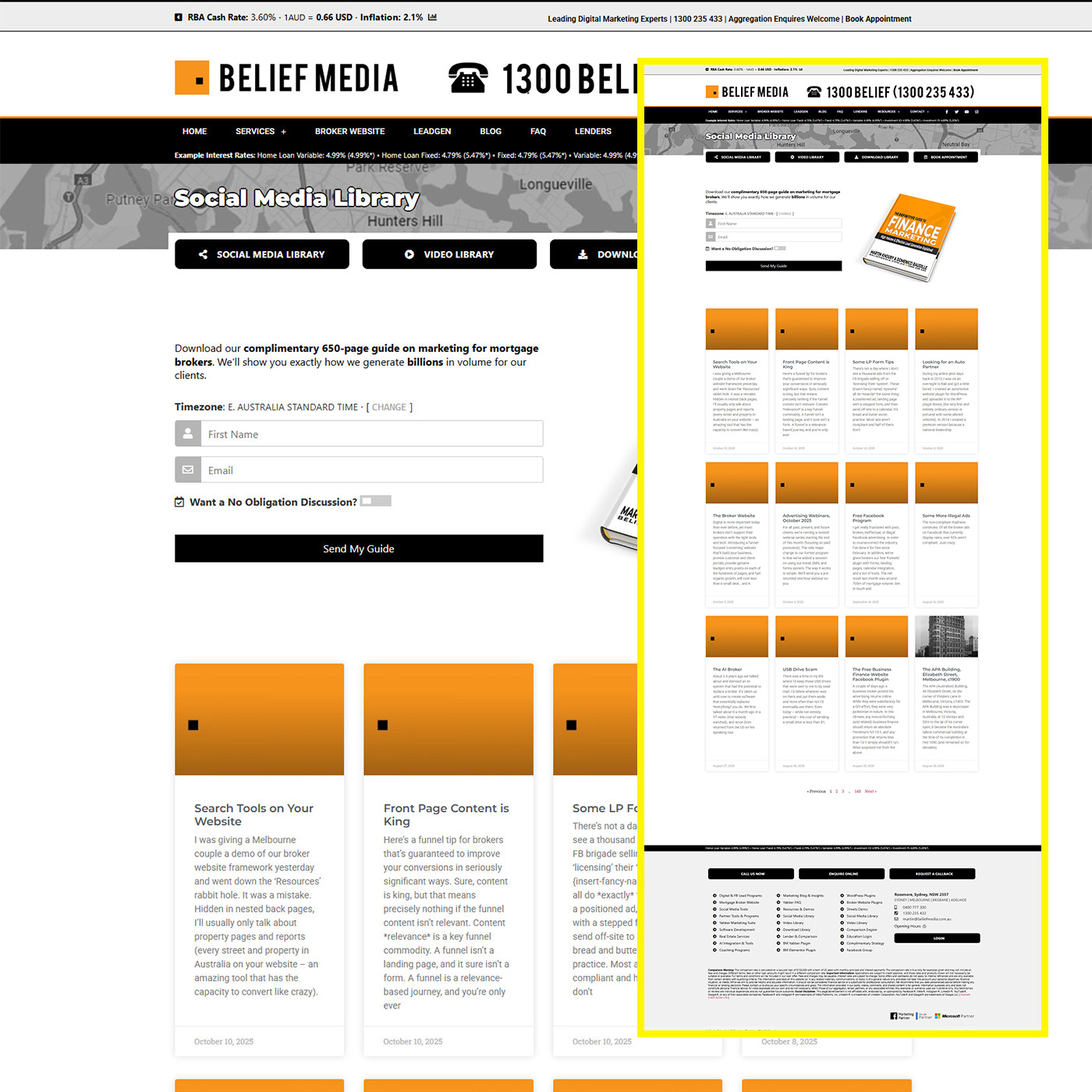

Social and Video Archive: The mortgage broker website we provide our clients includes links to the social, video, and various other archives in the website footer. The content fed to the social archives is part of the standard (and optional) distribution made available via the Instagratify and Vista social media modules (the former is an Instagram hashtag-based filtering tool while the latter is a method to post to social directly from a dedicated Outlook calendar) - both amazing tools. The video archive was formerly an automated tool but we've since updated the system so videos ingested by Yabber enjoy a little TLC before they're sent. Both of these archives are presented in a blog-style format with a styled page showcasing your content. They're both an excelling customer-focused and SEO tool that assigns ownership of the content you create back to you. If your website is the centre of your marketing universe (and it is), then your website should be an archive of your entire digital footprint - we shouldn't allow other networks to take ownership of our content.

The Result

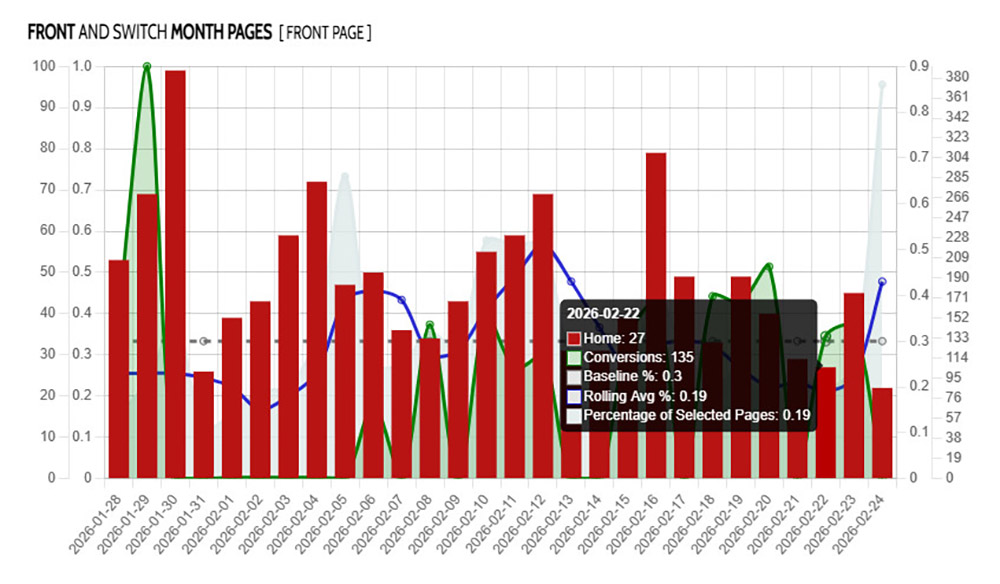

To return the default slider, we'll use the shortcode of [bm_posts_slider]. The slider isn't really intended to be used in an article, so we've used the shortcode attribute of truncate="16" to shorten the title, and this was done simply to ensure the title doesn't wrap around multiple lines.

Social Archive

Exactly 25 years ago I blasted off from Biggin Hill Airport in the UK flying a Bandeirante configured with 17 seats as part of the support team for the London to Sydney Air Race (2001). Flying to London (solo) as a youngling in my early 20s was fun, but bunny-hopping back to Sydney with a bunch of passionate people was an experience that's impossible to describe. It's on the race where I met the Campbell's team (flying an awesome Albatross), Kylie from Willow, and a bunch of other of our early billion-dollar business marketing clients. We'd sold AWE only weeks earlier for about 10k times what it was worth, and supporting these clients put us on a path that hasn't changed. Flying in a helicopter around the pyramids, flying a formation with the Albatross from Bali into Darwin, flying a tight formation with Ray Heiniger (recently retired Chief Pilot at Qantas) over Sydney Harbour, and a hundred other memorable moments in the air and on the ground, contributed towards an experience that really were the 'good old days'... but nobody told me that while they were happening. I founded iChoice only a few months after I returned. (The picture of…

Social Archive

Make no mistake: brokers are next. View on Instagram

Social Archive

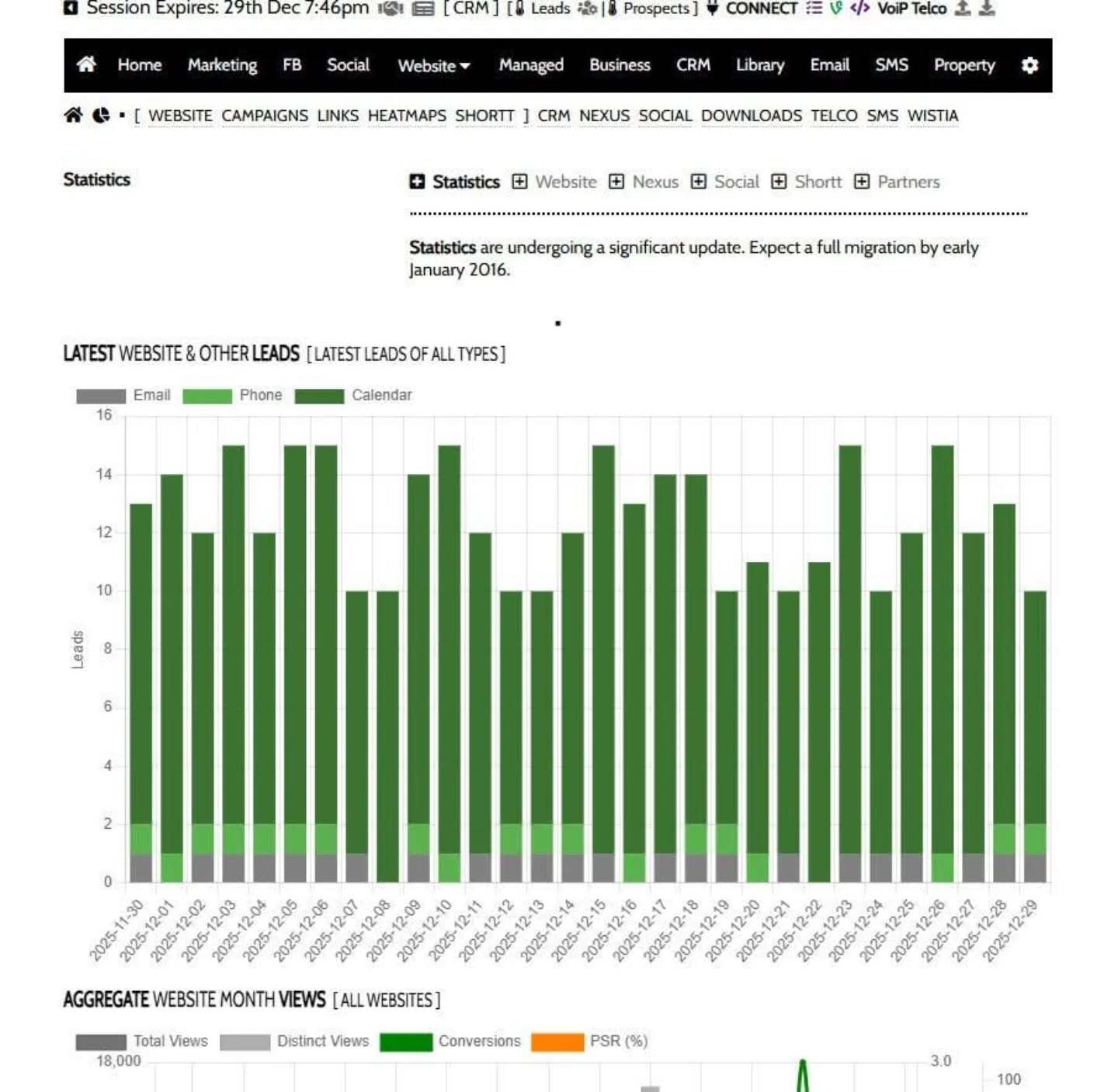

This is how a group returned 200m in monthly volume for less than 7k. 364 paid leads. Around 35% of their monthly lead expectation. Around $17 per SMS-verified lead. A little high, but verification will do that (it also reduces lead quality by about 20%). Leads typically cost less than $7, so this was an expensive gig. Around 243 converted clients based on results measured to the 14th December. Expected monthly return is over $200m. About 77% of leads visited the group website, and about the same number visited more than 5 pages. Half of that group visited the site again to review bookmarked or other pages. Digital done right gets results. You shouldn't expect to break a speed record in your Corolla, and you shouldn't expect good online results with a poor customer journey. We've still got website spots left for 80% off. Call me. 0400 777 300. View on Instagram

Social Archive

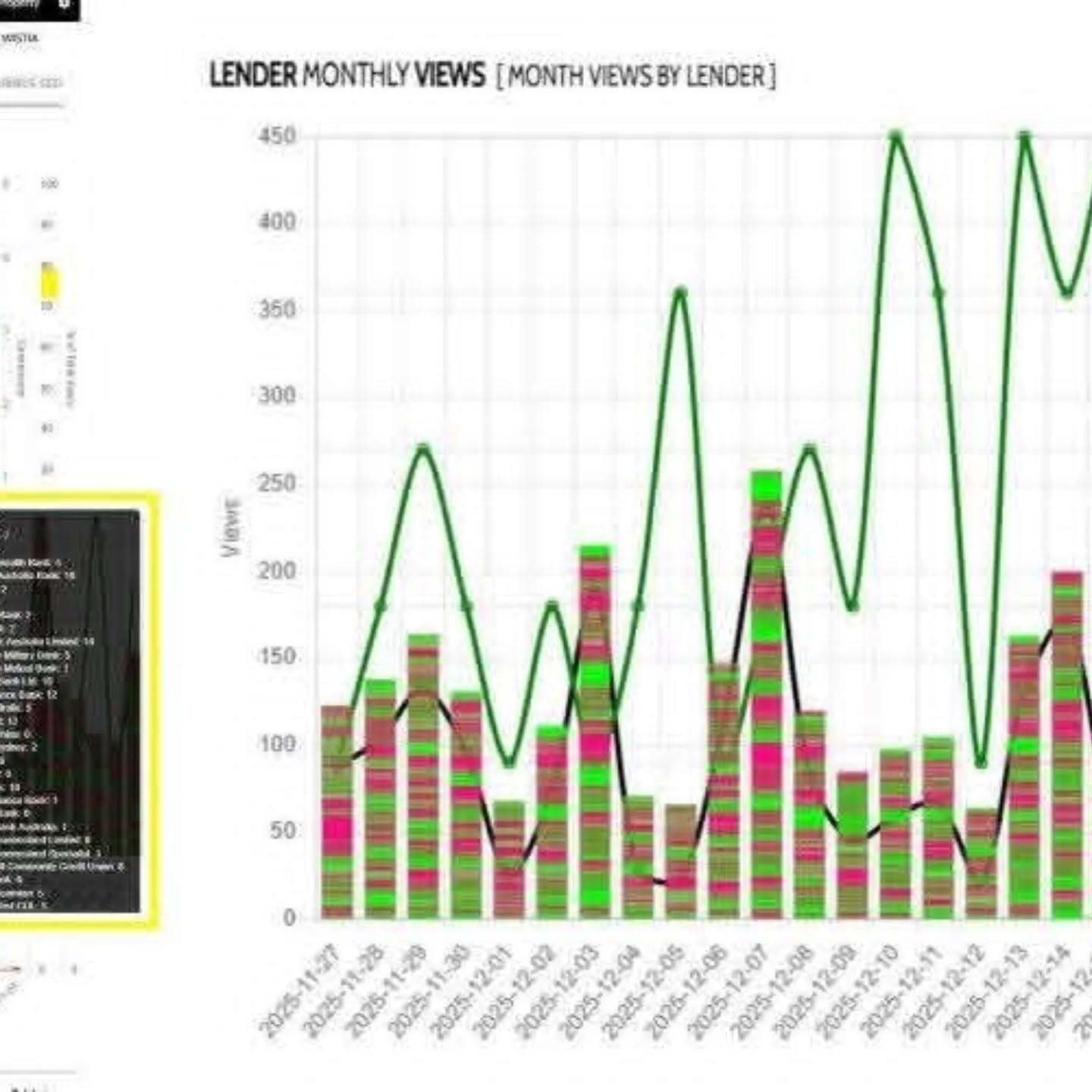

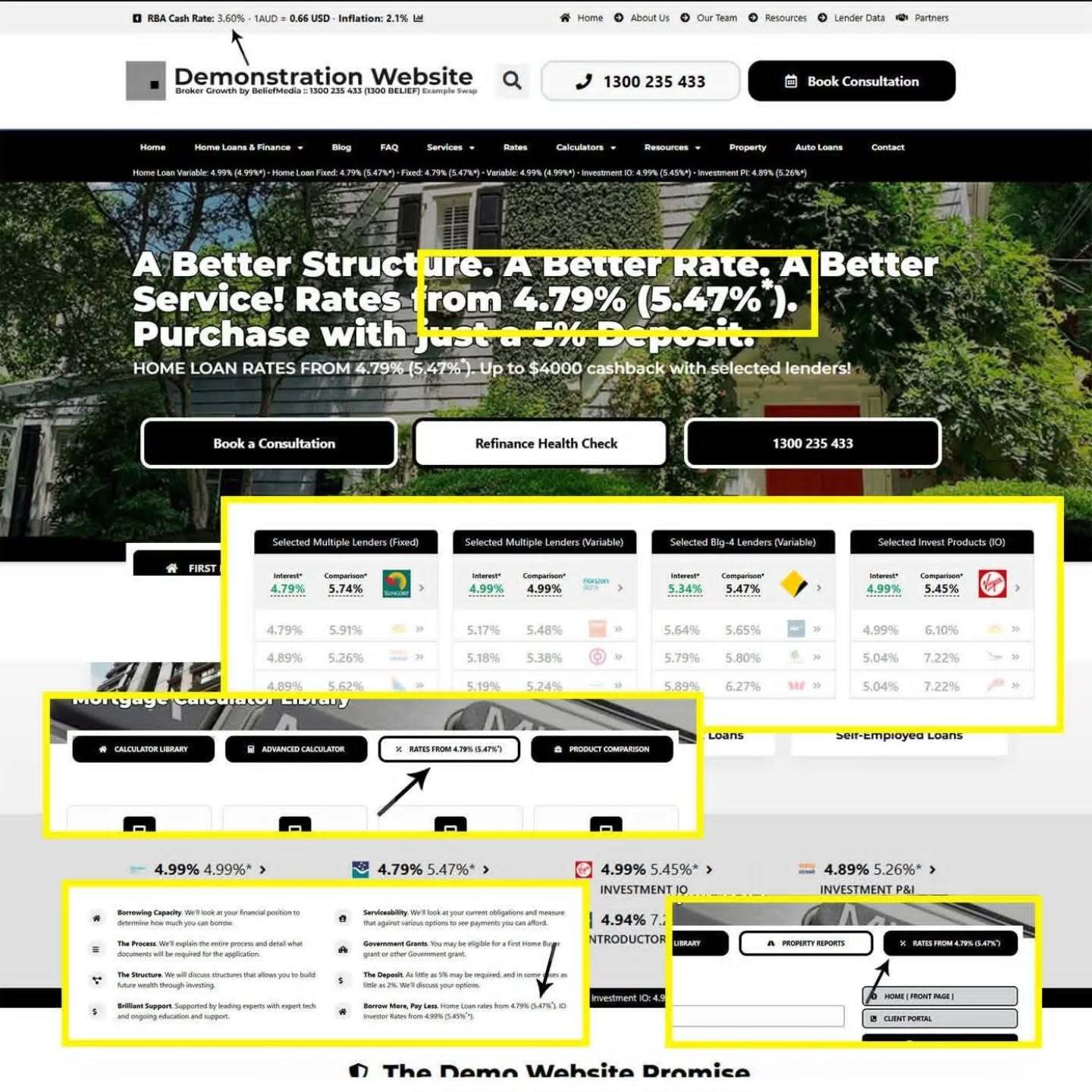

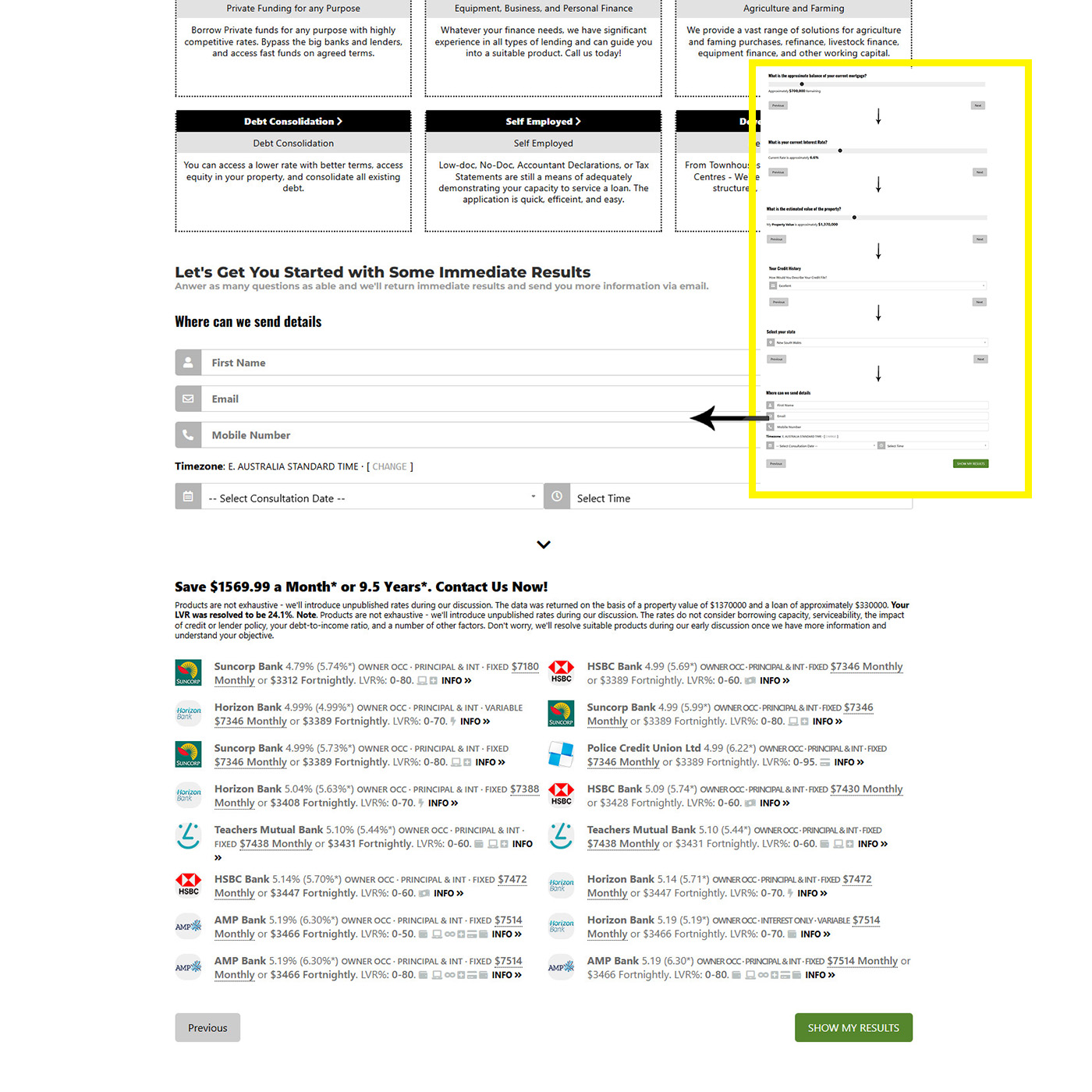

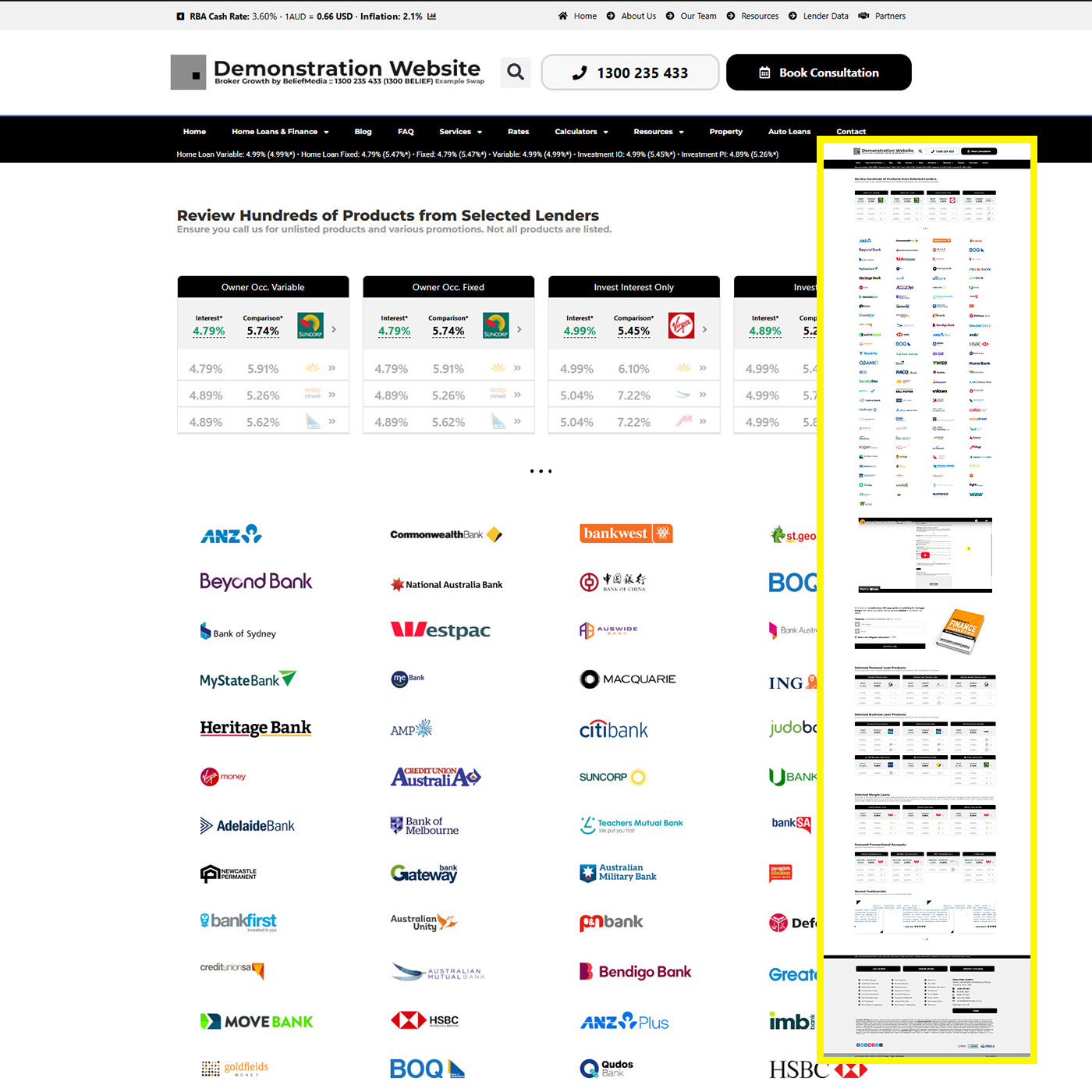

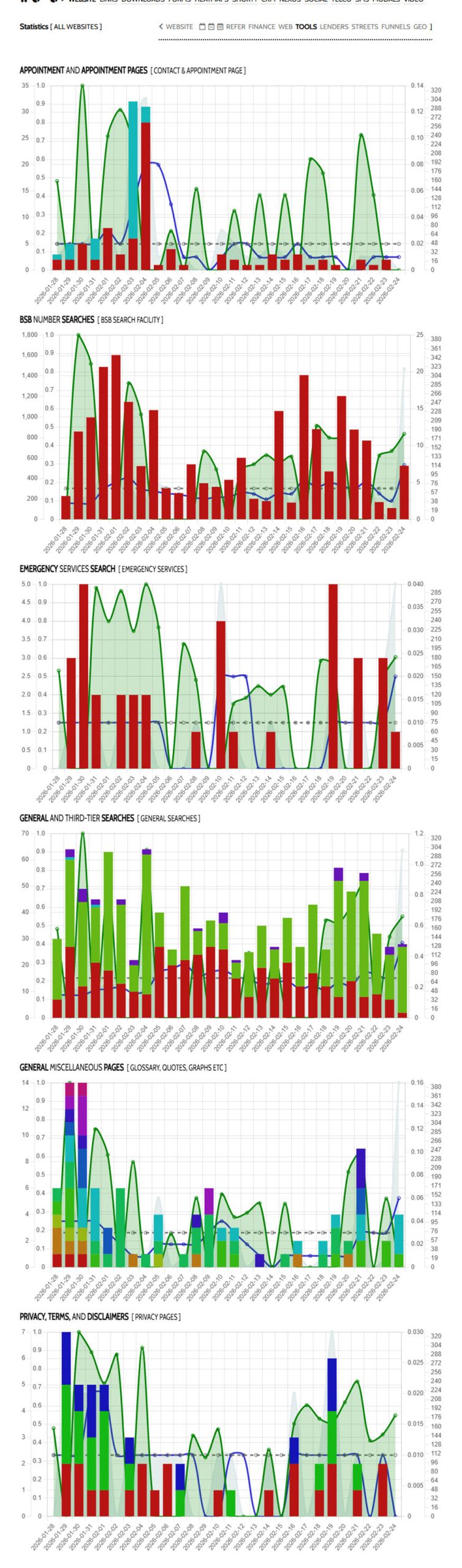

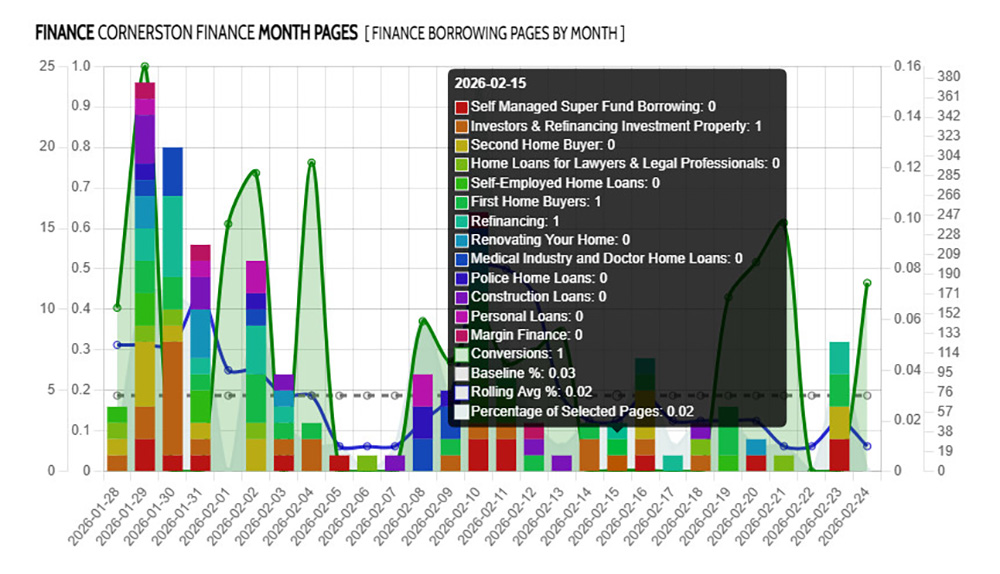

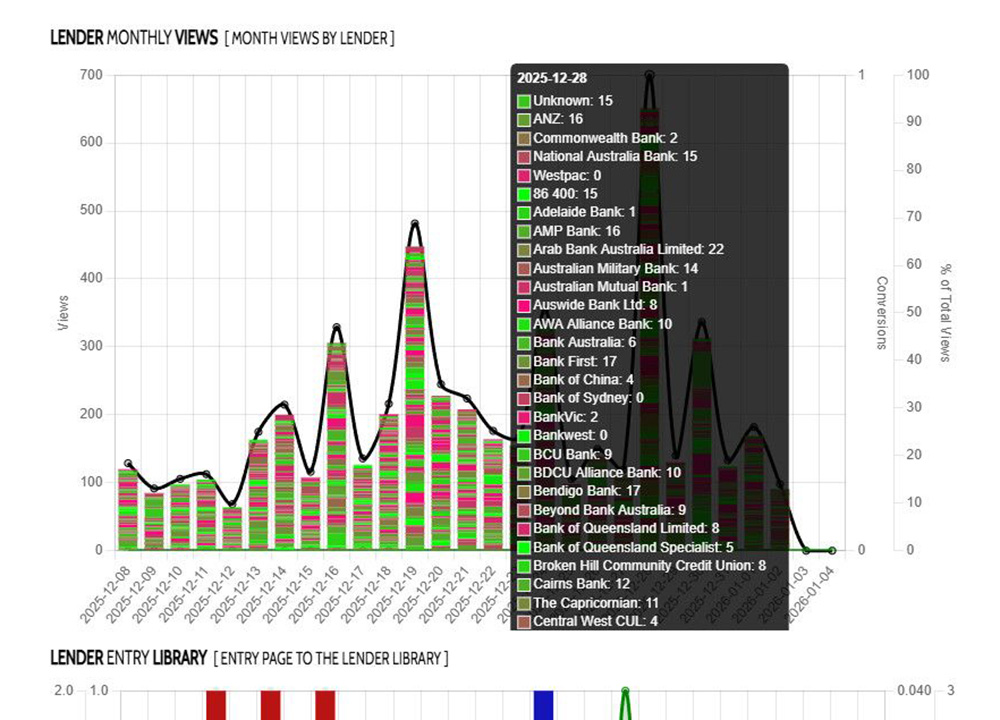

Rate data on your website is important. I've discussed it over and over, and I've talked about how those that are misinformed will erroneously associate information and education as a rate-driven broker culture. It's BS. From a performance point of view, I've attached some stats from a broker getting good results. The graph shows only lender product pages (stacked by lender). It also shows the lever views measured against all pages views, and conversion numbers (as line graphs). In this case, Mick's getting at least 200 views a day to lender product pages - and on some days over 400 - but the important part is that he's attracted at least a single calendar lead every day... and in this case he's attracted around 100 *quality* leads over the month. If you don't provide the information that is important to borrowers, others will. Not all our guys convert off these pages, and there's clear reasons for this. First, you need the right promotion on social, paid ads, promotion etc., and video (assigned in Yabber) explodes conversions. I see some with more page views and less conversions, and that's because the video or conversion facility isn't relevant. The gamified lender data…

Social Archive

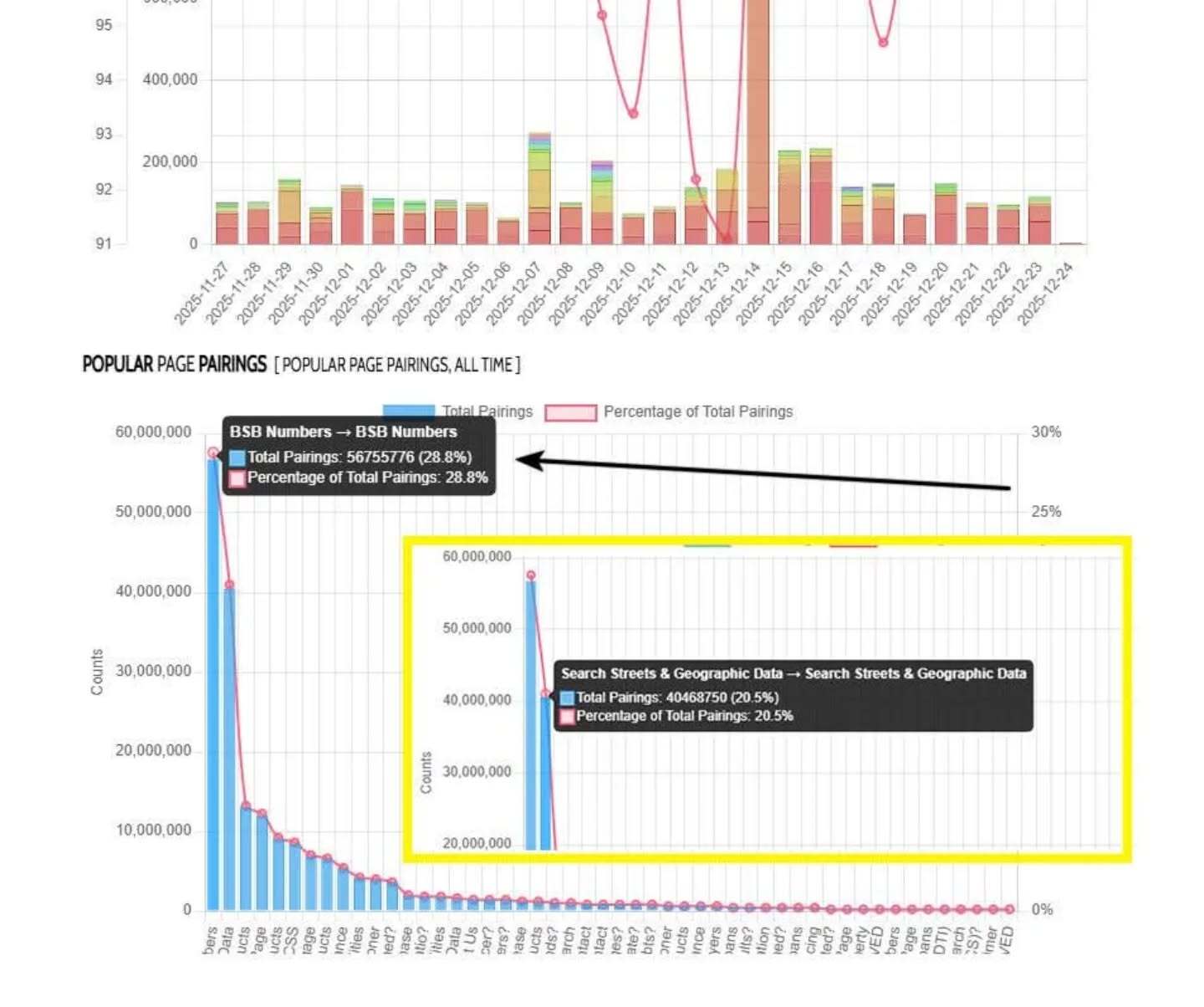

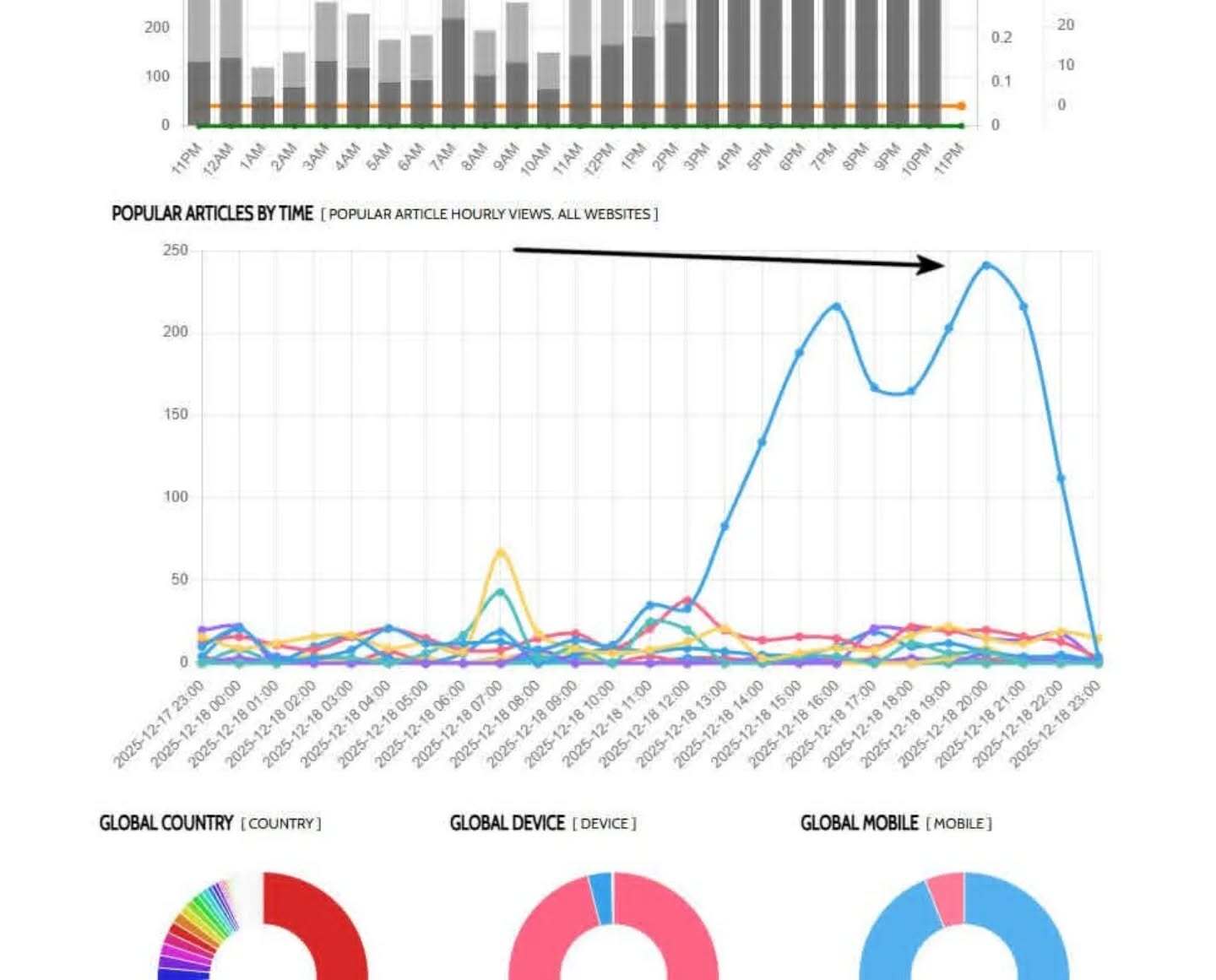

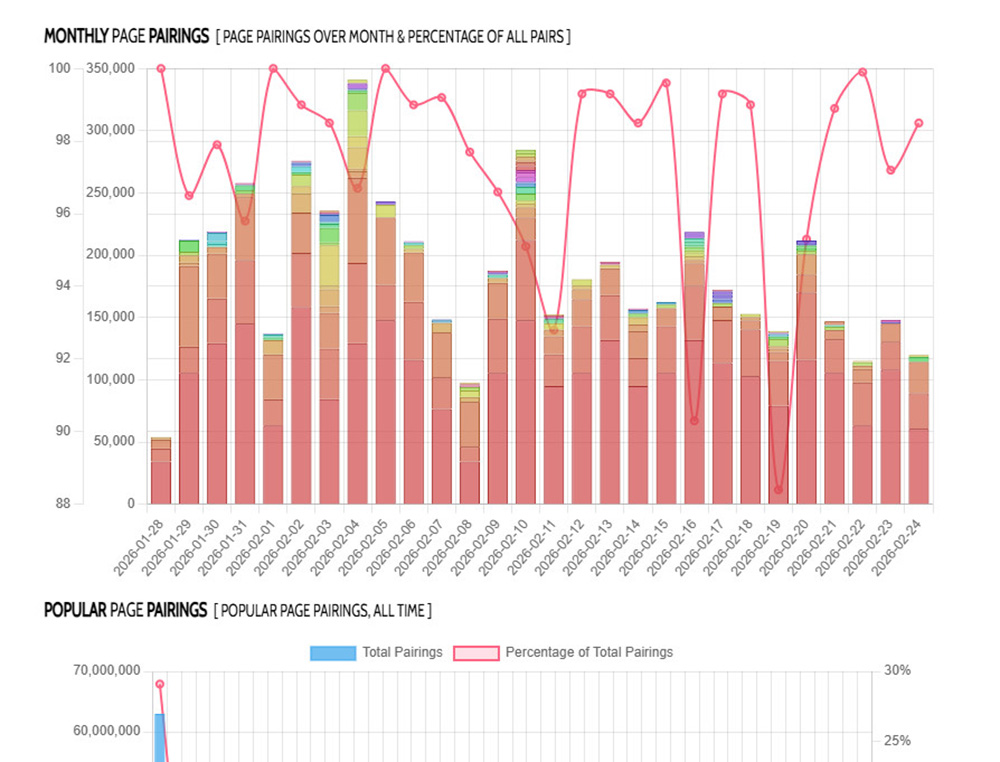

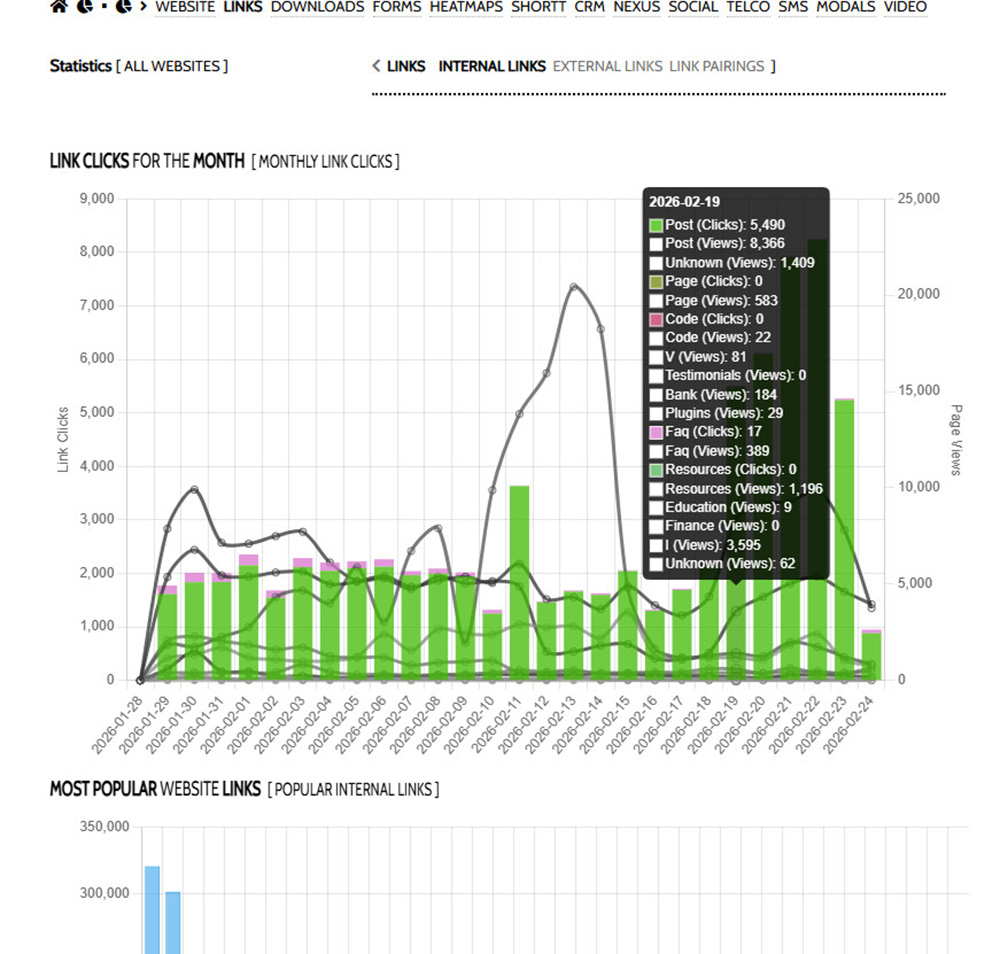

This statistic is very revealing. 100 million page pairings over a single year (from one of our own sites). It's why we built the same features into your website. Think of the conversion possibilities hiding in those numbers. Every page on your website is a type of landing page. Treat it as such and your life will change. View on Instagram

Social Archive

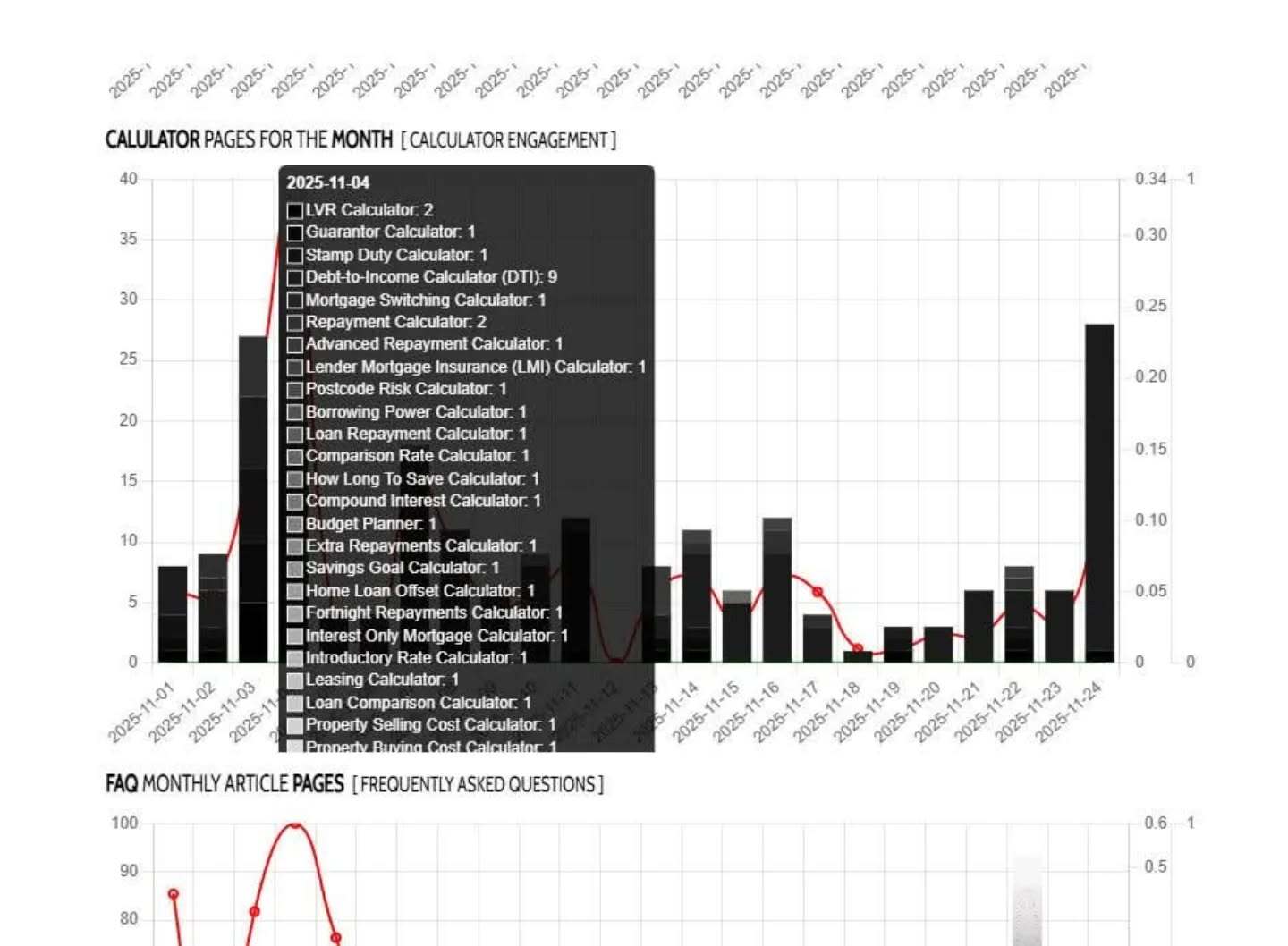

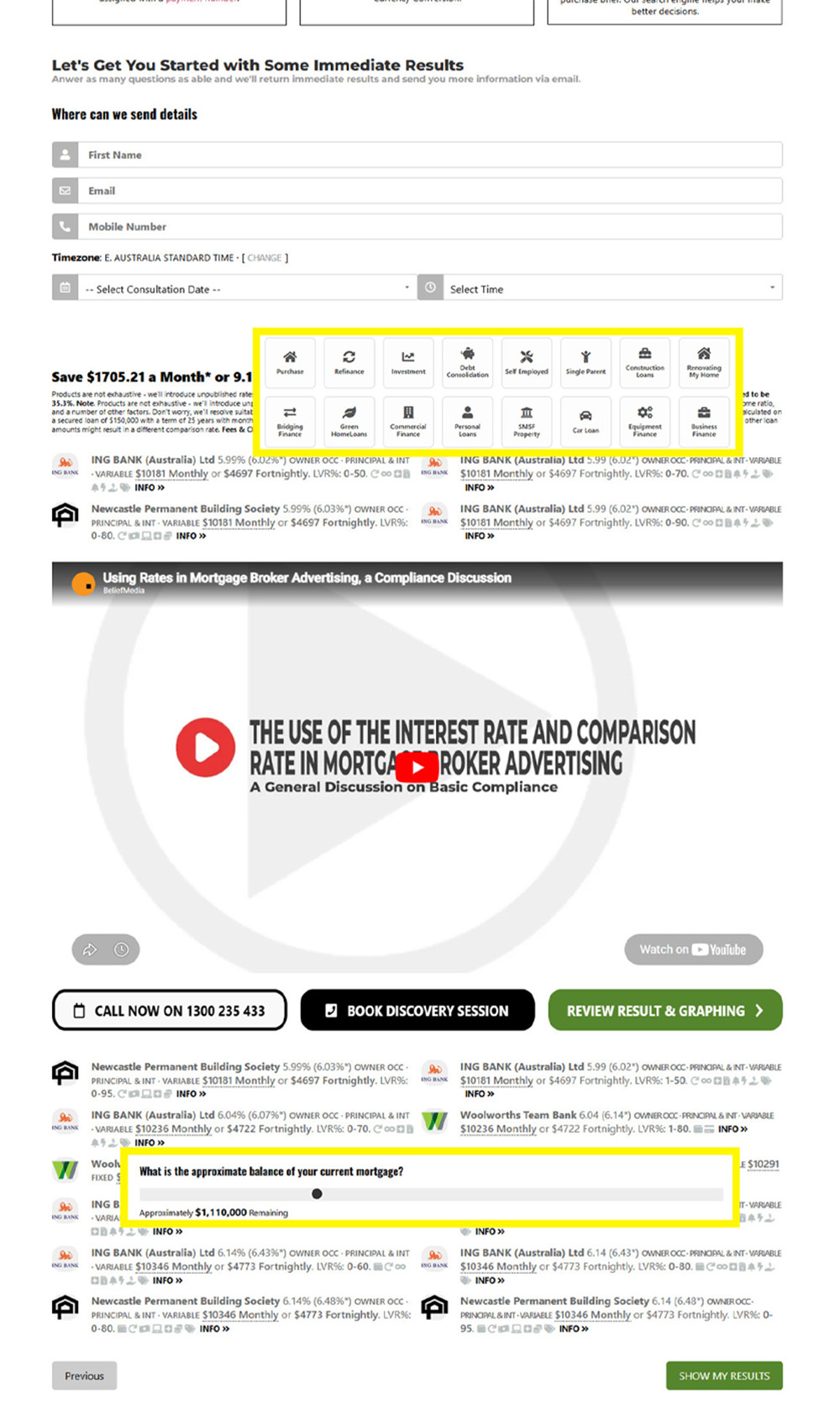

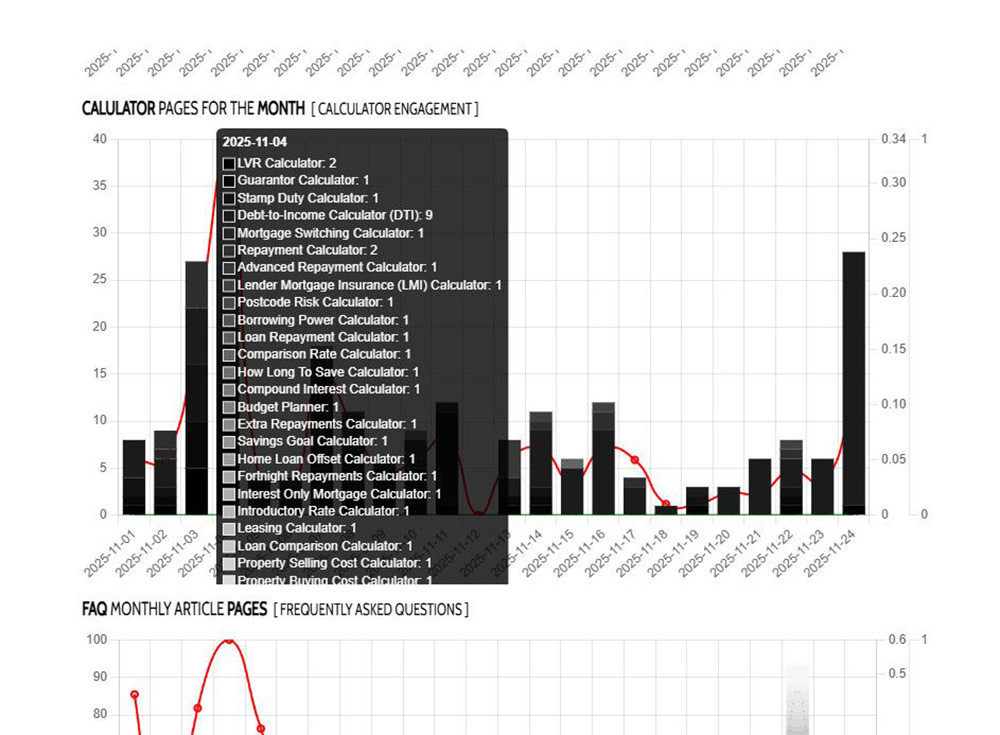

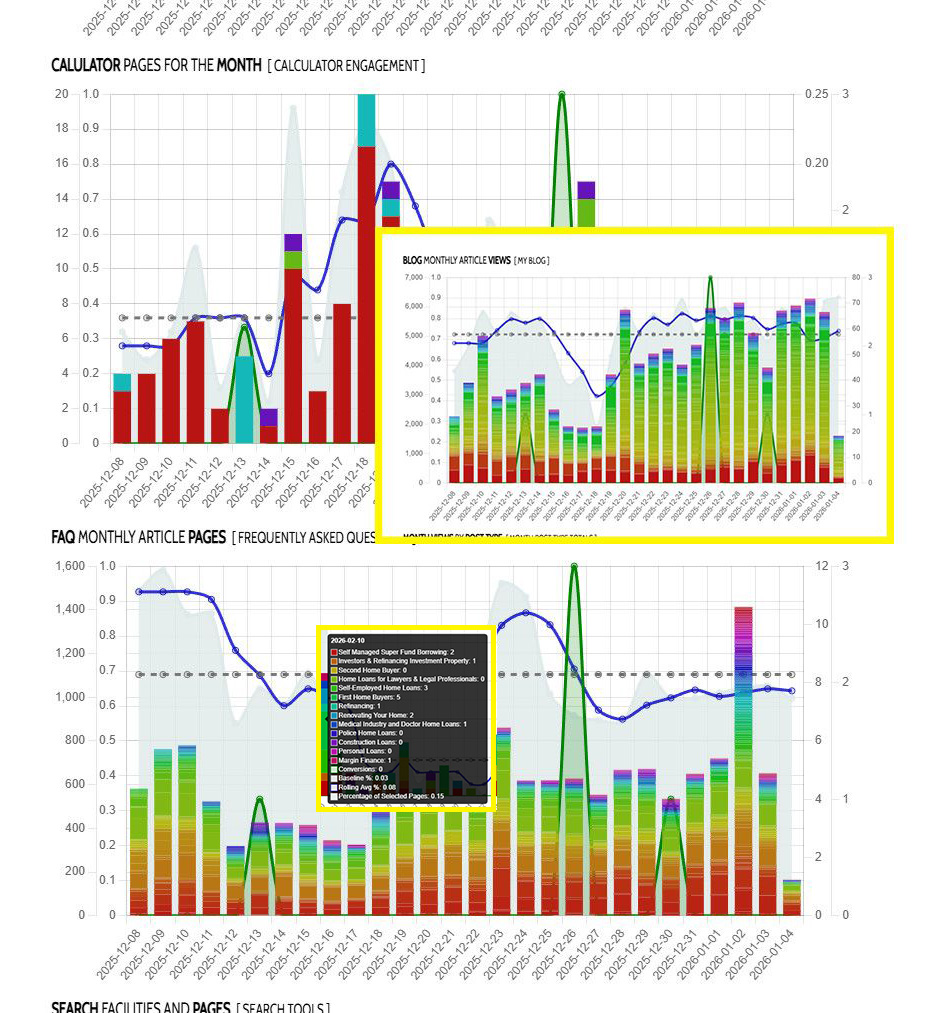

Stats from typical calculator views on a 'typical' site. You need to have calculators on your site to satisfy broad E+AT expectations, but they're only something you need to have, not something that'll actually be used. For a lot of brokers, 10-20 page views a day on just calculator pages might be a lot, but for our guys - while the pages should be design to convert (a whole other discussion), and should have purpose - they represent around 0.05% of all daily visits. It's staggering how much of an improvement can be introduced to your operation by way of out website for such a ridiculously small outlay. Call me. 0400 777 300. View on Instagram

Social Archive

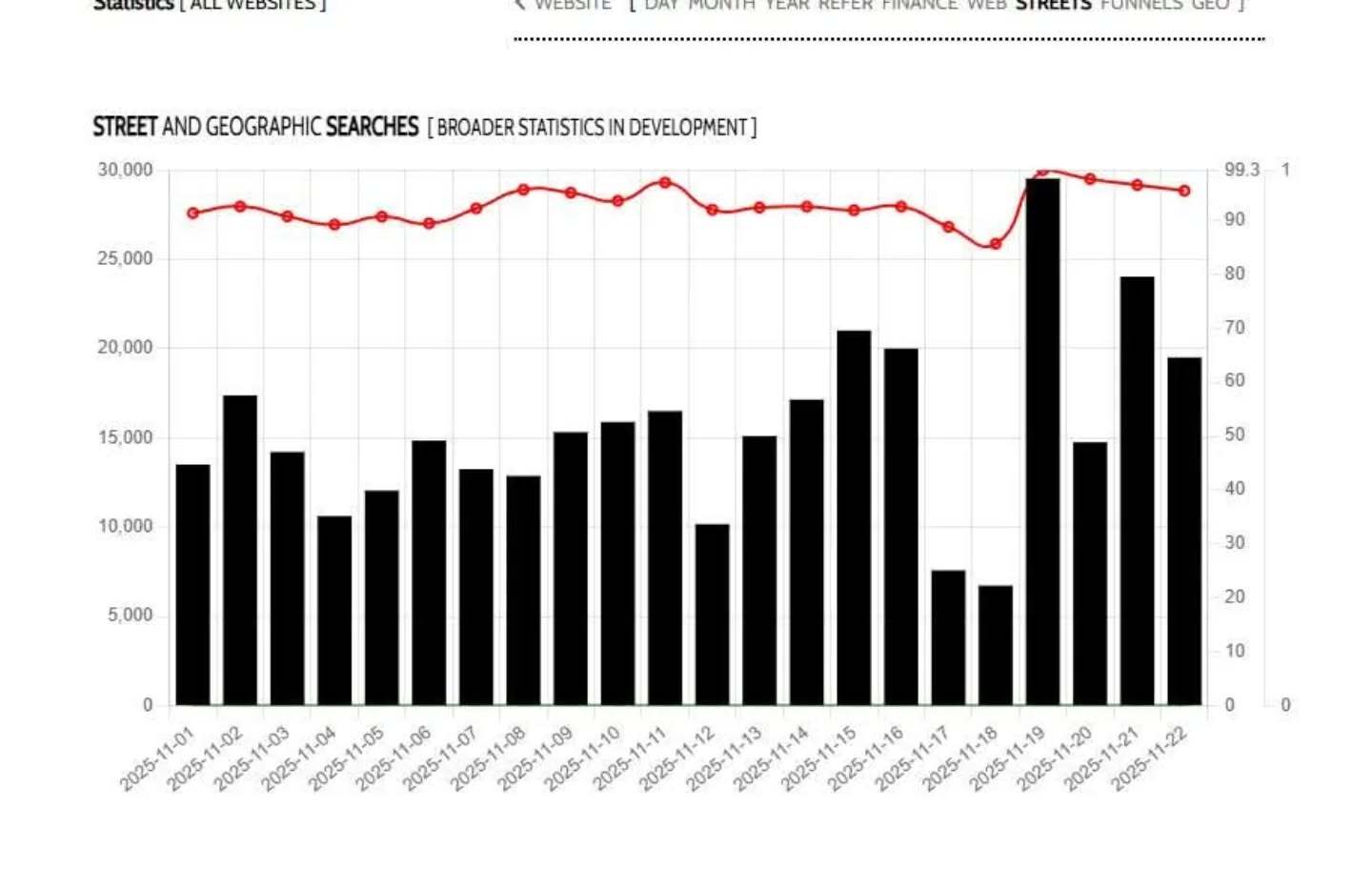

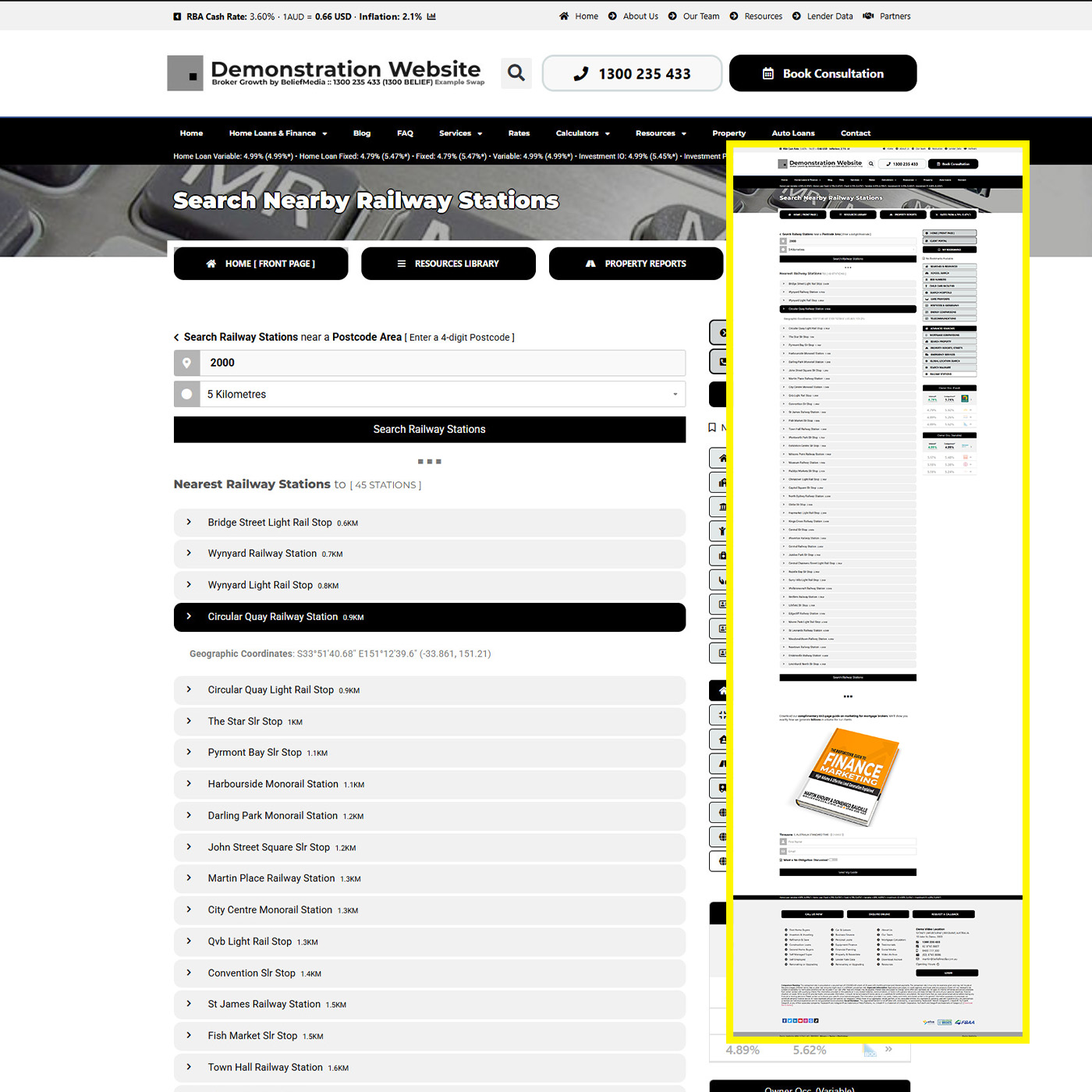

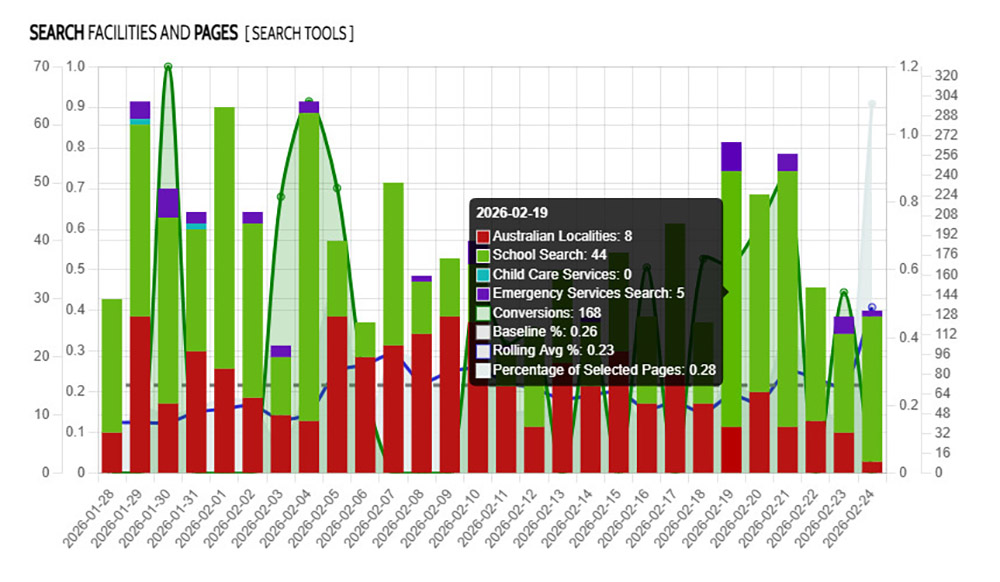

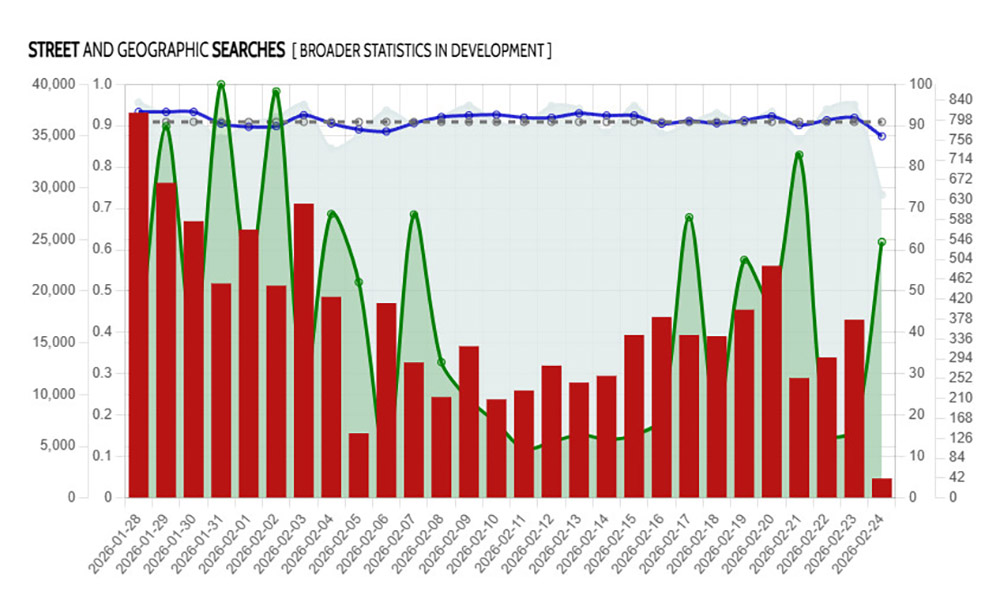

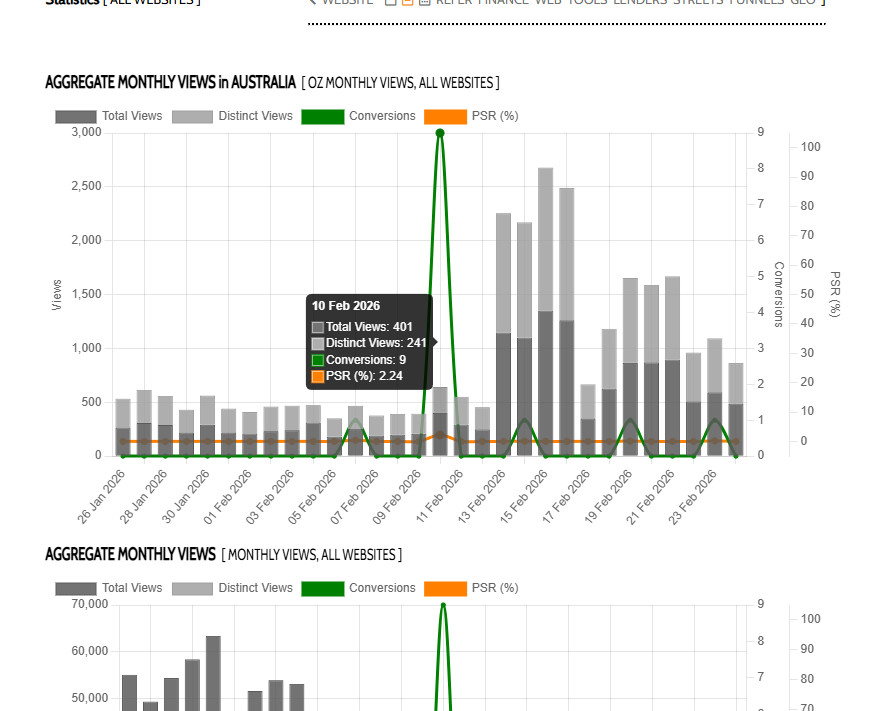

What would you pay to have an extra 25'000 visitors to your website every day? Is you were throwing money at Facebook, you would expect to pay around 300k. The broker associated with the pictured graph is attracting an average of 15k child visits to his website *every day* on the back of *just* the Geographic and Streets module. He plays this traffic well with high-intent offers via targeted forms and videos, and he attracts triple-digit leads every month. It's made him one of the highest-volume brokers in the country. SEO is made up of a number of parts. The first is the Object Graph and Markup (how your page is presented to Search/Crawlers), and the second is User Engagement Optimisation. It's the latter that is supported by this feature. It doesn't matter how you start a conversation... but it does matter how it ends. Before I continue, I should remind you that every page on your website is a type of landing page. Traffic comes from anywhere for any reason (in this case, your Geo modules), so we're compelled to provide appropriate conversion facilities on every page. If you're conversion doorway fails, you won't see any conversions... and I…

Social Archive

As I work through and update the vast array of advanced statistics in Yabber, I'm coming across some images I think are worth sharing. Pictured center are stats for a Sydney broker. He's averaging just 10 page views a day on his 'cornerstone' finance pages which isn't too bad given he's had his site for about a month (he previously averaged close to zero). However, he's averaging 17k views a day to his Streets module. 17k views a day! In fairness, the results aren't typical because he's promoted heavily through email campaigns and organic social, but the moderate effort has returned more leads in a month than he's seen in 3 years. You don't make friends with salad. Call me. 0400 777 300. View on Instagram

Social Archive

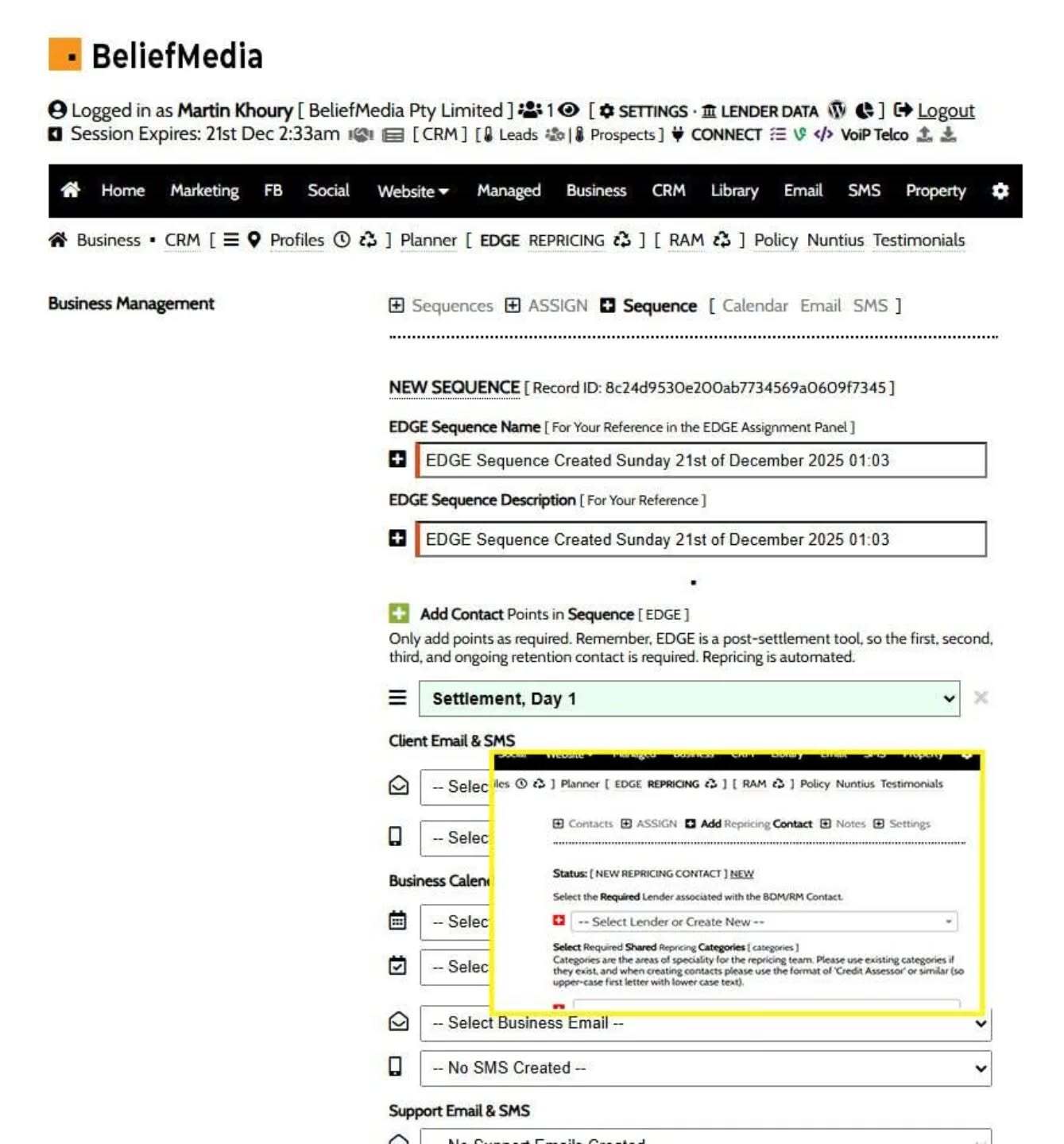

Our RAM module is worth taking about. Via `Shared Contacts' of lender BDMs, RMs, and others (that may optionally be synced to Outlook), you may send a single email to groups of support people that might be able to assist with a scenario or question. With the introduction of Nexus (email), all emails will now carry a reference ID in the title, and they'll be sent as an email campaign. This means that replies can be sent to your CRM, archived and aggregated, or used for other purposes. This module will be made available to (mostly) all in January. It is currently used by our managed groups to send several thousand emails a month. It's worth mentioning that emails are sent through your MS365 email account, optionally included in 'Sent Items', fully tracked, and completely compliant. Once you use it once you'll use it every day. It's no wonder our guys simply get better results. (Pictured image is before the update). View on Instagram

Social Archive

Our first version of Edge, a post-settlement and repricing system, was created around 2010. It has seen a number of changes over the years, and with the introduction of the new Nexus mail system, it'll be updated again. There's dozens of copycats now, and the industry finally caught up with the concepts, ideas, and methods that were the backbone of my own brokerage, and part of my course messaging when I was coaching. Our Edge system isn't currently available to all brokers, but it will be released to (mostly) everybody in early January after we've applied the email updates. I did a 2am Web demo this morning with a broker that was using High Level for this task. As an auditor, this terrifies me, and as a marketer, it makes me laugh. If High Level is part of your business stack, it's time to re-think you're life choices! From a functional perspective, It doesn't even create CRM notes. Just crazy. Don't use High Level for anything! By the way, I've even heard of a coach (that should know better) introducing High Level for this post settlement purpose. Apart from *massive* compliance issues, it doesn't and can't perform 10% of the…

Social Archive

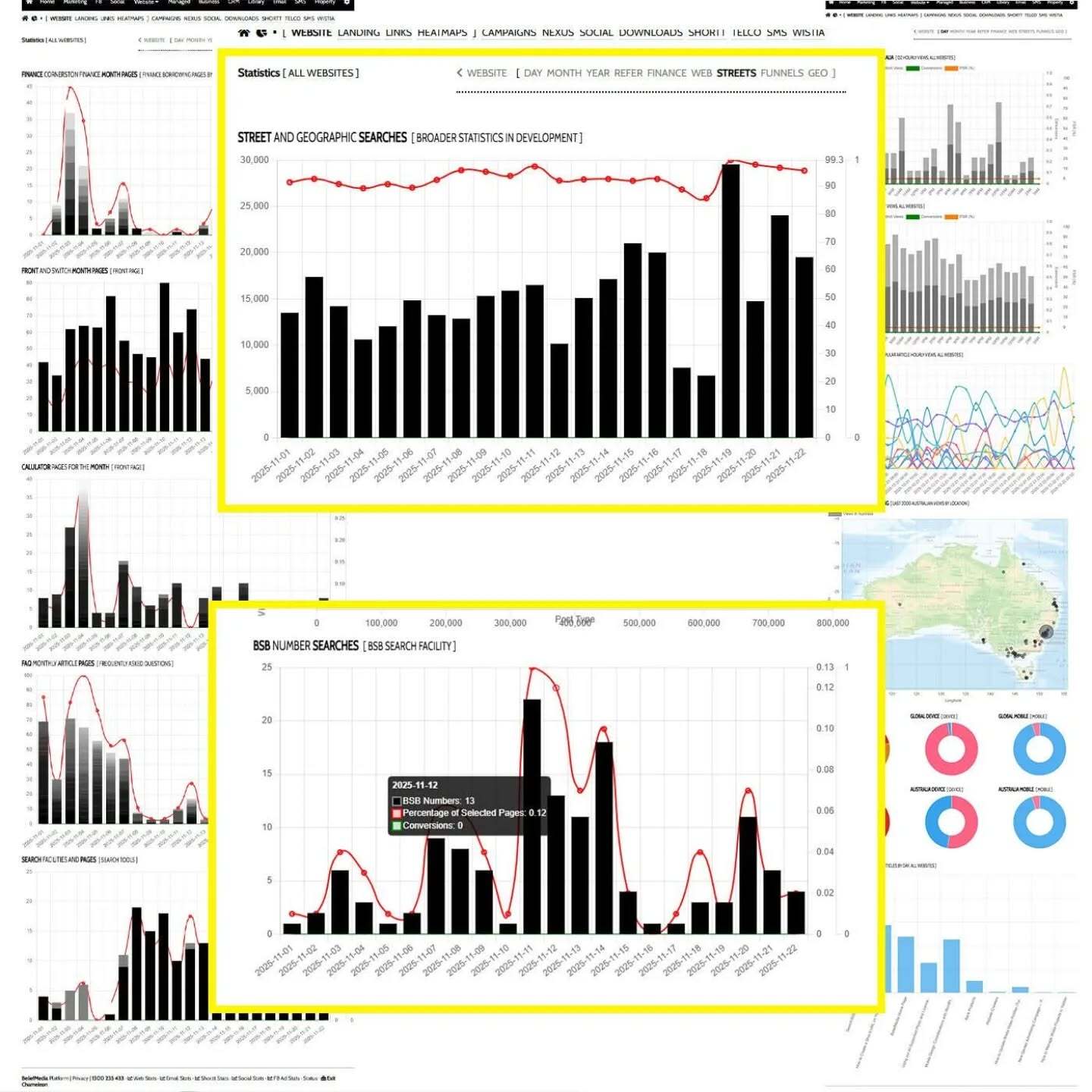

I shared a BSB website example the other day and talked briefly about why it existed, and how a conversion facility was necessary. The broker in question didn't have a sound conversion funnel in place, so I built one with her. The net result of up to 280 cold views each hour? Four new bookings in a single day, which is more than acceptable for completely cold traffic. Again, the traffic was completely cold, so they were directed to her site for reasons other than home loans. I genuinely hate seeing brokers throw a budget into bad leads before they've optimised their website. Most business owners have no idea of the traffic that bounces elsewhere because their experience was underwhelming. View on Instagram

Social Archive

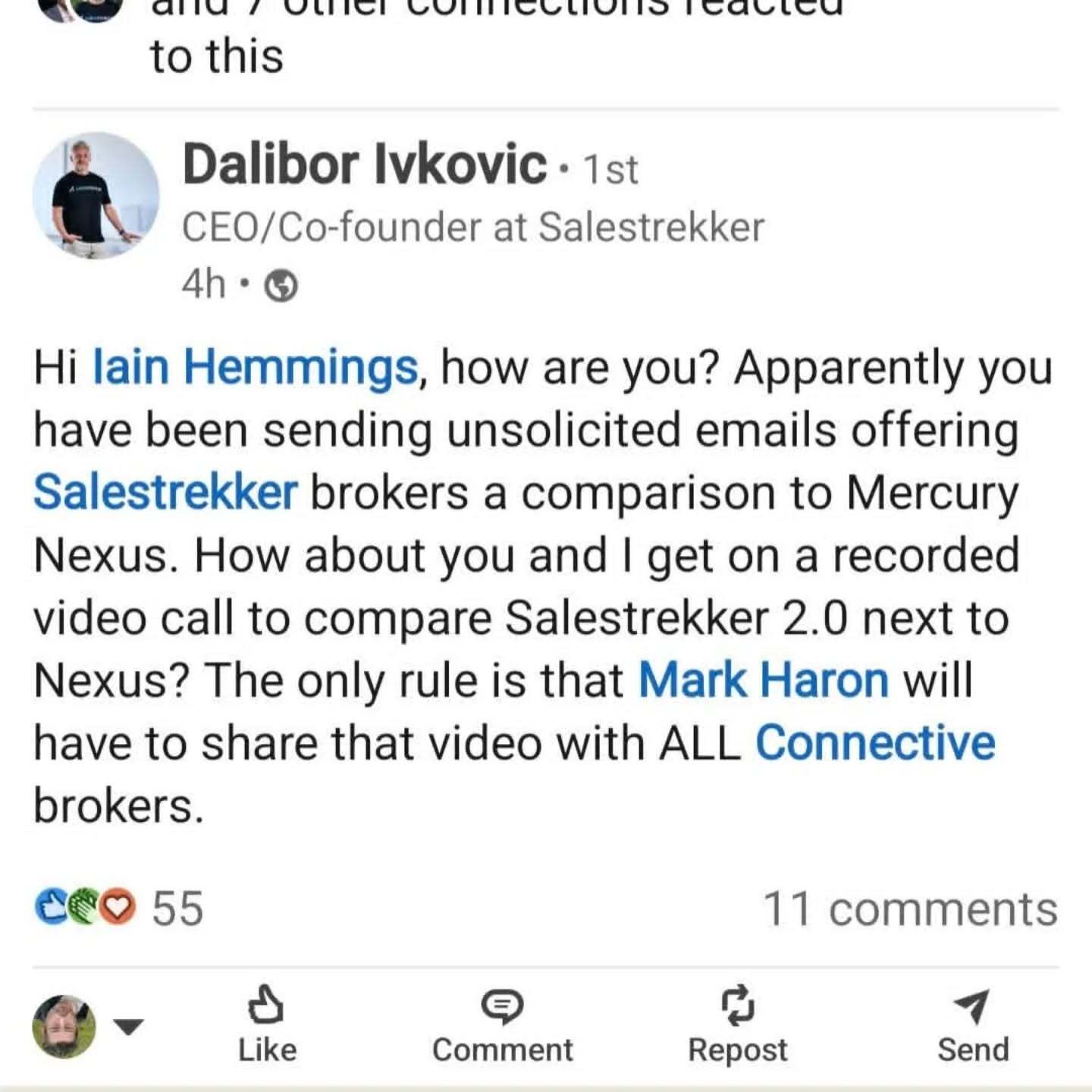

Salestrekker is a better CRM, but Mercury comes in at a close second. Certainly, if you're looking for API integration in order to automated your operation, Mercury is more reliable. Everything else comes in various shades of 'not as good'. I'd love to know how we could convert ST guys into (our) Nexus?!? The cost, perhaps? View on Instagram

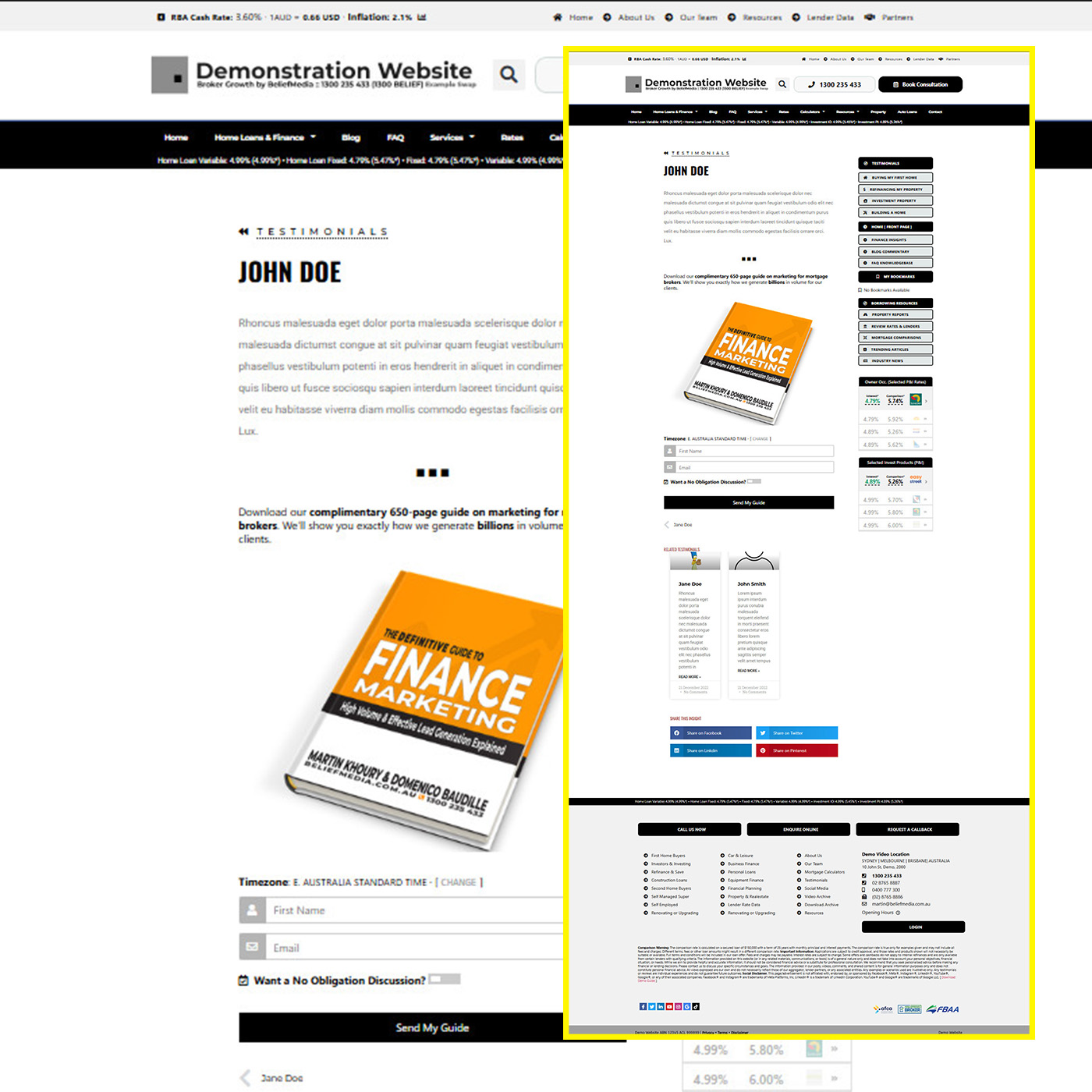

Slider Details: Showing a slider in this narrow post isn't ideal because much of the formatting is lost, and various spacing isn't preserved. It's likely we'll have an example on the front page of this website. As we'll introduce shortly, virtually every option in the slider may be customised (including the image shown as the 'featured' image). We looked at including the hashtags in various locations but ended up simply adding them to the end of the description. Note that only the most recent results will show the correct featured image and image icons until a Yabber database update is performed.

Pictured: Two slides showing post from the video archive. Note that we have 'play' icons that launch video modals. The featured image is inherited from the featured image defined as the video category in Yabber.

An option is made available in Elementor (and shortcode) that renders all post images as icons which will launch an image modal. This feature is enabled by default, and it is available for content other than the posts in the social archive.

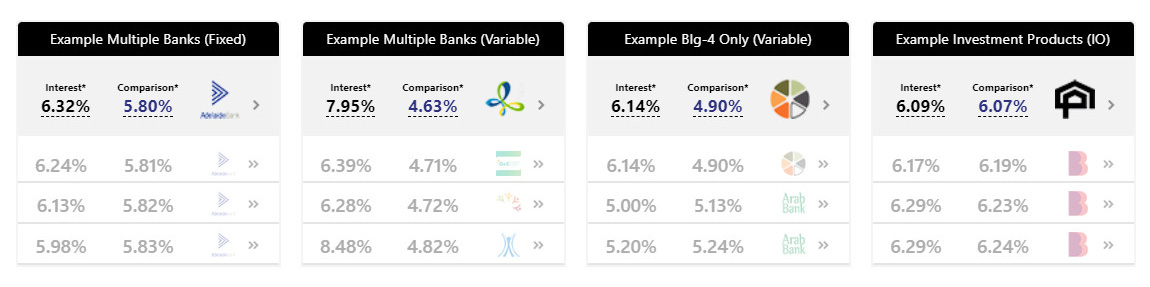

Before we introduce the simplicity of Elementor, consider the shortcode necessary to render the next slider. Shortcode of [bm_posts_slider post_type="post" meta_margin_top="-12" include_first_image_as_featured="1" slide_speed="6" number="14" items="1" truncate="50" apply_shadow="0"] returns the following:

Blog & News

How deregulation, securitisation, mortgage management, independent broking and distribution technology created one of the most consequential institutions in Australian finance. Finance aggregation is now part of the institutional infrastructure of Australian lending. It connects thousands of independently owned mortgage and finance broking businesses with banks, non-bank lenders, mortgage managers, insurers, technology providers and regulators. Aggregators administer lender panels, accredit brokers, transmit applications, calculate and distribute commissions, maintain compliance systems, collect market data, deliver professional development, provide licensing structures and, increasingly, manufacture or distribute white-label credit products. This mature institutional form conceals an irregular history. Aggregation was not invented on a particular date, nor can its emergence be attributed convincingly to one company. It developed through the convergence of several earlier markets and organisational forms. Traditional finance brokers already arranged commercial, equipment and private mortgage finance before the modern residential broker channel existed. Financial deregulation then weakened the institutional boundaries that had governed Australian banking. The recession of the early 1990s redirected bank balance sheets towards residential mortgages. Wide lending margins created room for specialist competitors. Securitisation allowed lenders without deposit bases or national branch networks to fund residential loans. Mortgage managers separated the funding, origination, administration and branding of a…

Blog & News

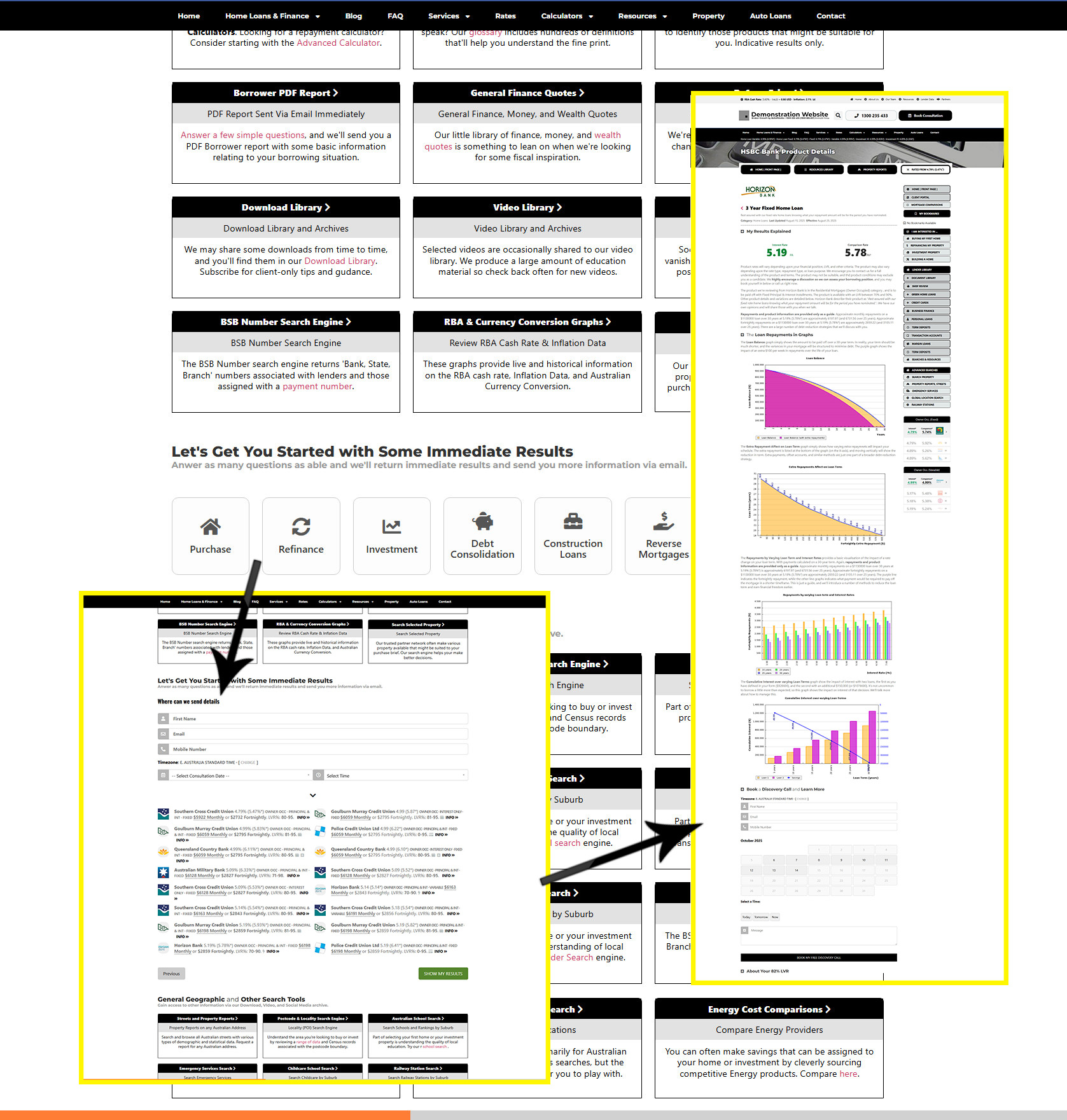

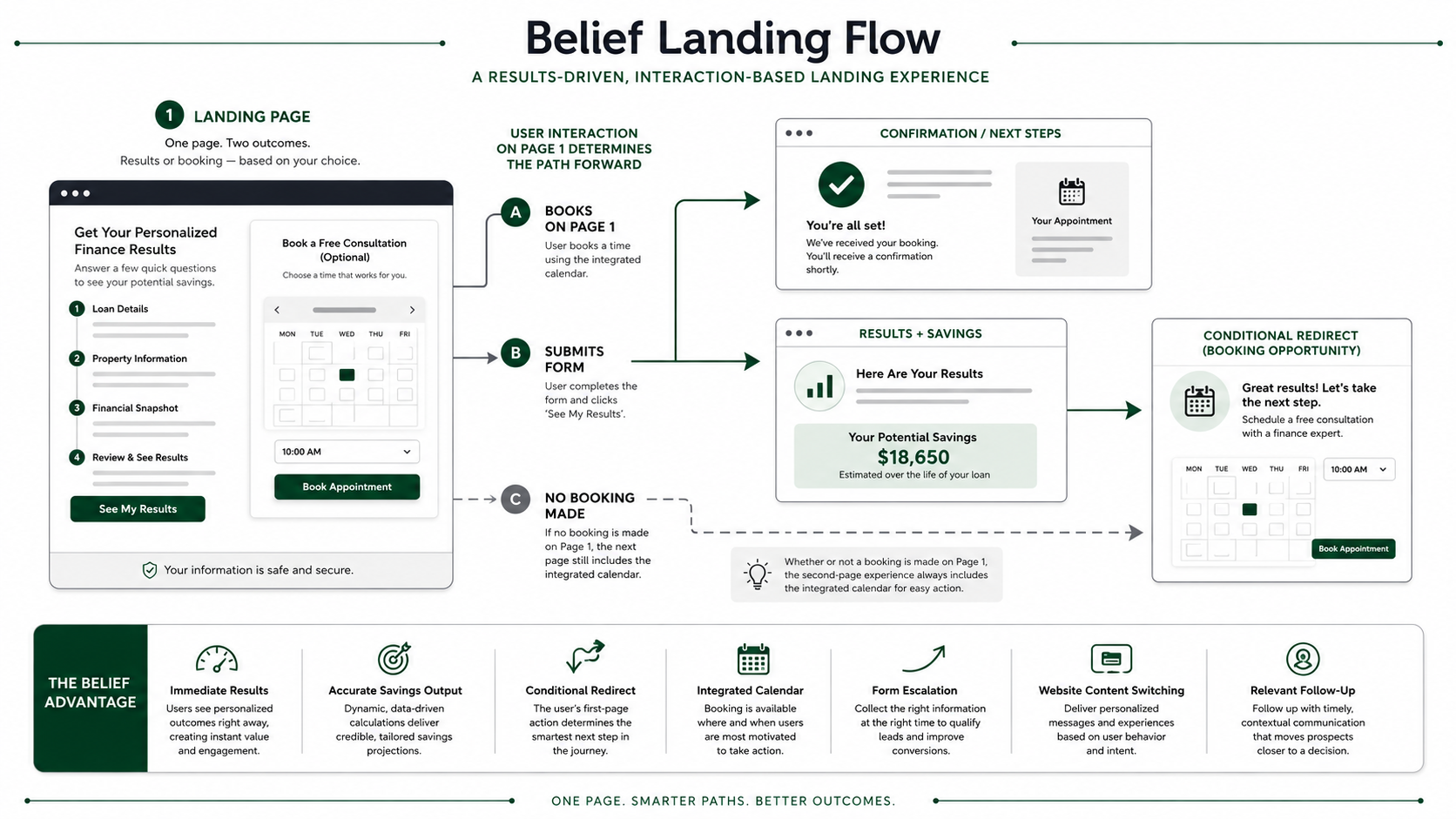

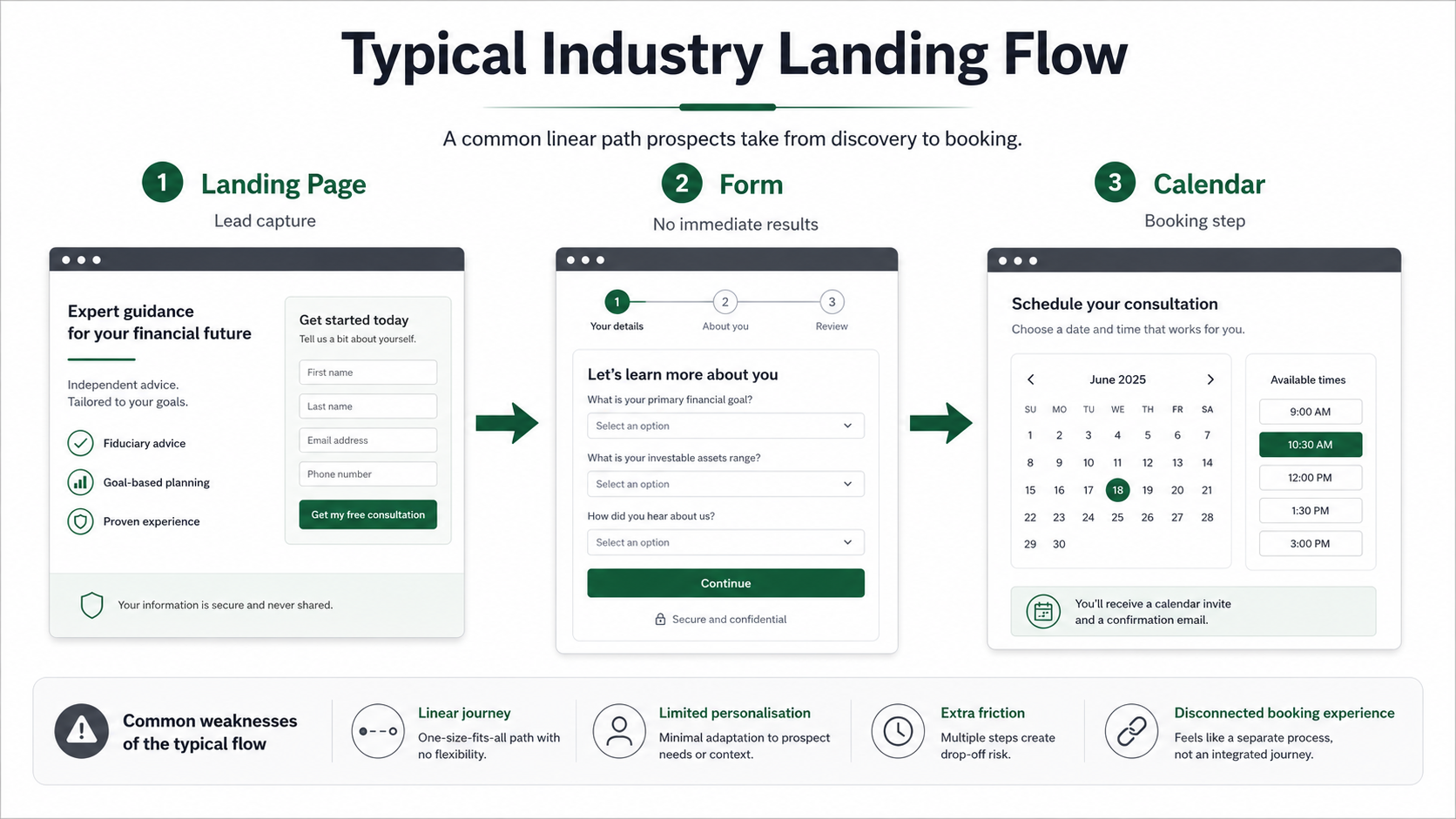

The mortgage broker website framework should be understood as two systems operating at once. On the surface, the architecture of the website tells the story of the business through a compliant public-facing infrastructure that forms the basis of a coherent framework. The page and content architecture gives your website depth, credibility, search value, education value, and commercial clarity. It makes the broker look serious, established, useful, and authoritative. But the visible page structure is only the first layer. The real power is not simply that the website contains more pages, more tools, more data, and more resources than a conventional or pedestrian broker website. The power is that those assets are connected to a broader cognitive and conditional funnel-centric conversion system. The framework becomes materially different because the website is directly integrated with funnel-focused tools and functionality. This means the website does not merely present information - it responds to interaction. A user who enters through a refinance page, completes a comparison form, watches a video, downloads a guide, clicks a rate, books a meeting, or returns to a property page should not be treated as anonymous traffic. Their behaviour should shape what happens next. Detailing how and why our…

Blog & News

Corporate litigation rarely attracts the attention of an entire industry. Most disputes between shareholders remain confined to boardrooms, courtrooms and legal practitioners, carrying little consequence beyond the commercial interests of the parties themselves. Occasionally, however, a case emerges that transcends the immediate dispute, raising broader questions about governance, commercial influence, market structure and the future direction of an entire sector. The litigation involving Connective, Slea Pty Ltd and the eventual involvement of Liberty Financial belongs firmly within that category. At first glance, the proceedings appear to concern an allegation of shareholder oppression under the Corporations Act 2001 (Cth). Such disputes are not uncommon. Australian courts routinely consider allegations that minority shareholders have been unfairly prejudiced by the conduct of those exercising control over closely held companies. The legal principles are well established, the available remedies are broadly understood, and the proceedings generally conclude with little public interest beyond those directly involved. The Connective litigation was different. Over more than a decade, what began as a dispute between former business associates evolved into one of the most significant corporate conflicts ever witnessed within Australia's mortgage broking industry. The proceedings traversed issues of shareholder oppression, fiduciary obligations, corporate restructuring, financial assistance, litigation…

Blog & News

The notion of “owning” a client list in mortgage broking is one of the most persistently misunderstood constructs in financial services law. Brokers frequently assume that the client relationship - particularly once initiated through personal rapport and ongoing servicing - attaches to the individual broker rather than the firm. Australian courts have consistently rejected this intuition where it conflicts with contractual restraint clauses, equitable obligations of confidence, and the statutory architecture governing credit activities under the National Consumer Credit Protection Act 2009 (Cth) (“NCCP Act”) and associated licensing regimes administered by ASIC. The decision in Dargan Financial Pty Ltd v Isaac [2017] NSWSC 1077 (often cited in industry disputes concerning broker mobility) is a particularly instructive case study in how Australian courts conceptualise client lists not as relational goodwill personally owned by the broker, but as protectable commercial assets of the firm, capable of equitable protection and injunctive restraint. At its core, the Dargan Financial Pty Ltd v Isaac case involved a mortgage broker who, upon transitioning to a competing business, retained and utilised a client list generated during his engagement, and further accepted approaches from former clients. The Supreme Court of New South Wales held that such conduct constituted…

Blog & News

There are remarkably few subjects within modern mortgage broking that generate greater uncertainty than the prospect of unsolicited contact. Brokers understand cold calling. They understand digital advertising, social media campaigns, referral arrangements, seminars, direct mail and purchased leads. Yet the question of whether a mortgage broker may physically walk through a neighbourhood and knock on doors occupies an unusual legal and ethical grey area. Unlike financial planners, insurance advisers and investment advisers, mortgage brokers operate within a legislative framework that sits primarily within consumer credit law rather than financial product law. This distinction has historically created the perception that activities prohibited elsewhere within financial services may somehow remain available to credit representatives. The reality is substantially more complicated. Australian regulation has evolved considerably during the past two decades. Following the Global Financial Crisis, the introduction of the National Consumer Credit Protection Act 2009, the findings of the Financial Services Royal Commission, the introduction of Best Interests Duty and the subsequent anti-hawking reforms, the regulatory environment has increasingly moved toward a philosophy of consumer initiation rather than intermediary pursuit. The modern mortgage broker is no longer regarded merely as a salesperson introducing loan products. The broker is now treated as a…

Blog & News

The increasing digitisation of credit intermediation has produced a structural evolution in how credit assistance is delivered, particularly through embedded third-party forms hosted within broker or aggregator-controlled digital environments. While such arrangements are often presented as operational efficiencies or specialist referral pathways, their legal and regulatory implications under the National Consumer Credit Protection Act 2009 (Cth) (NCCP Act), the Australian Credit Licence (ACL) regime, the Privacy Act 1988 (Cth), and ASIC’s Regulatory Guide 209 (RG 209) and Regulatory Guide 234 (RG 234) raise complex questions regarding disclosure adequacy, consumer understanding, conflict neutrality, and the integrity of Best Interests Duty obligations. A further and increasingly prevalent dimension of concern arises in relation to equipment finance and asset funding providers supplying embedded referral forms for use within mortgage broker digital environments, which are configured to automatically redirect or filter any enquiry outside residential mortgage lending directly to the originating equipment finance provider. In substance, these mechanisms operate as pre-programmed allocation filters that segment consumer demand at the point of data capture, often without contemporaneous and meaningful disclosure to the consumer regarding the identity of the ultimate credit assistance provider or the commercial basis upon which that reallocation occurs. While such arrangements are…

Blog & News

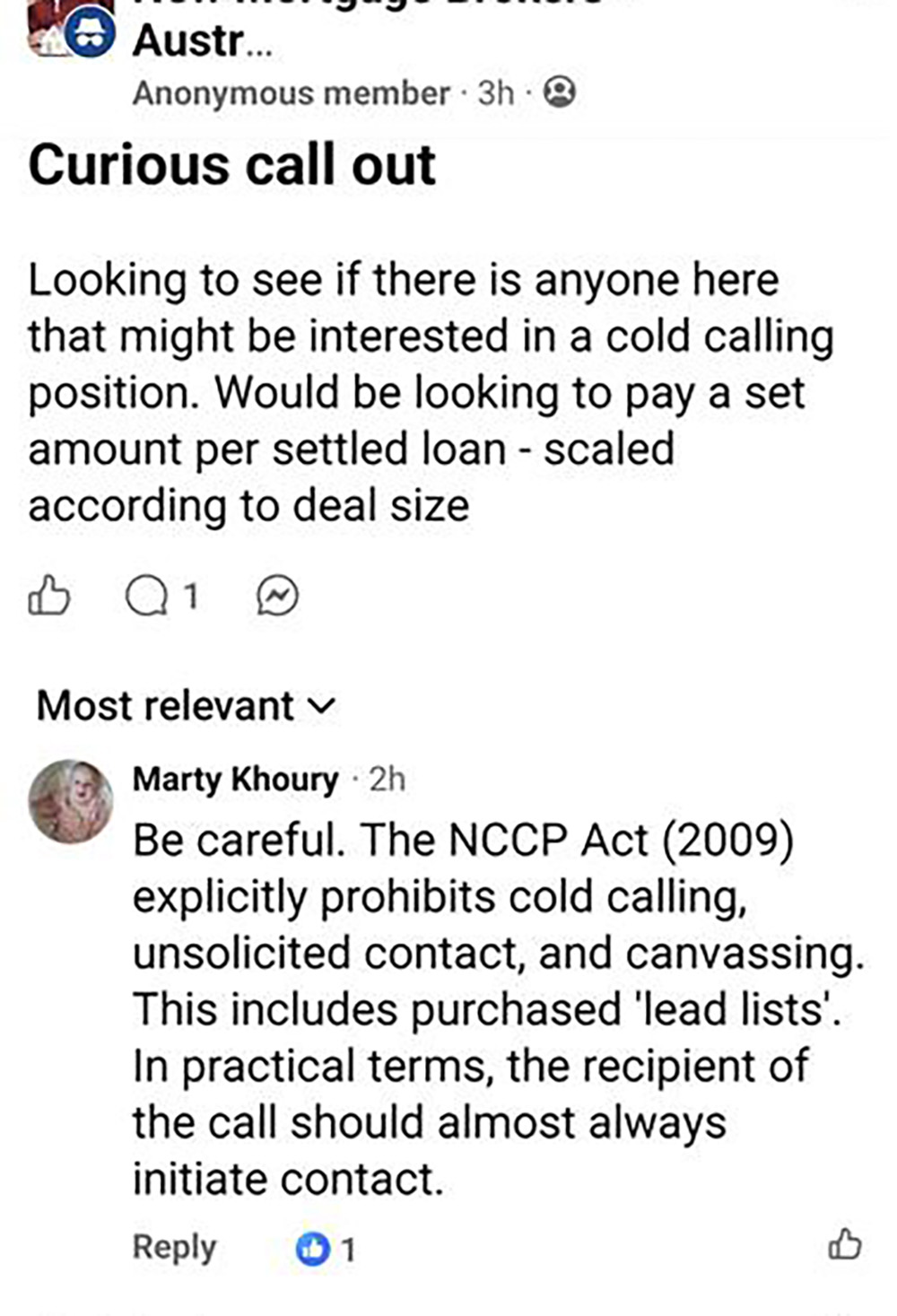

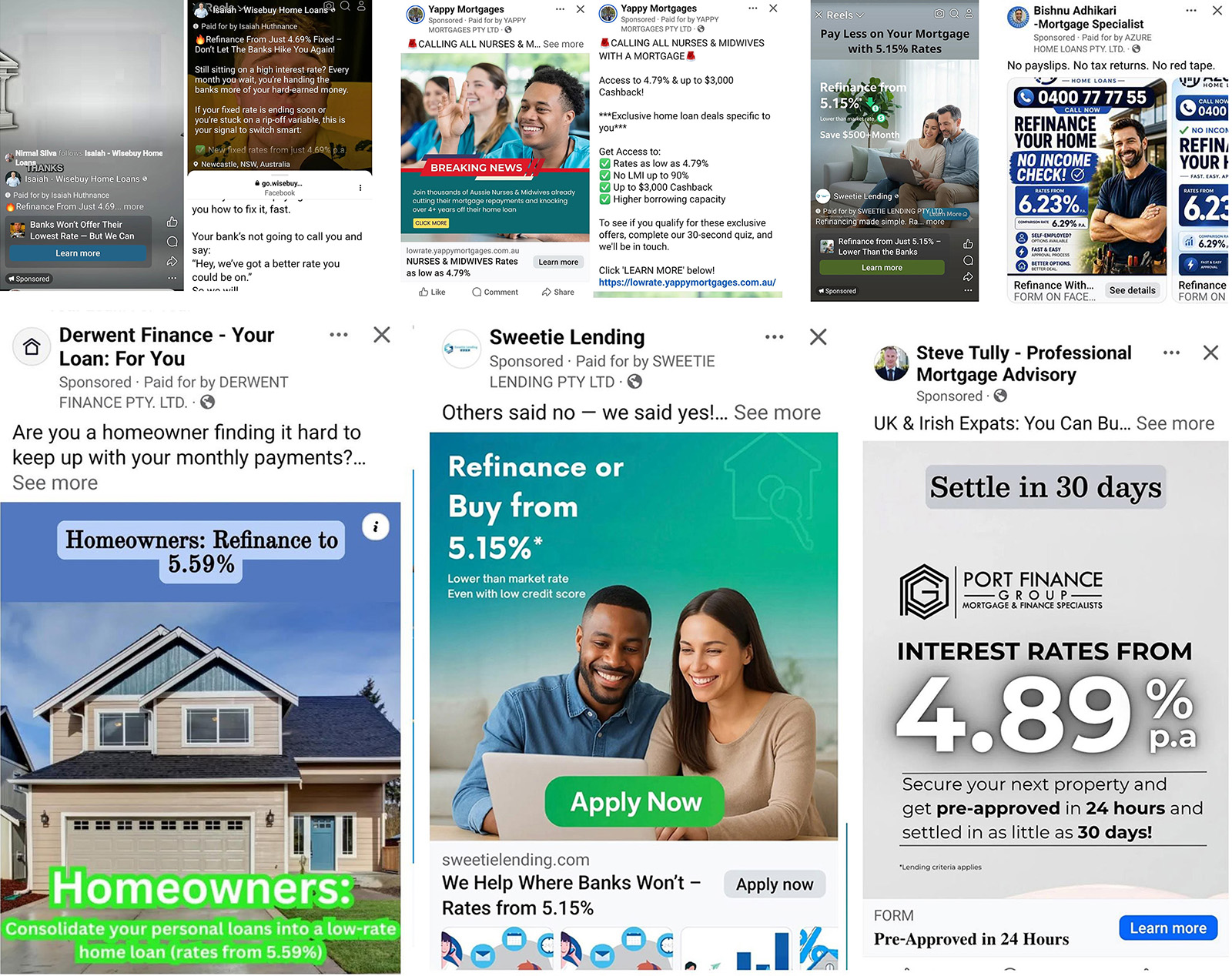

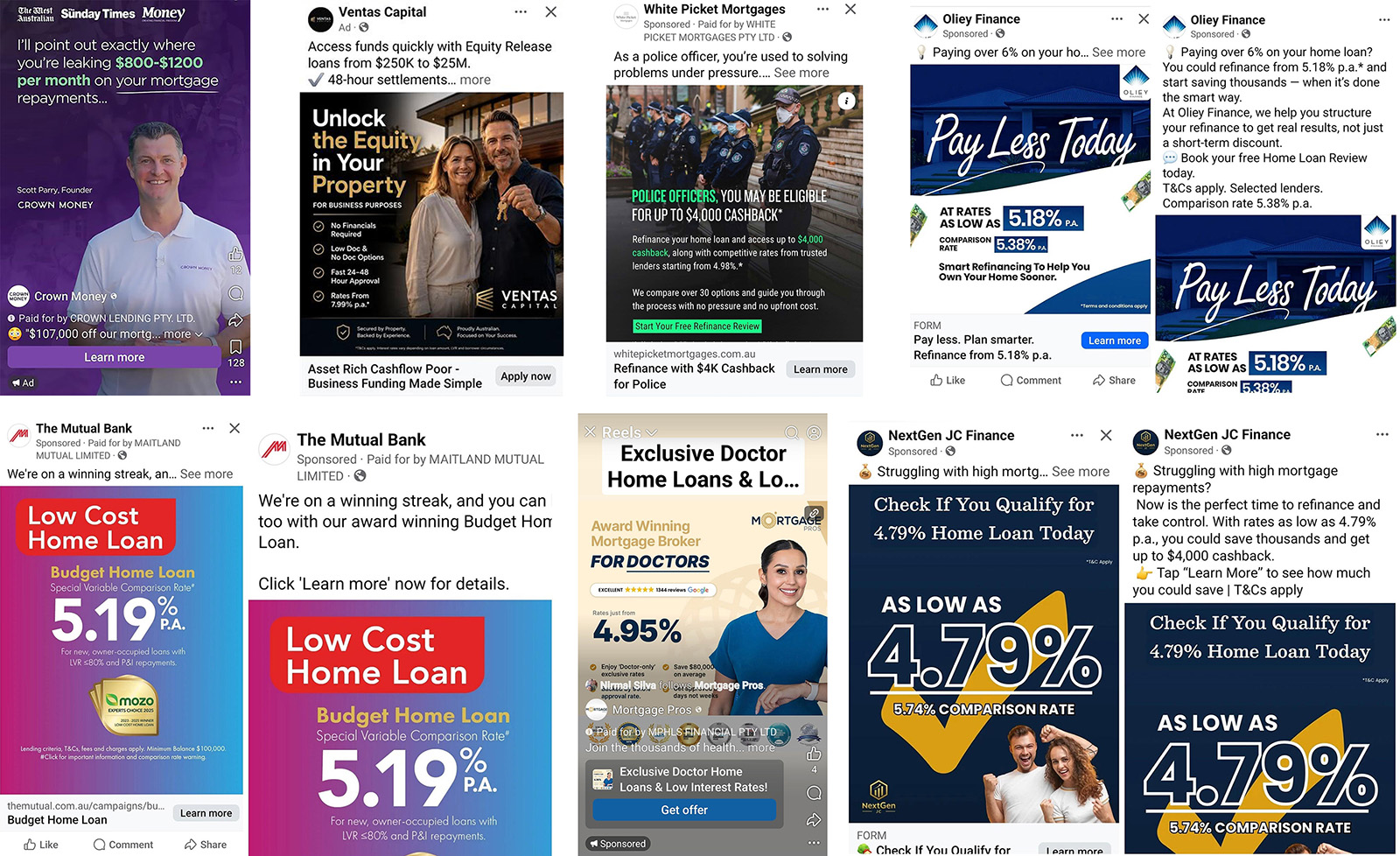

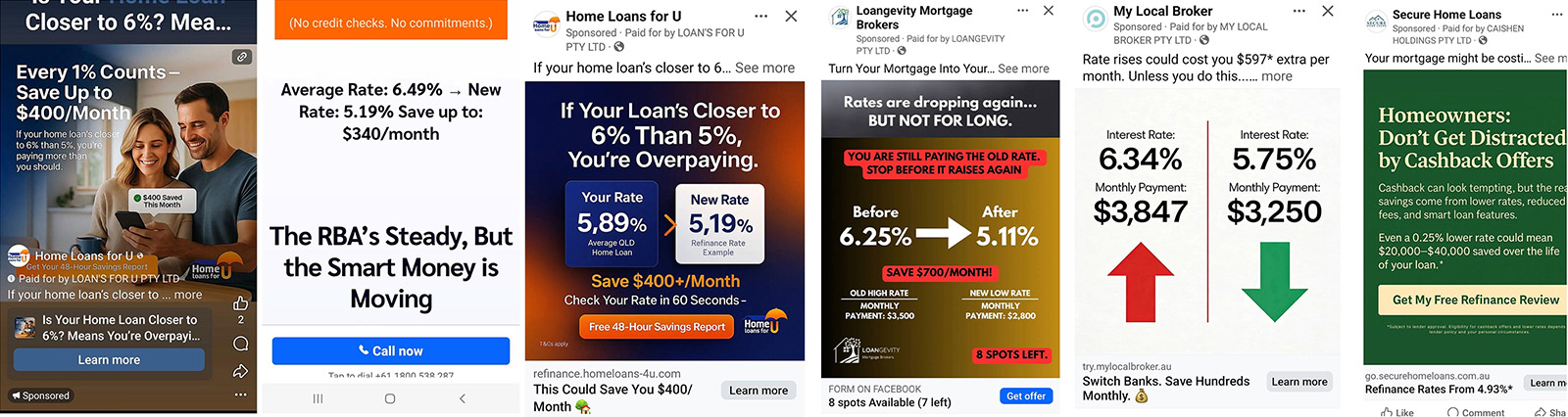

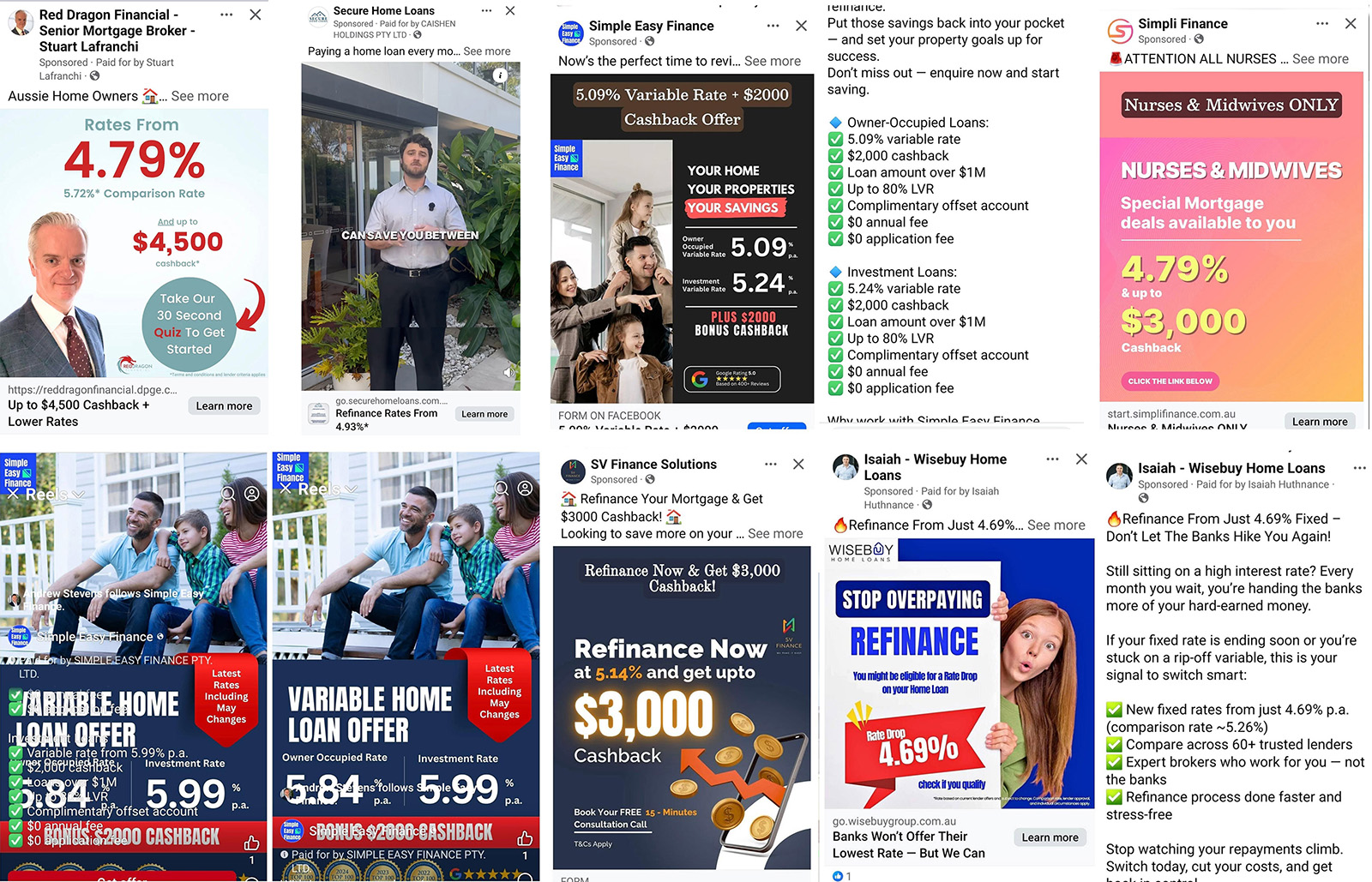

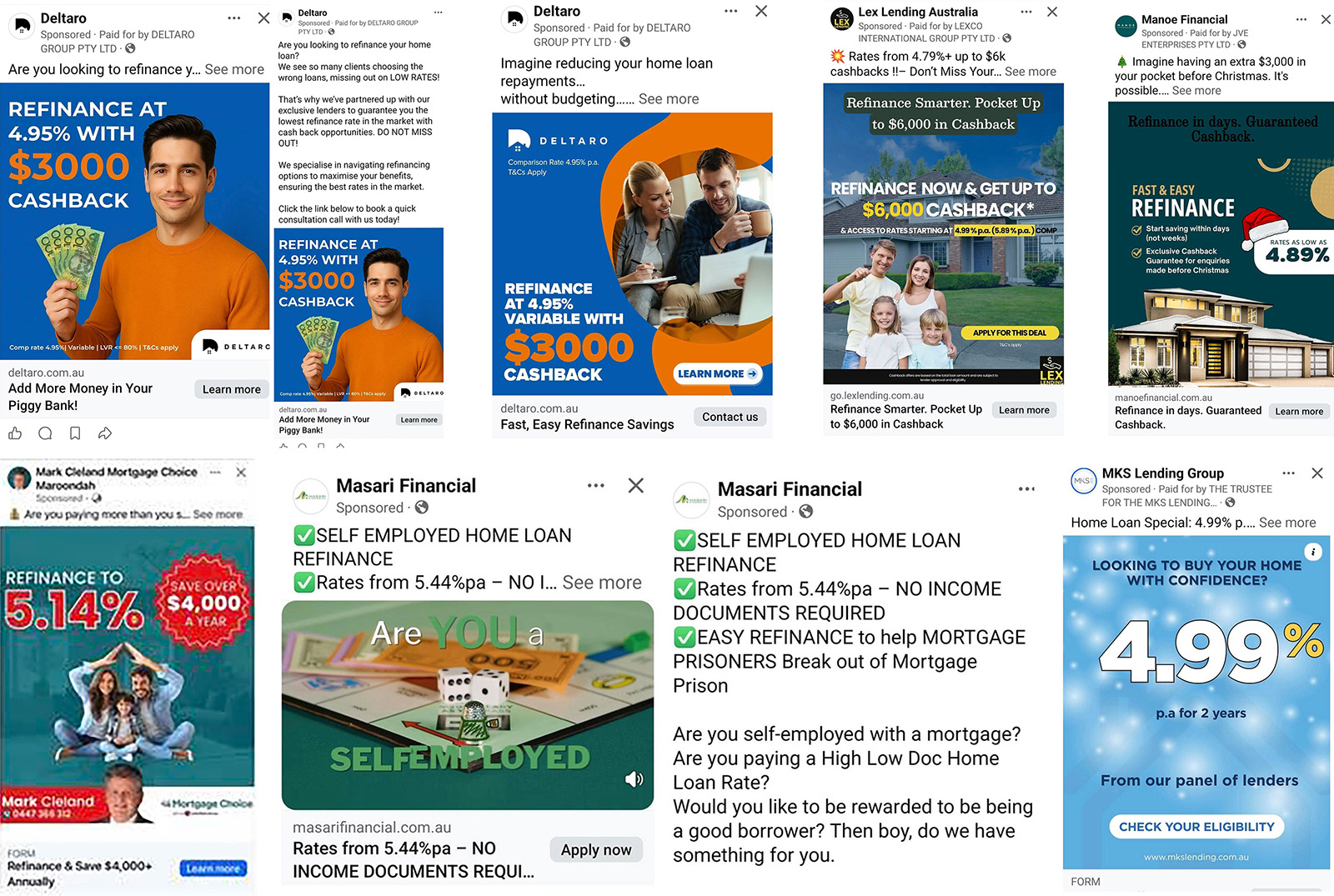

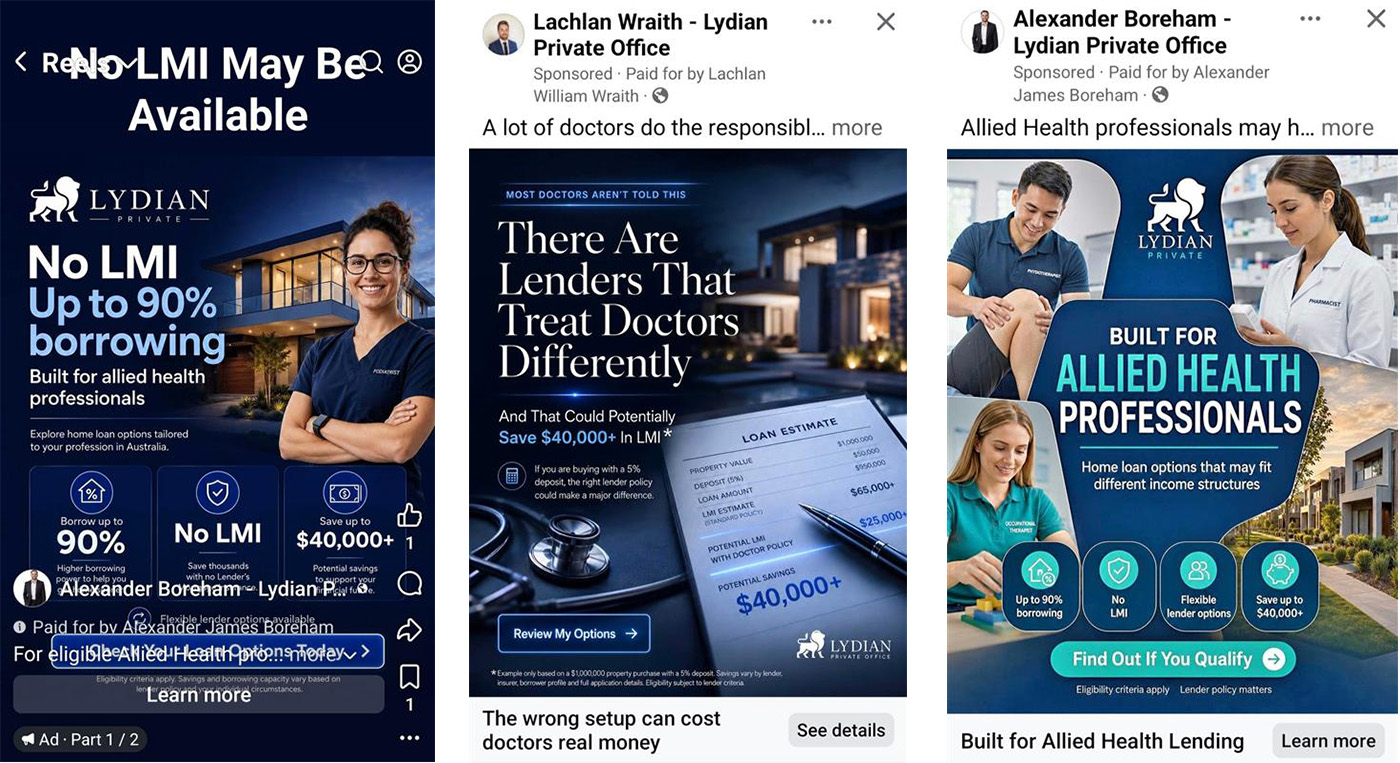

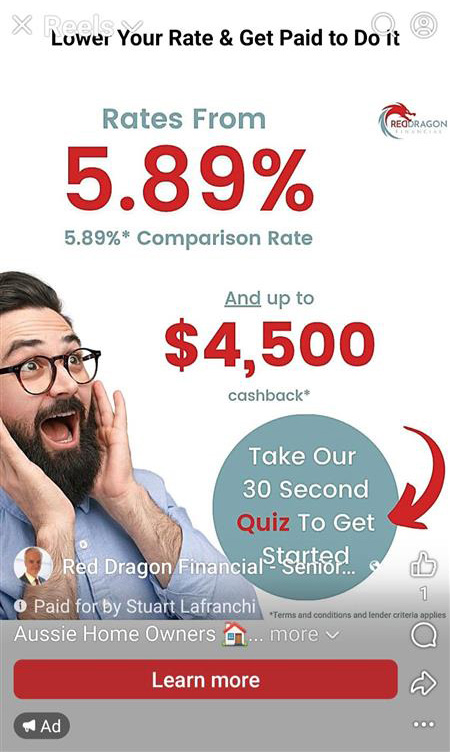

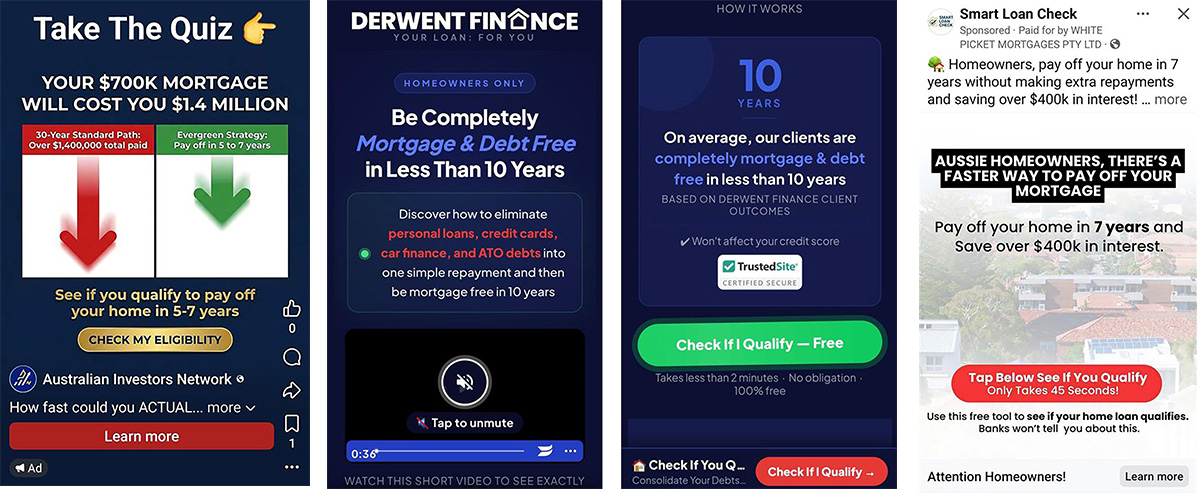

I came across a today where a broker was scouting for an individual for the purpose of cold calling potential mortgage clients with renumeration determined by the loan size. Apart from the fact that the employment conditions are typically appalling, the role itself is one that exposes significant legal exposure. First, the person making these 'cold calls' is engaging with 'credit activities' in a manner not unlike illegal '', and the role itself is objectively illegal and the subject of very specific legislation. In this article, we'll look at the colder style of marketing which includes phone calls, LinkedIn and other social platforms, open home records, and general canvassing. Unsolicited cold calling for mortgage products is heavily restricted and, in most practical circumstances, prohibited. The relevant provisions sit within the Australian consumer credit regime under the National Consumer Credit Protection Act 2009, particularly the rules dealing with unsolicited contact and hawking. A mortgage broker, lender, or their representative generally cannot simply telephone a consumer out of the blue to promote or arrange a home loan if the consumer has not consented to the contact, so cold calling is expressly prohibited. There are several legal frameworks operating simultaneously as it relates…

Blog & News

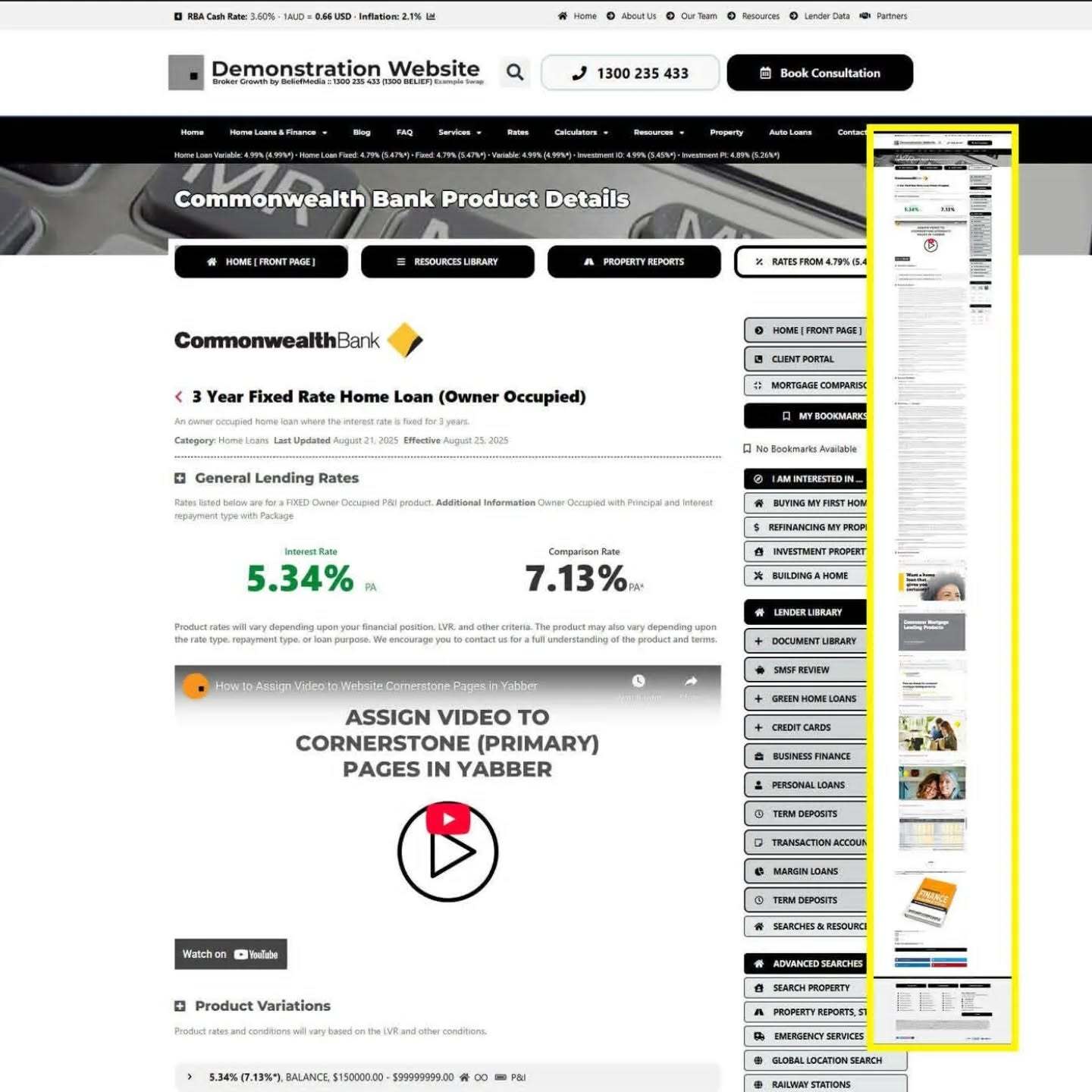

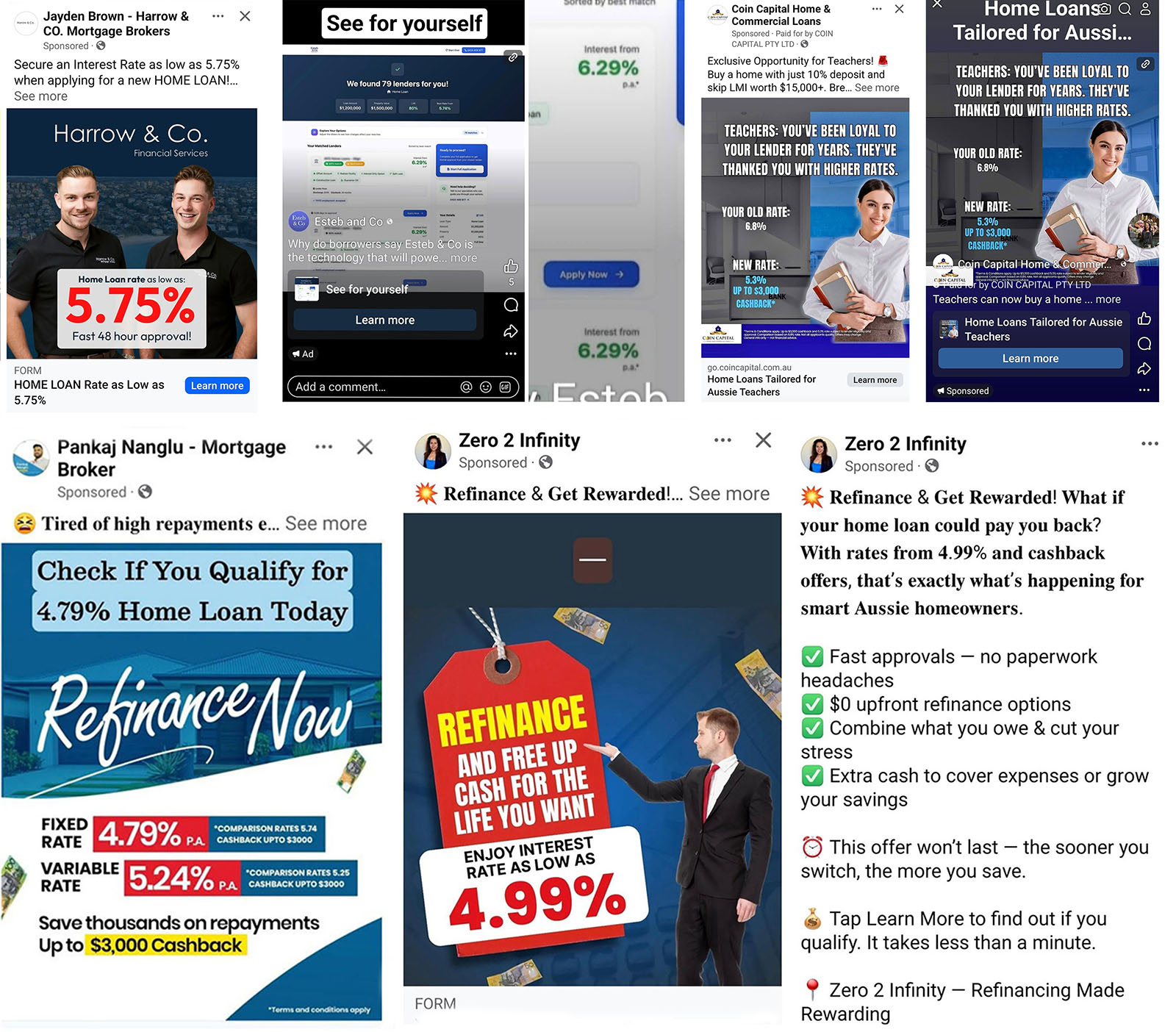

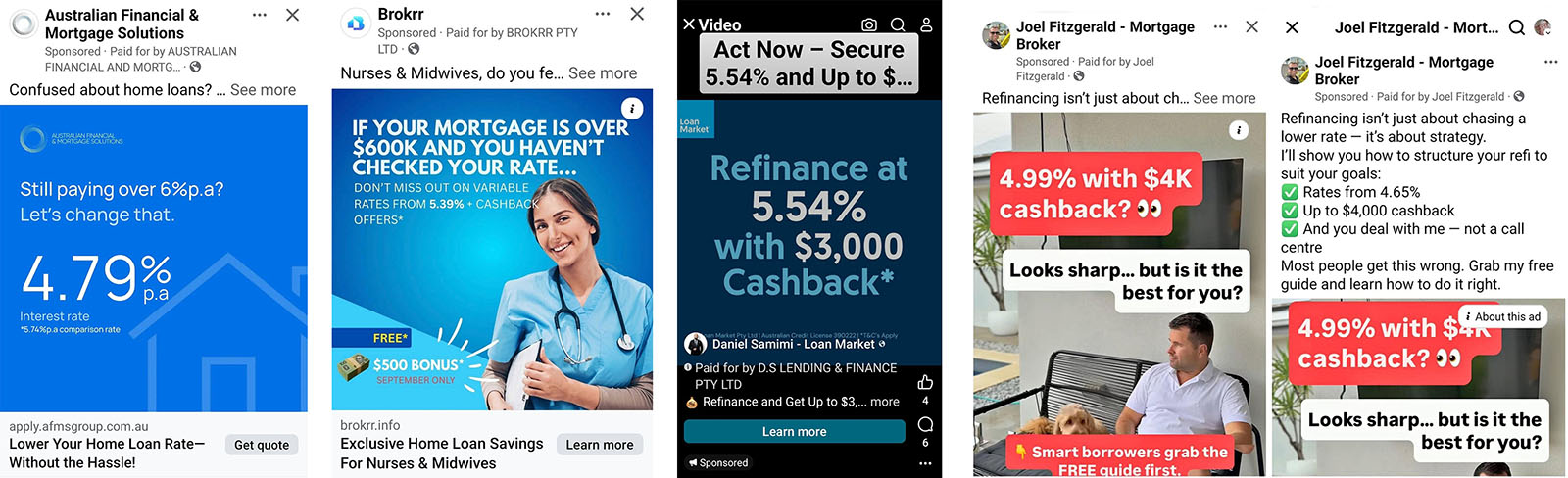

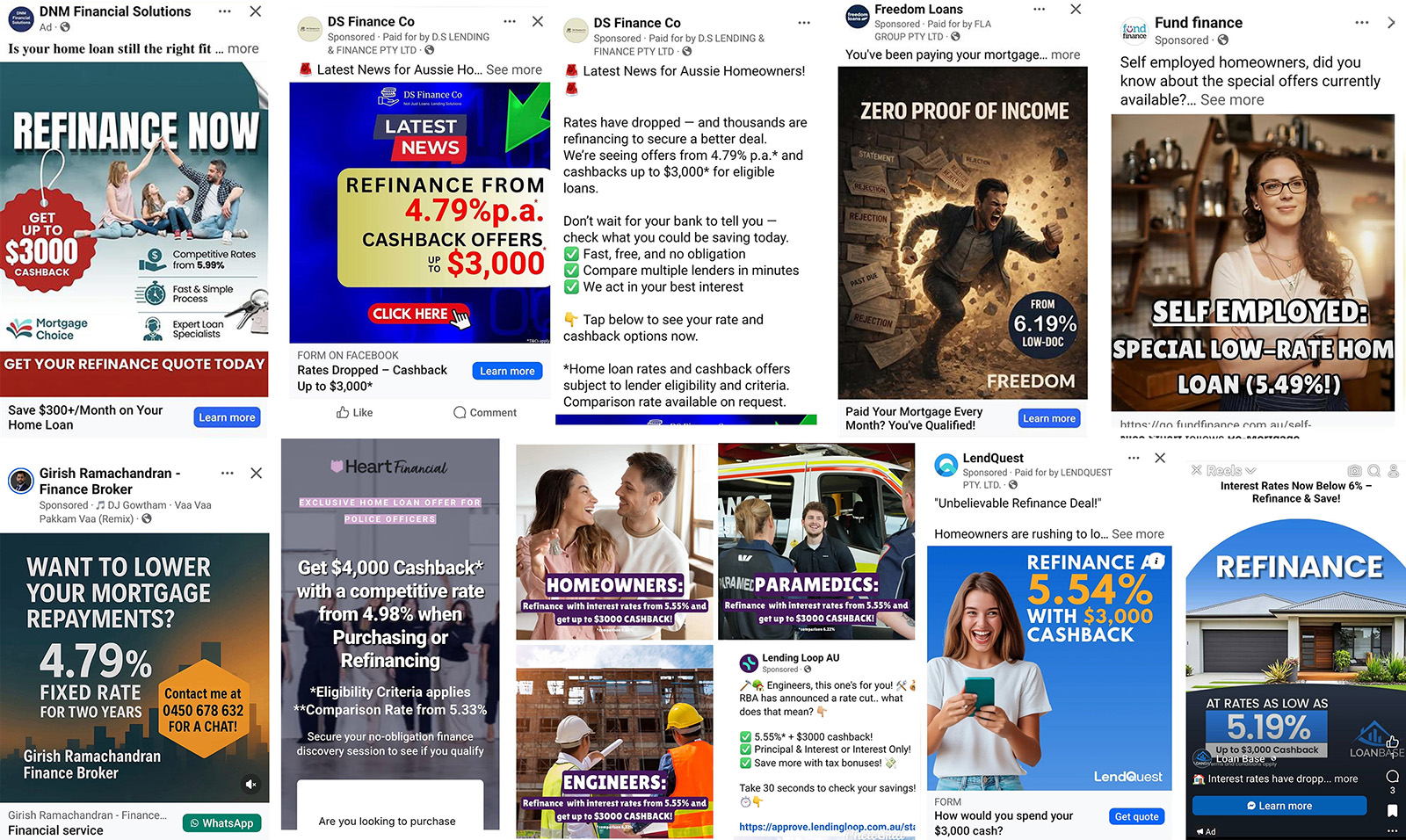

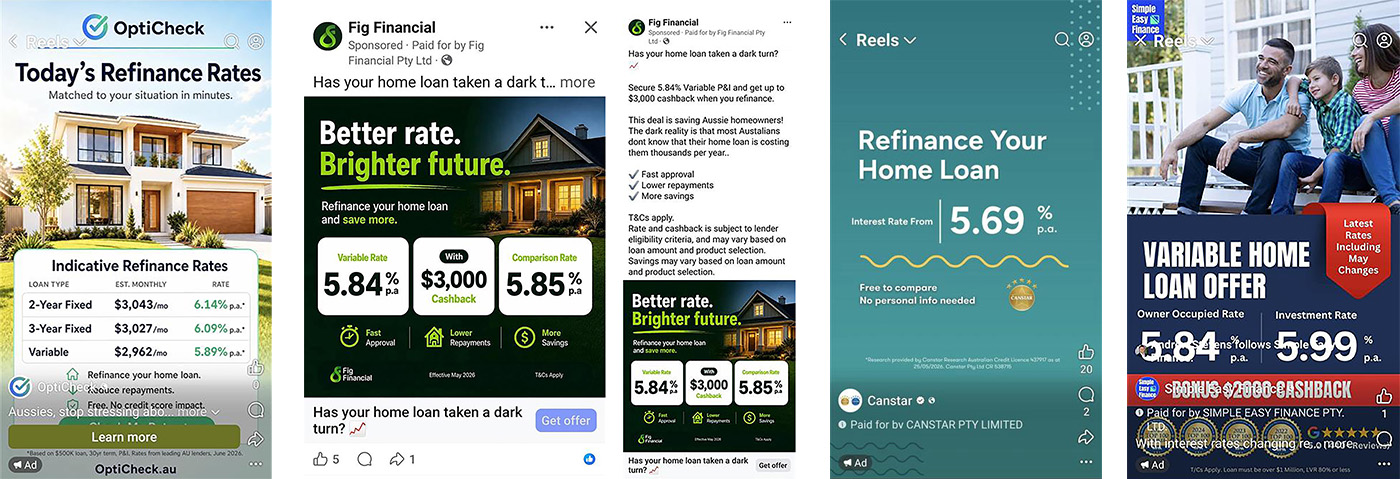

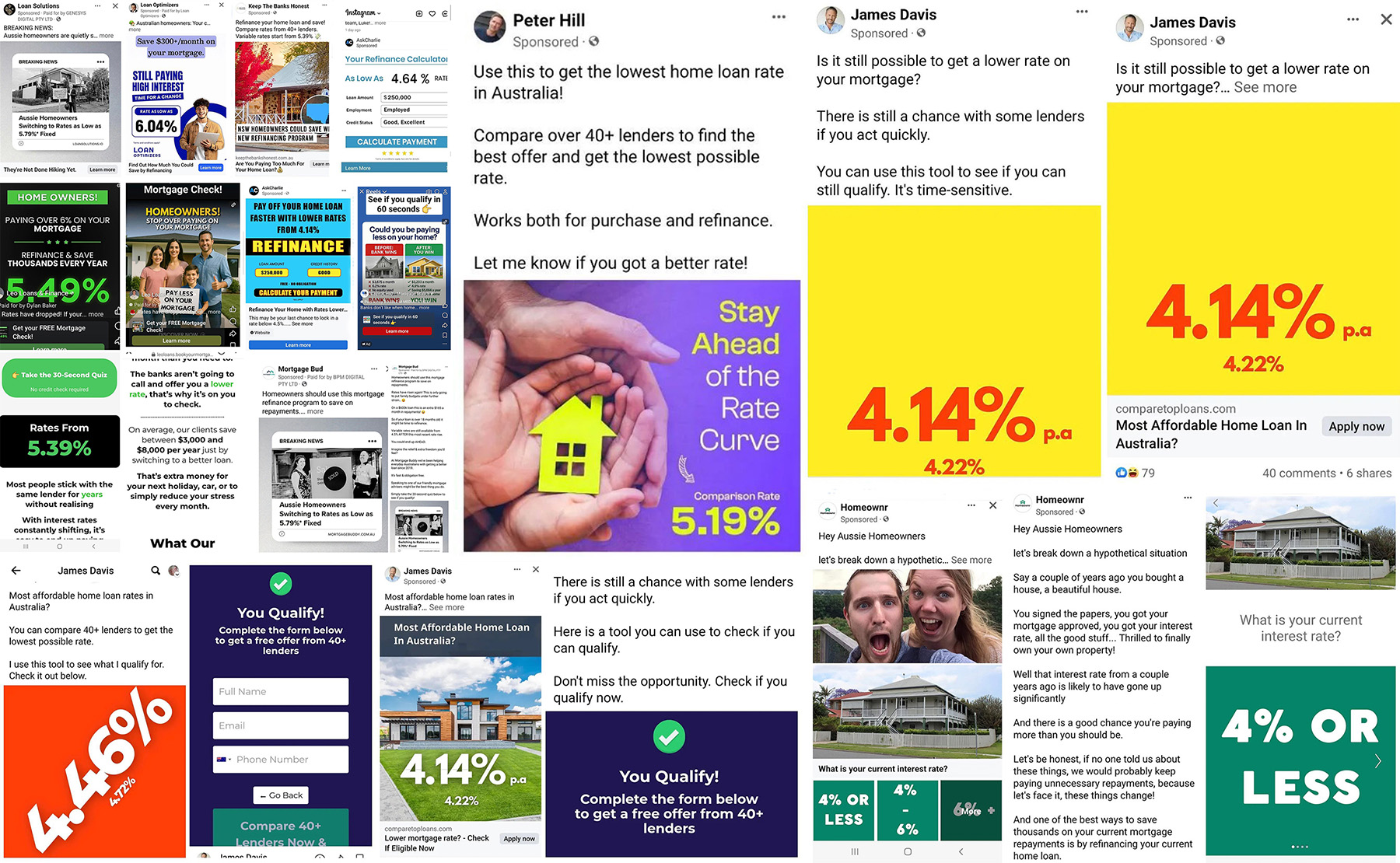

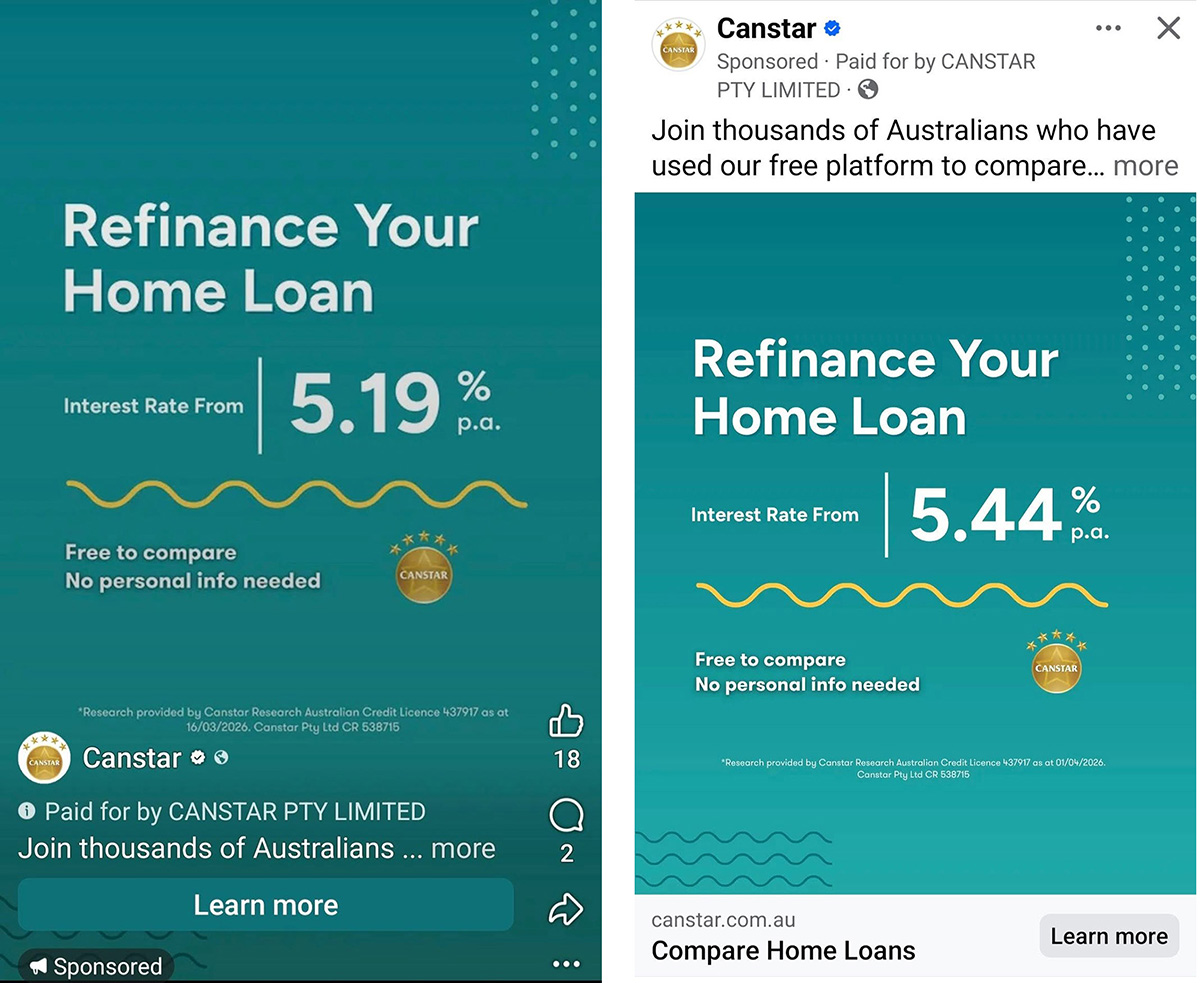

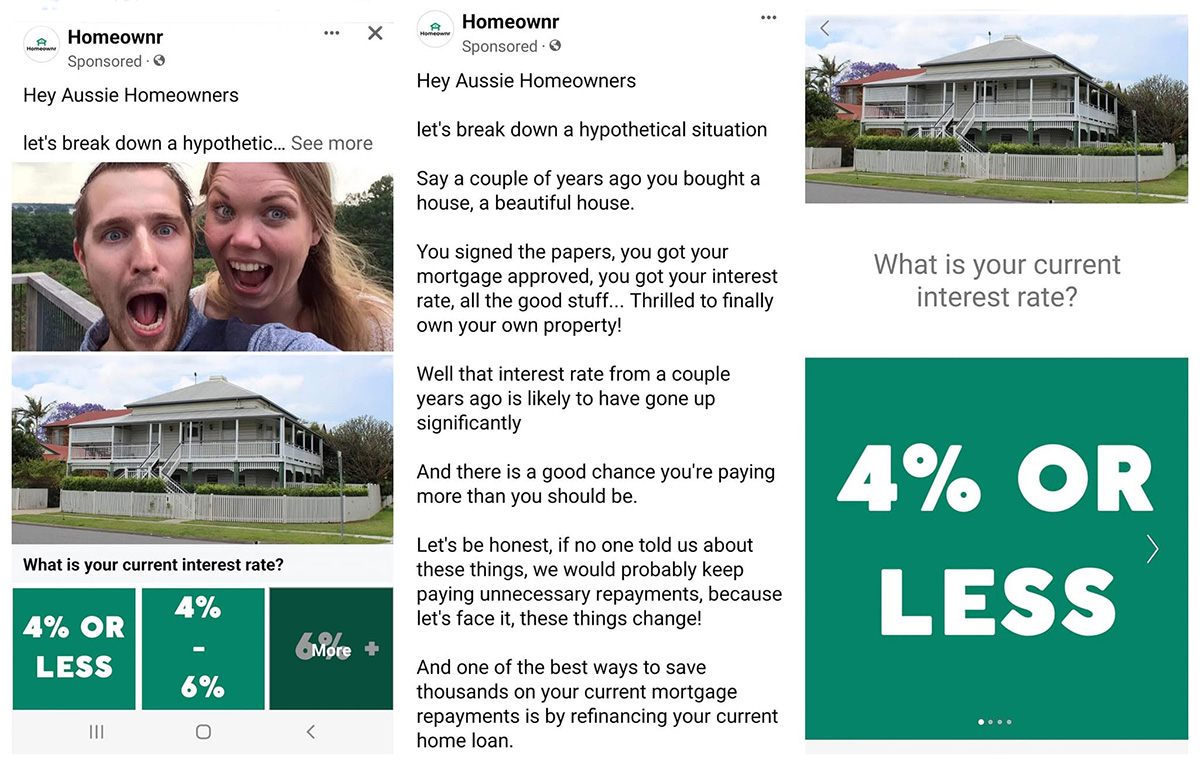

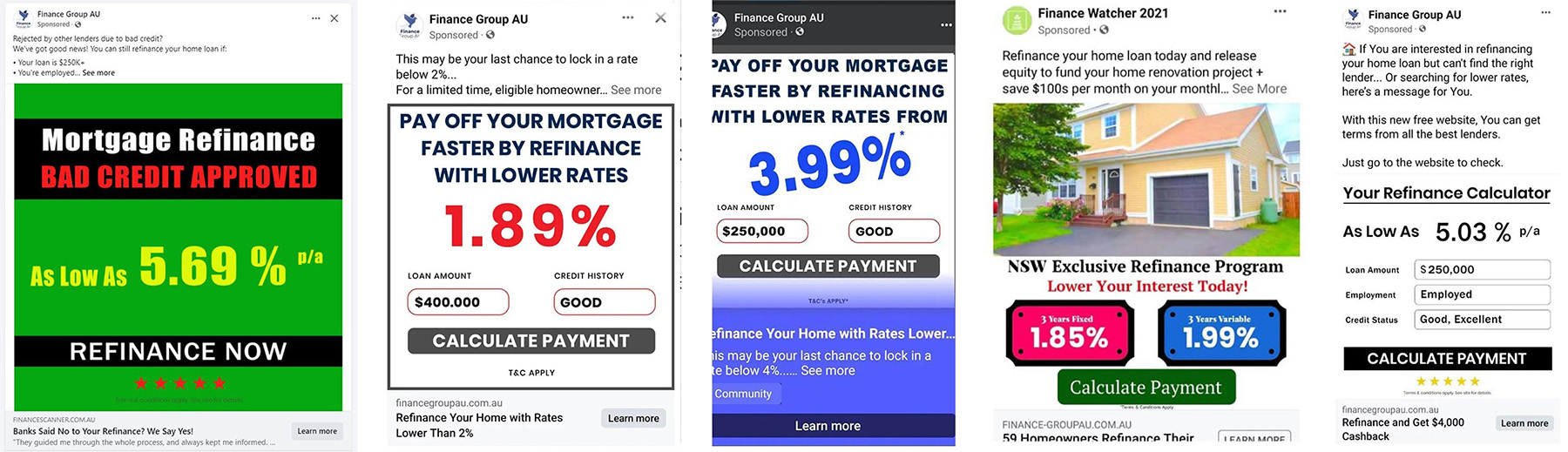

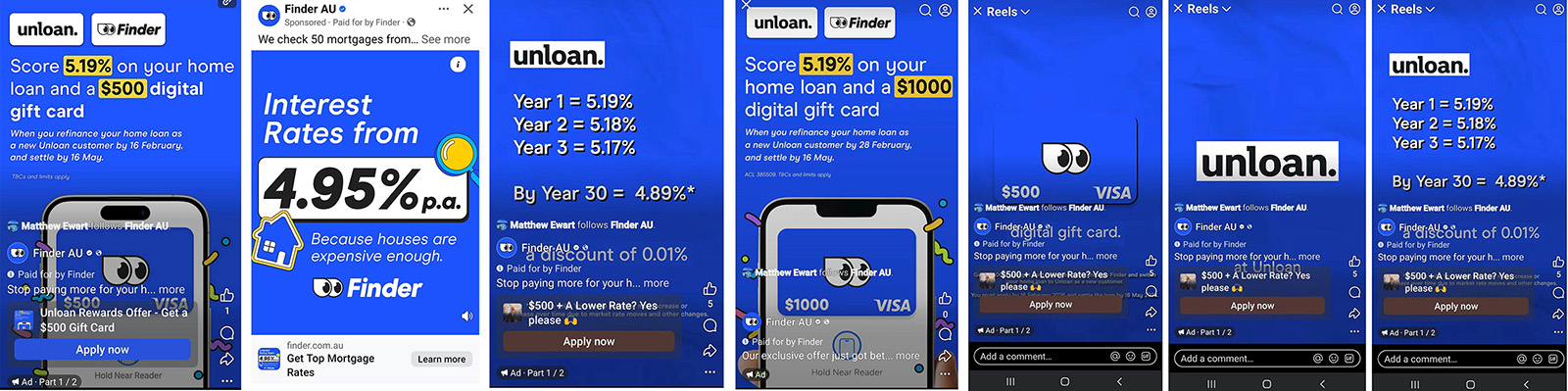

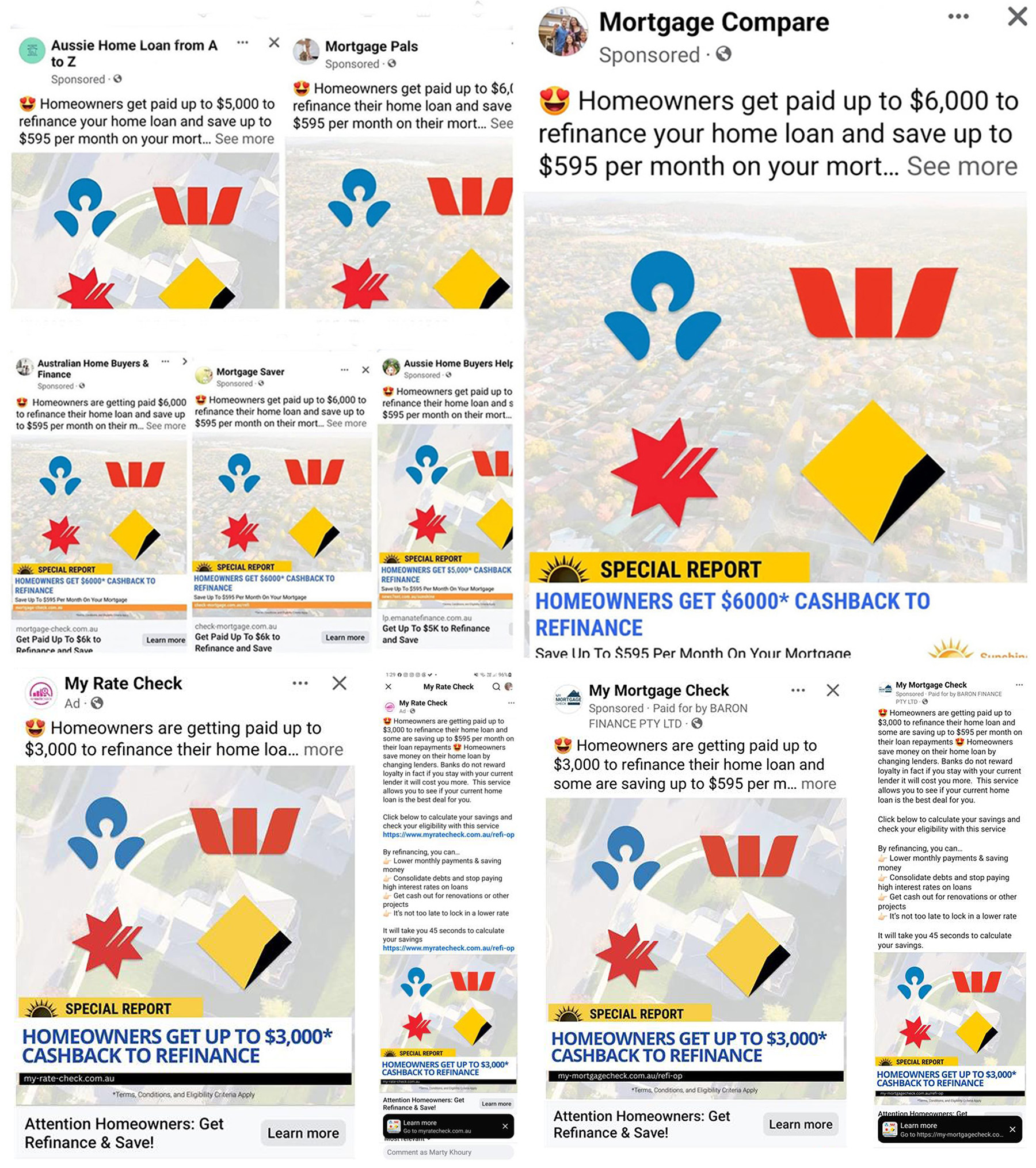

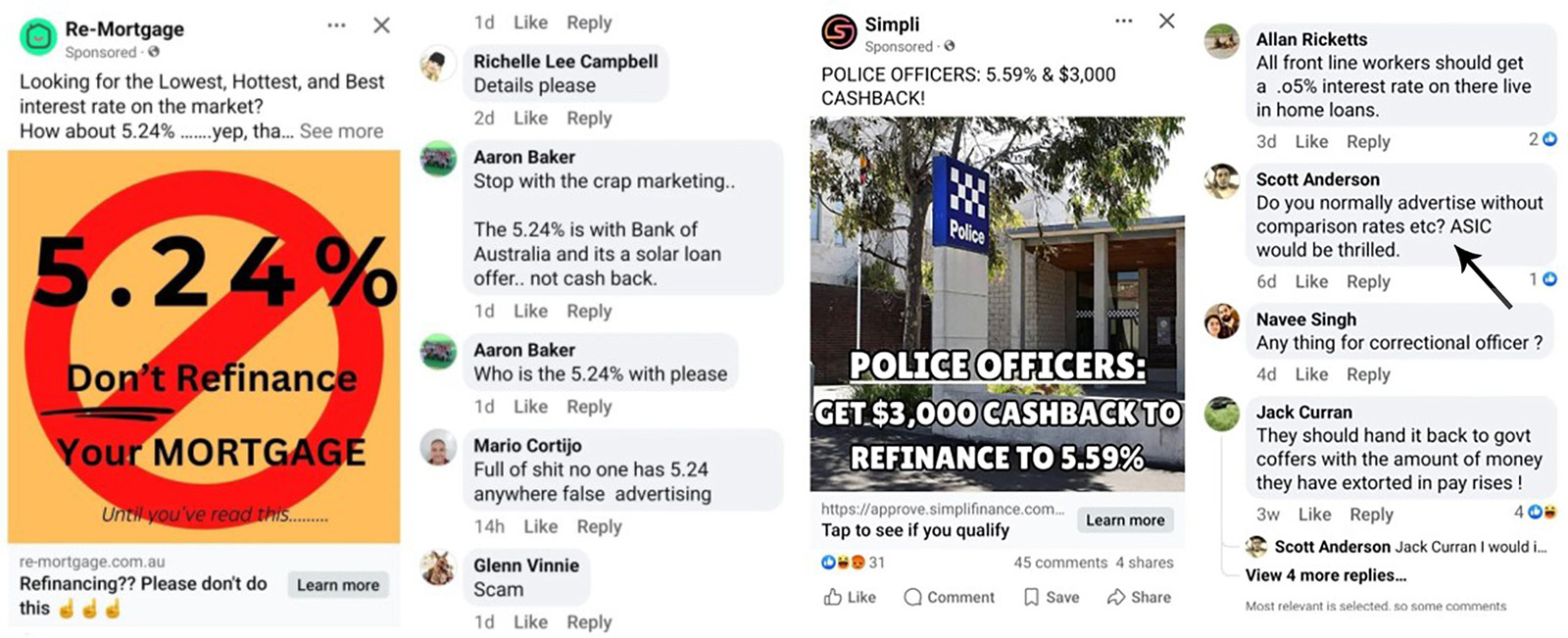

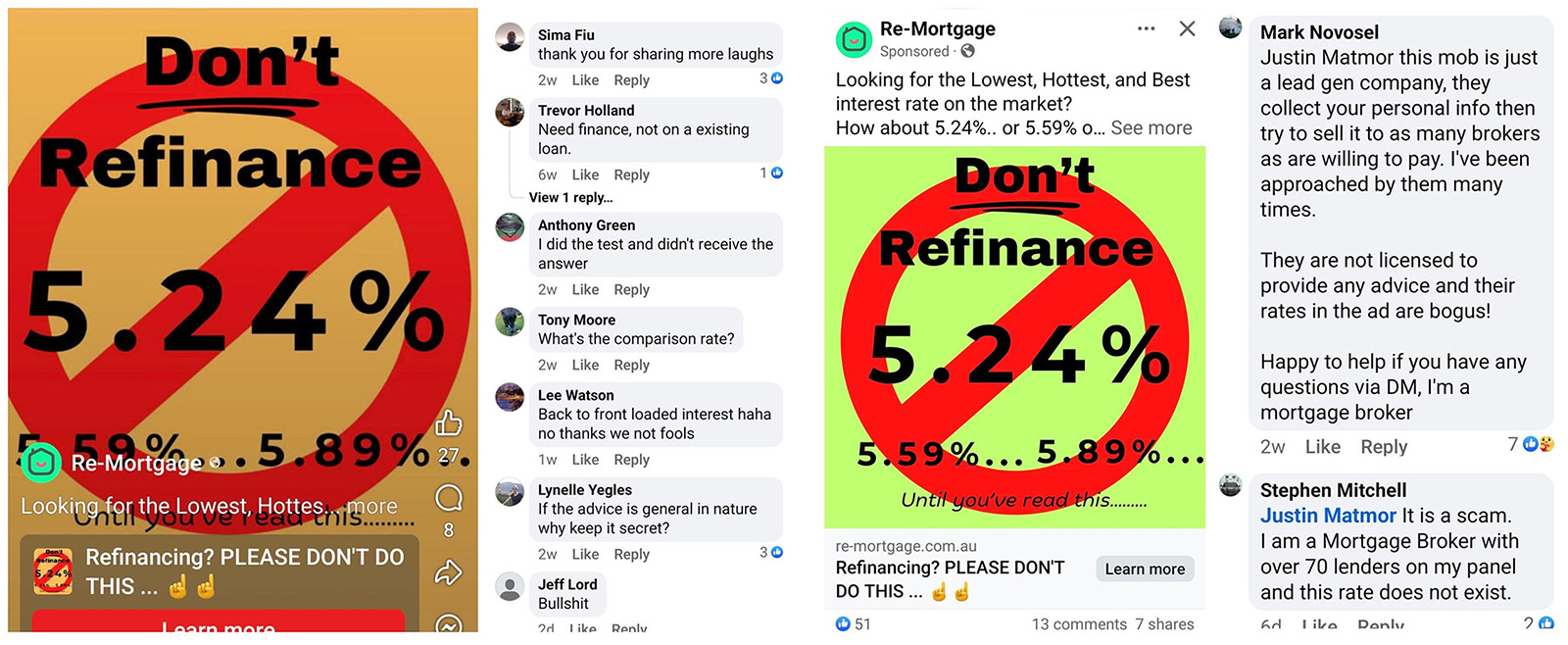

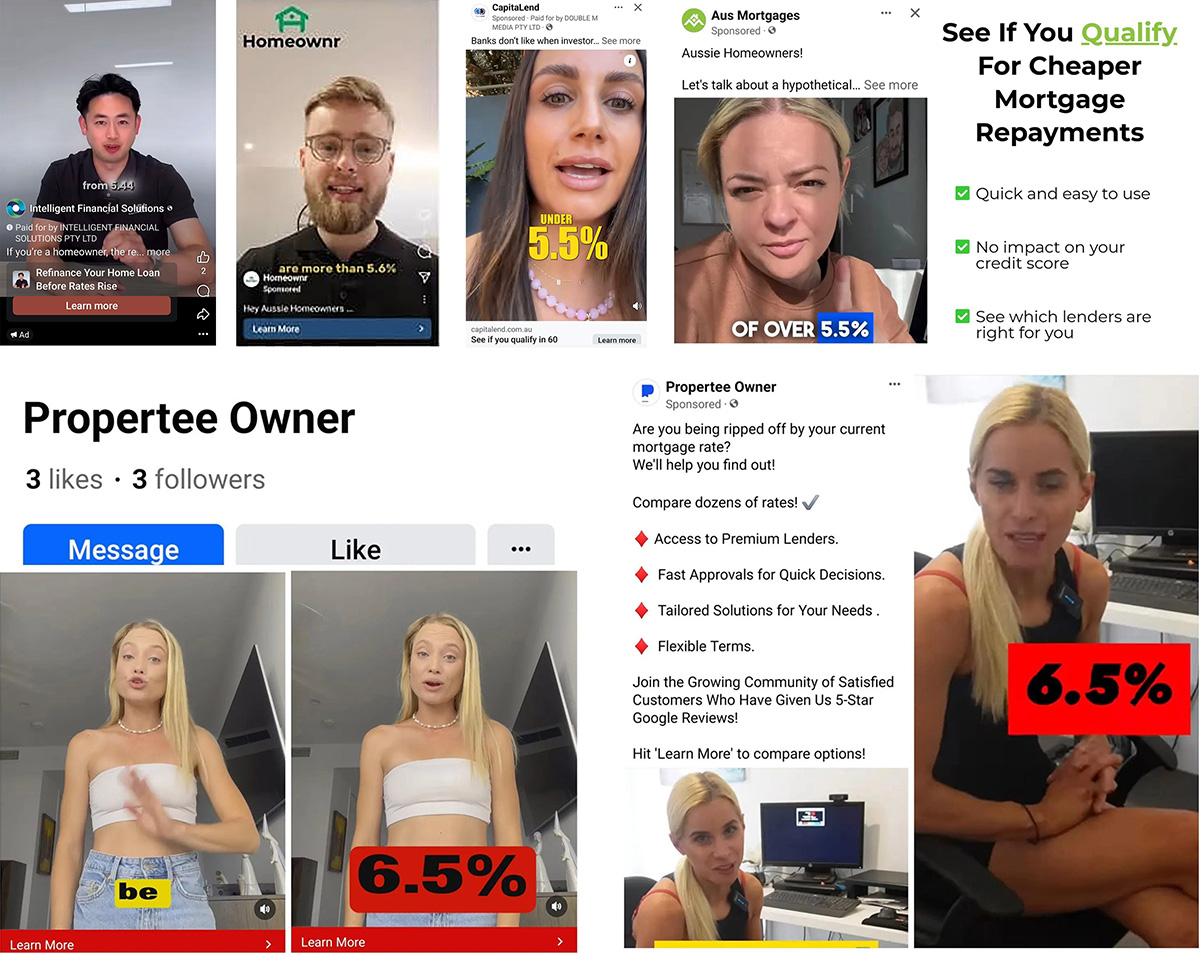

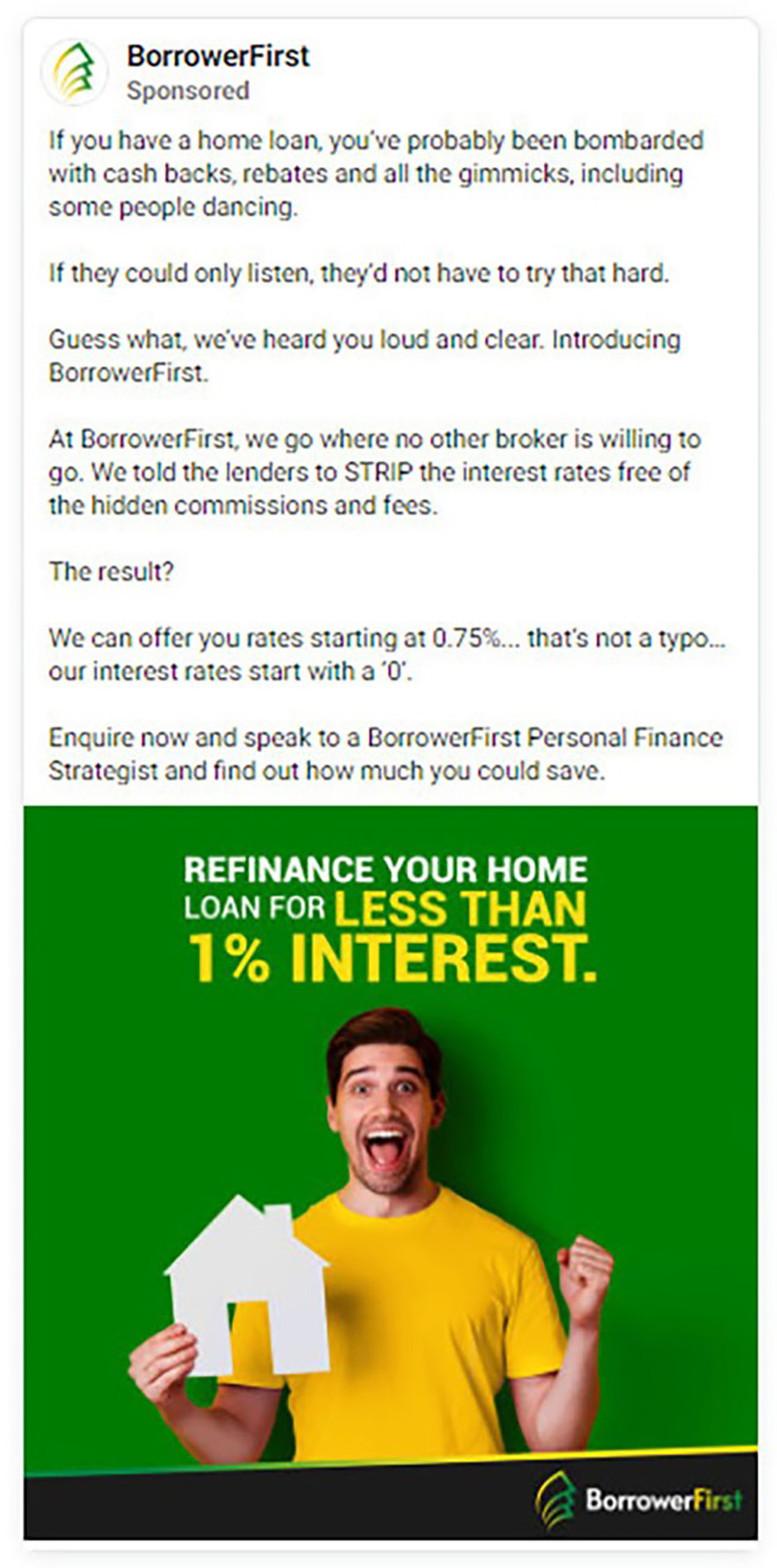

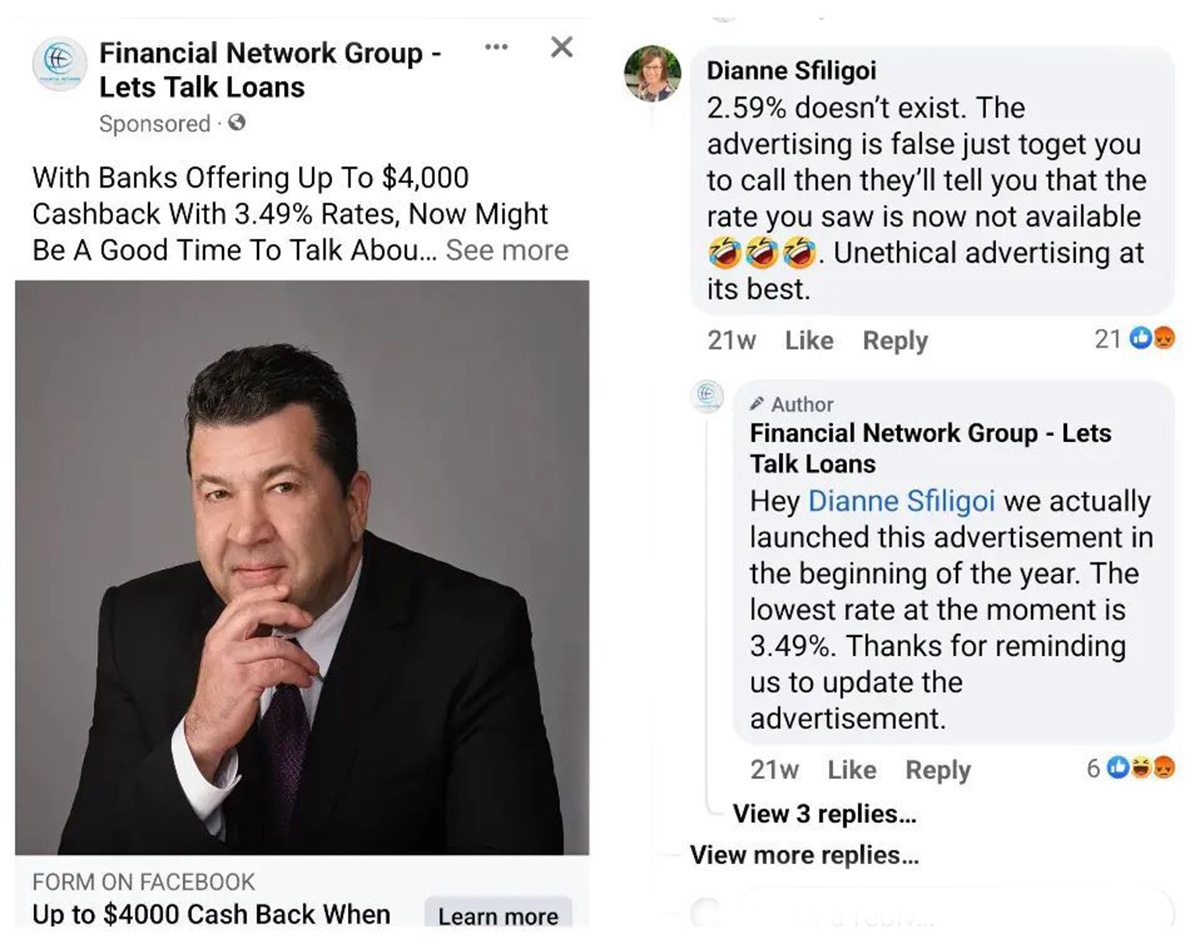

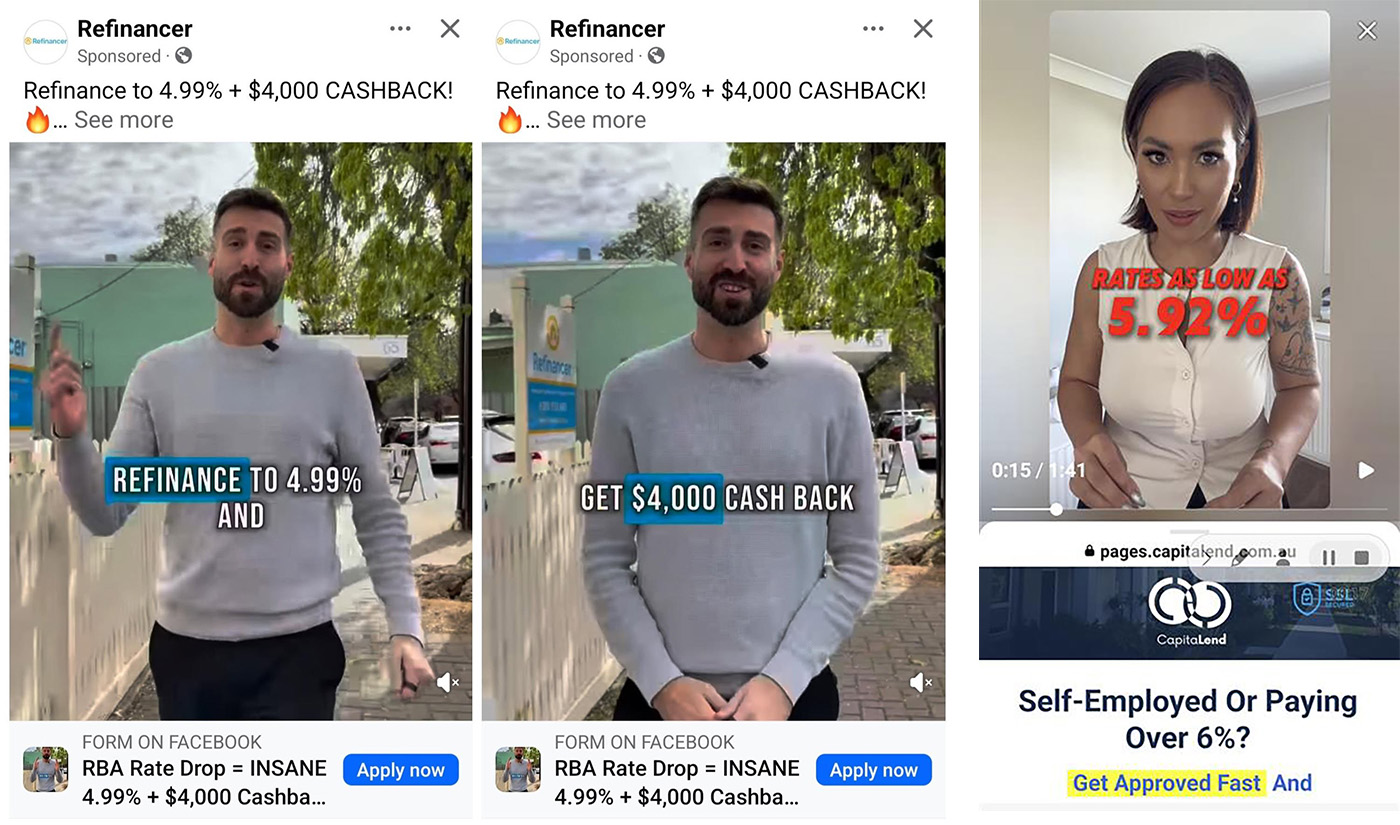

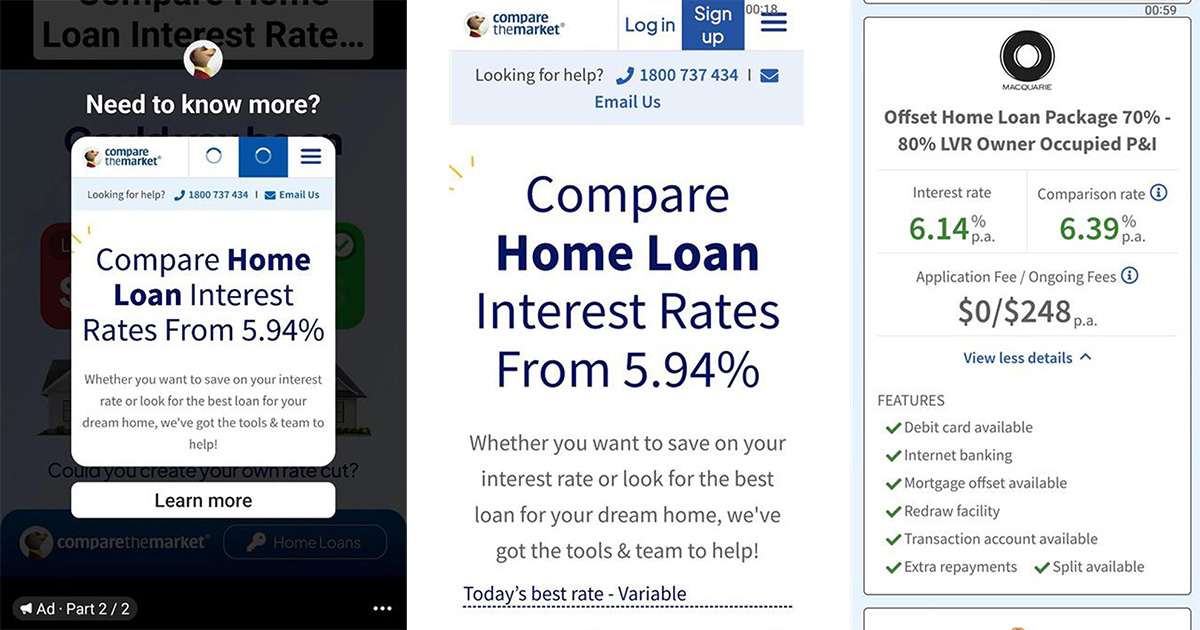

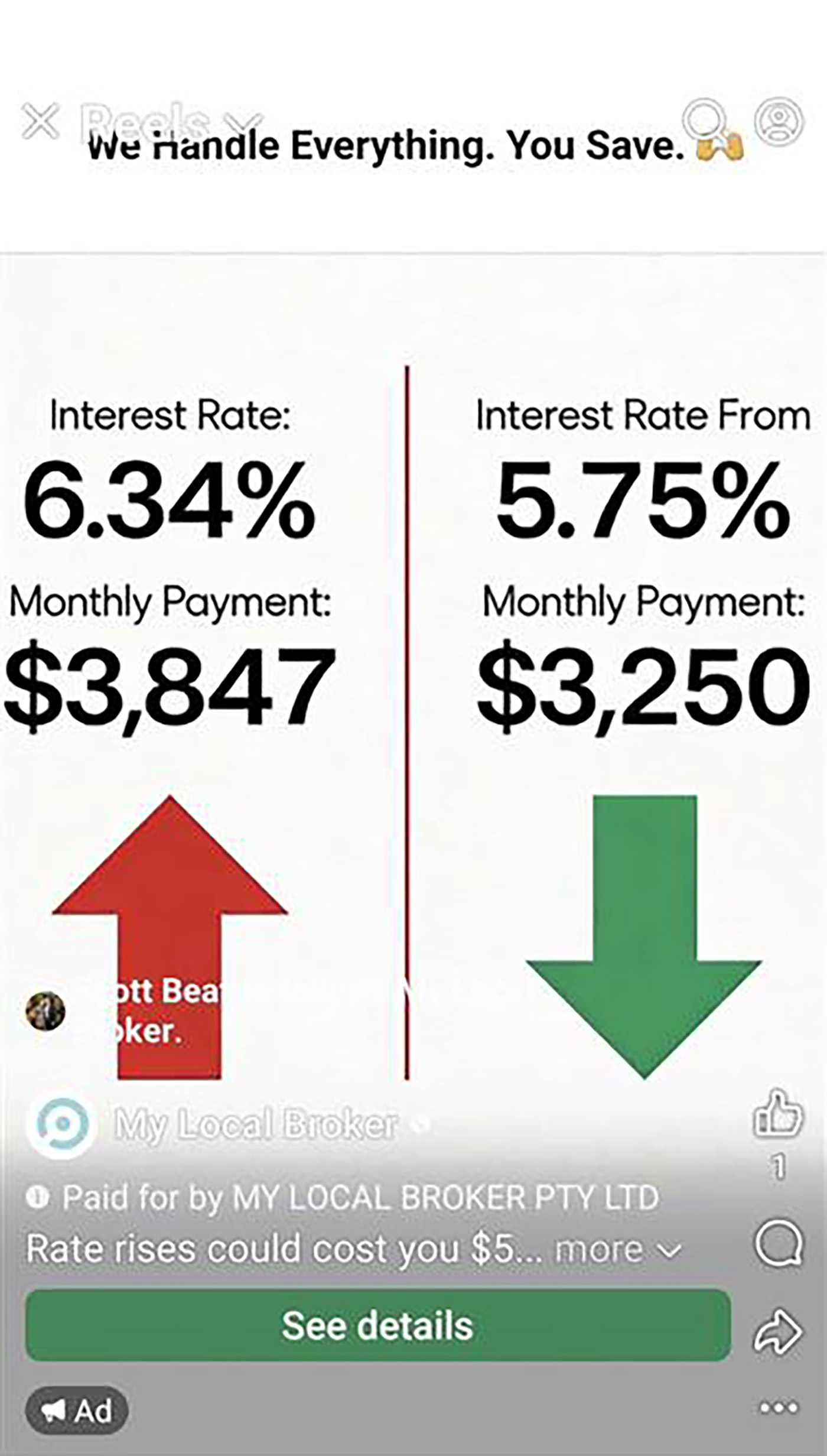

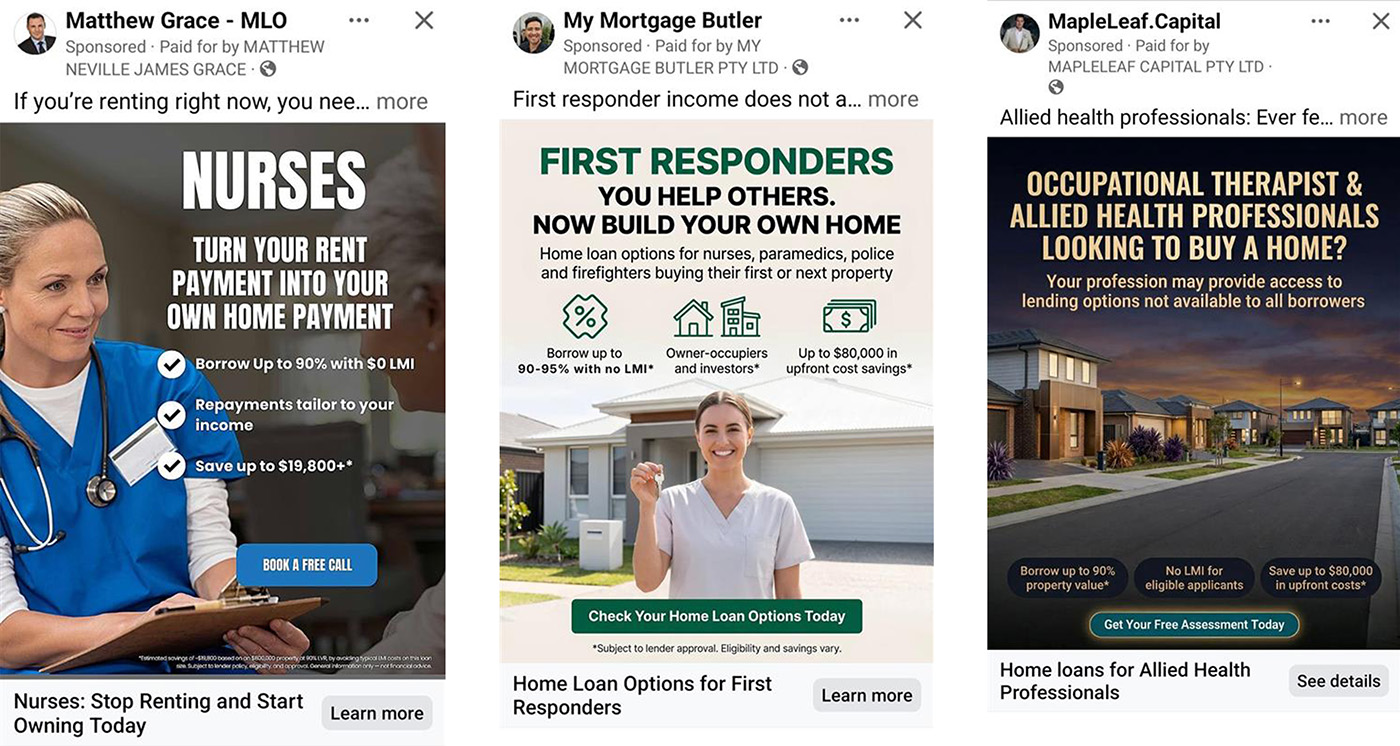

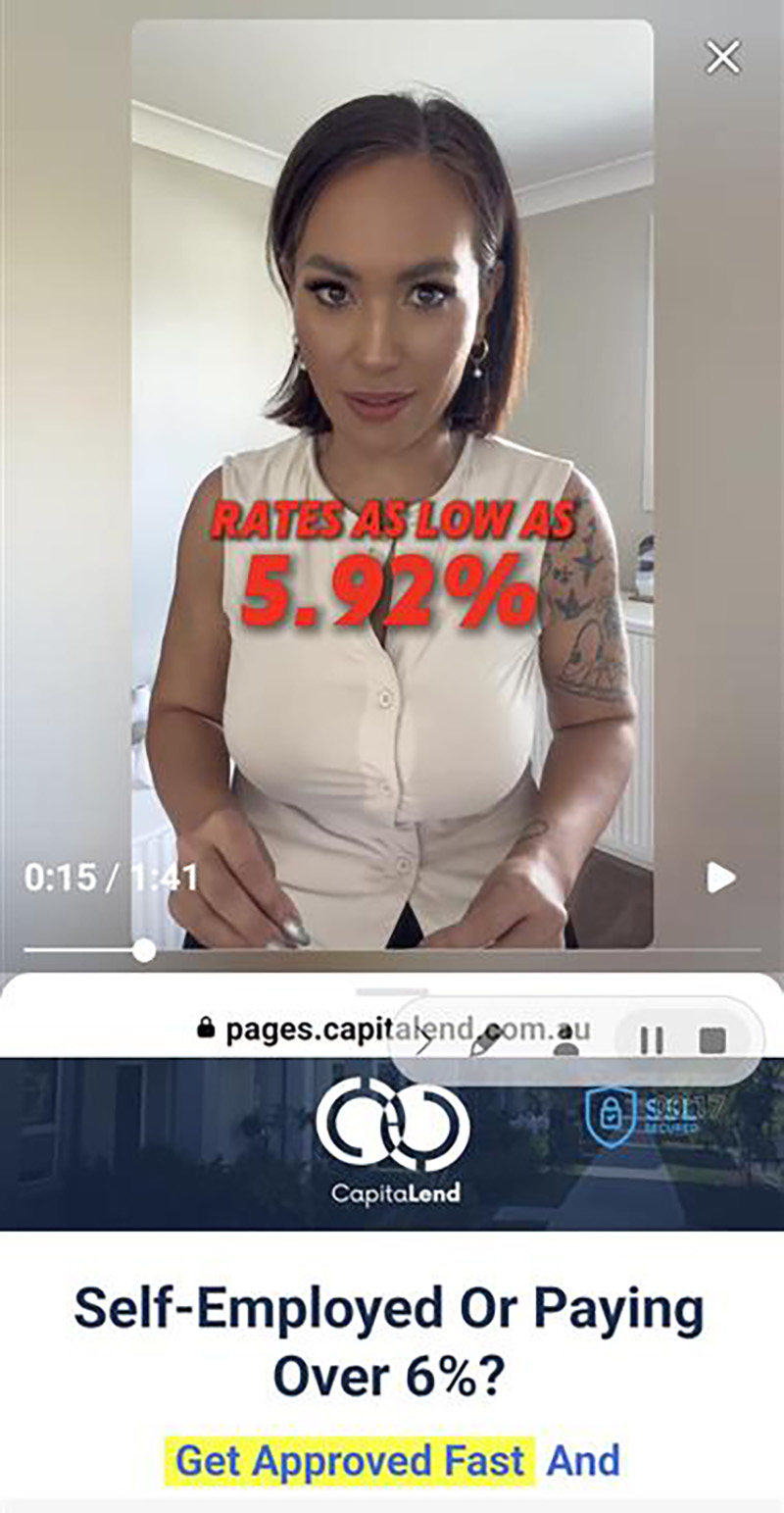

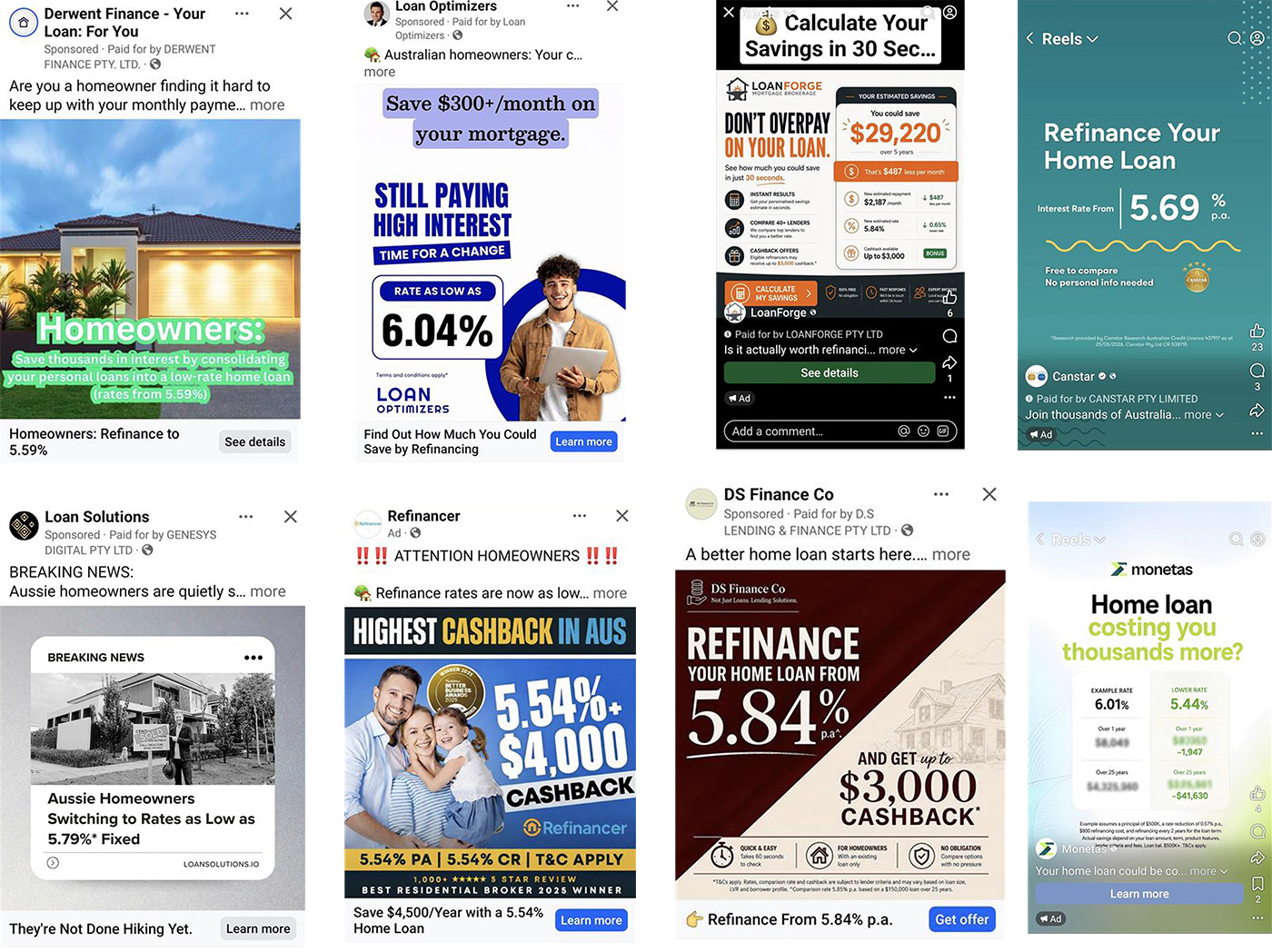

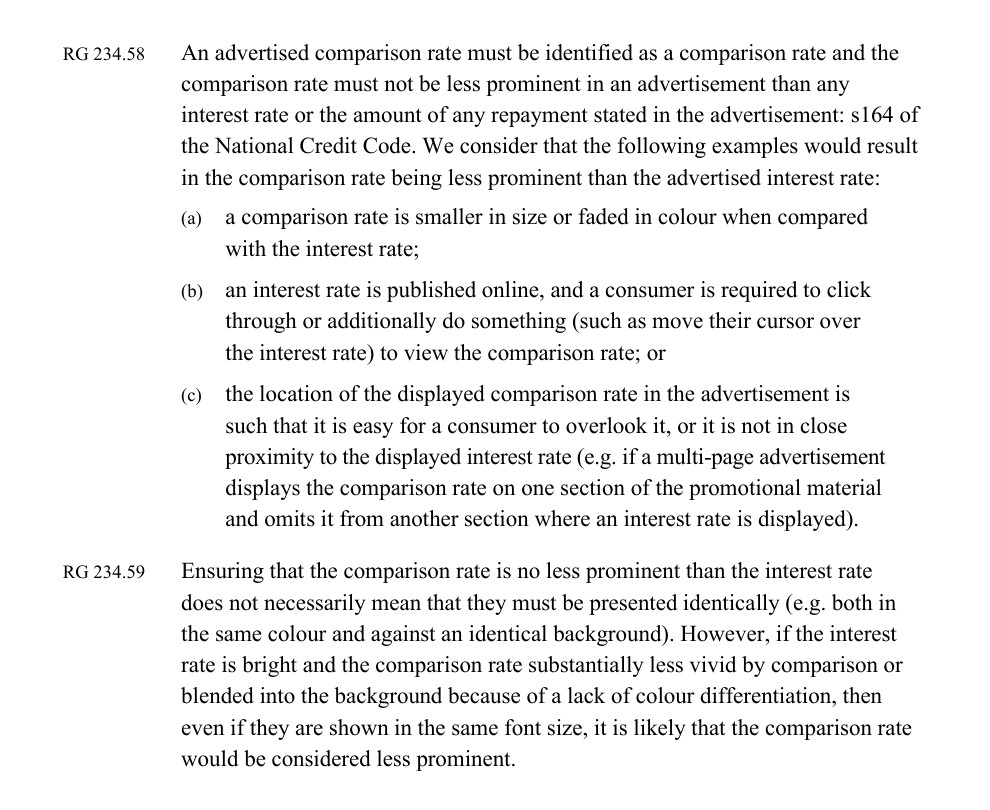

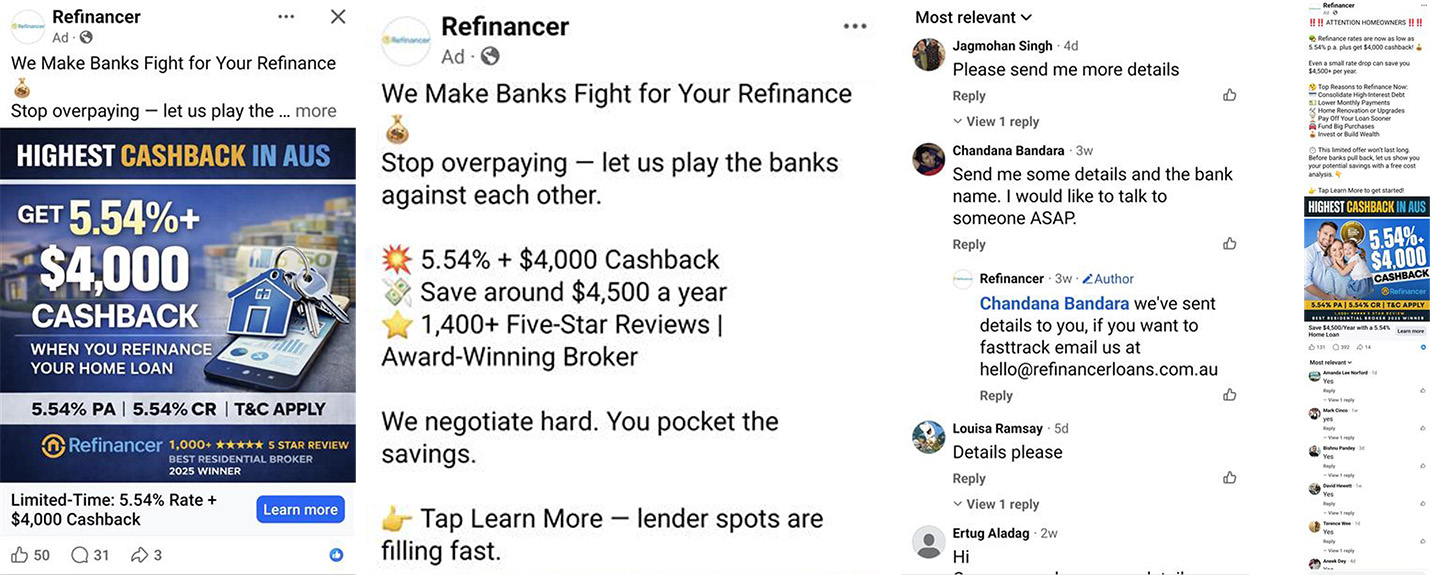

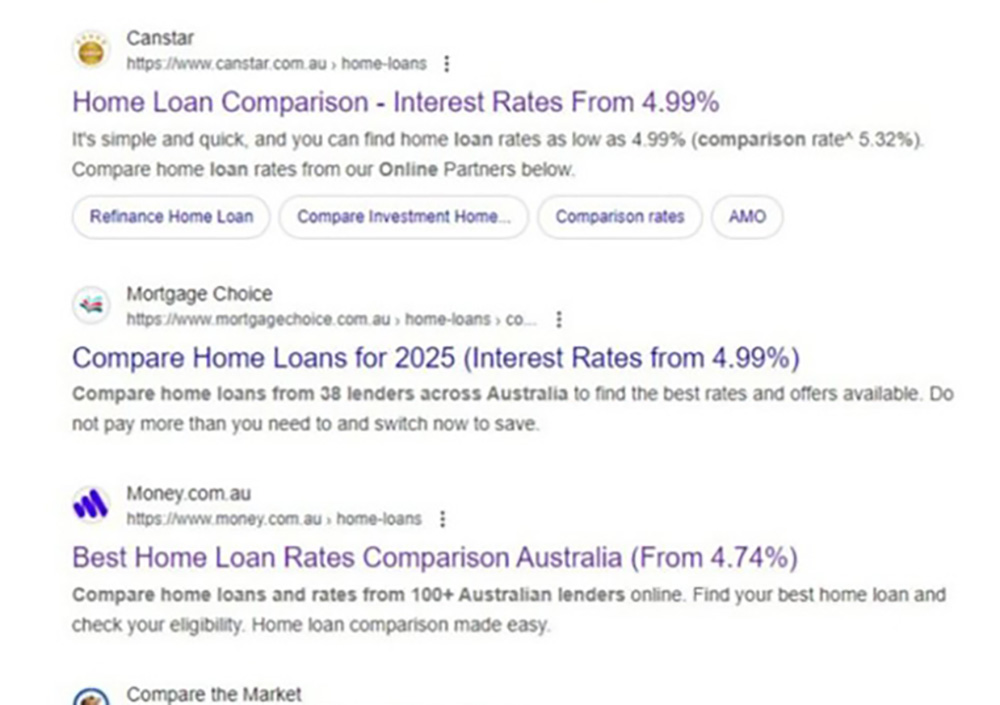

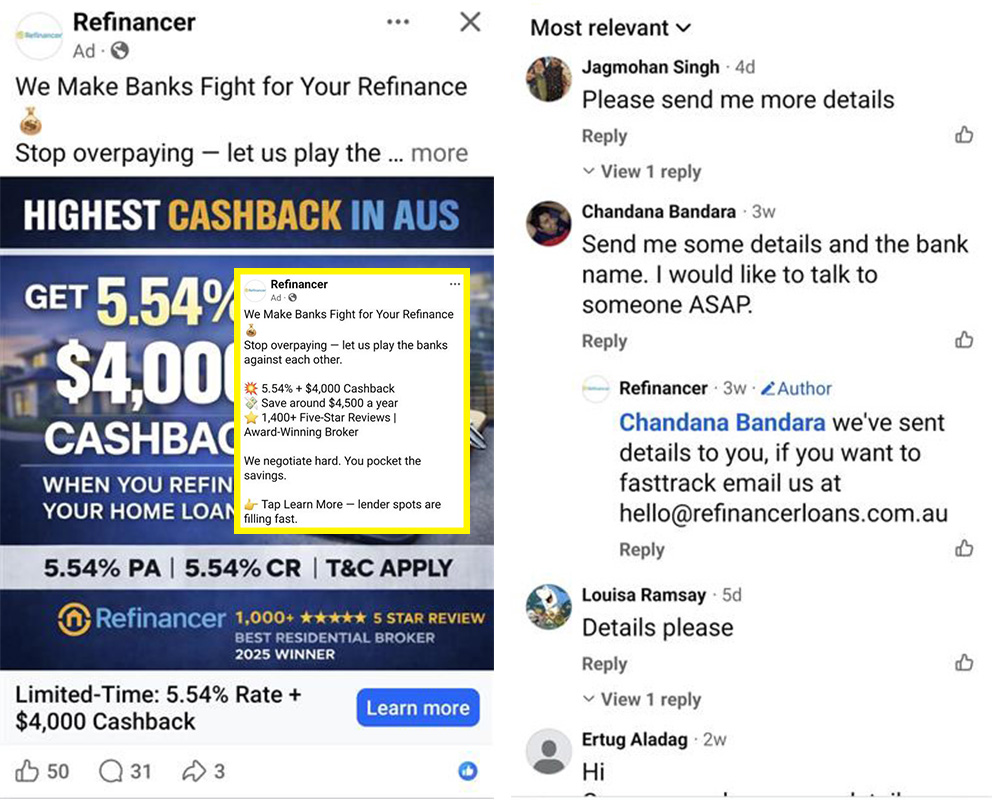

The advertising of mortgage interest rates occupies a unique position within consumer protection law. Unlike most forms of commercial advertising, the promotion of credit products is subject to an unusually prescriptive legislative framework that attempts to reconcile two competing realities. On one hand, consumers require simple and accessible indicators by which to compare competing mortgage products, and on the other, the true cost of credit is inherently multidimensional, incorporating not merely interest charges but also establishment fees, ongoing fees, discharge fees, package costs, offset account structures, redraw conditions, and numerous contingent expenses. The legislative response to this 'rate tension' was the creation of the comparison rate regime under the National Credit Code. The comparison rate was intended to function as a corrective mechanism against the behavioural tendency of consumers to focus exclusively upon headline interest rates. In psychological terms, legislators sought to counteract the cognitive bias known as anchoring, whereby consumers disproportionately weight the first numerical value encountered during decision making. The comparison rate regime therefore attempts to force advertisers to present a more comprehensive measure of borrowing cost alongside the headline rate. Despite the apparent simplicity of the legislative framework, widespread non-compliance remains observable throughout the mortgage broking industry.…

Blog & News

The increasing use of offshore staff, marketing agencies, virtual assistants, appointment setters, and lead-generation companies within the mortgage industry has created a significant and often poorly understood area of regulatory exposure under Australian credit law. This article looks at the legality of the process. Many broker businesses have adopted outsourced customer acquisition structures in which the initial consumer interaction no longer occurs with a licensed broker or authorised credit representative, but instead with a third-party operator whose role is ostensibly administrative or marketing-oriented. While these arrangements are frequently justified as operationally efficient, the legal distinction between administrative support and regulated credit activity is far narrower than many businesses appreciate. The issue is not determined by job title or contractual characterisation, but by the substance of the interaction itself. Once a non-licensed party begins engaging in conduct that influences, assesses, or guides a consumer in relation to a credit product, the conversation may move beyond marketing and into the realm of regulated credit activity under Australian law. The problem? The 'simple' recommendation passed onto a broker based on any early unlicenced assessment is objectively and lawfully viewed as 'advice', so the first conversation is not compliant. The central legislative framework governing…

Blog & News

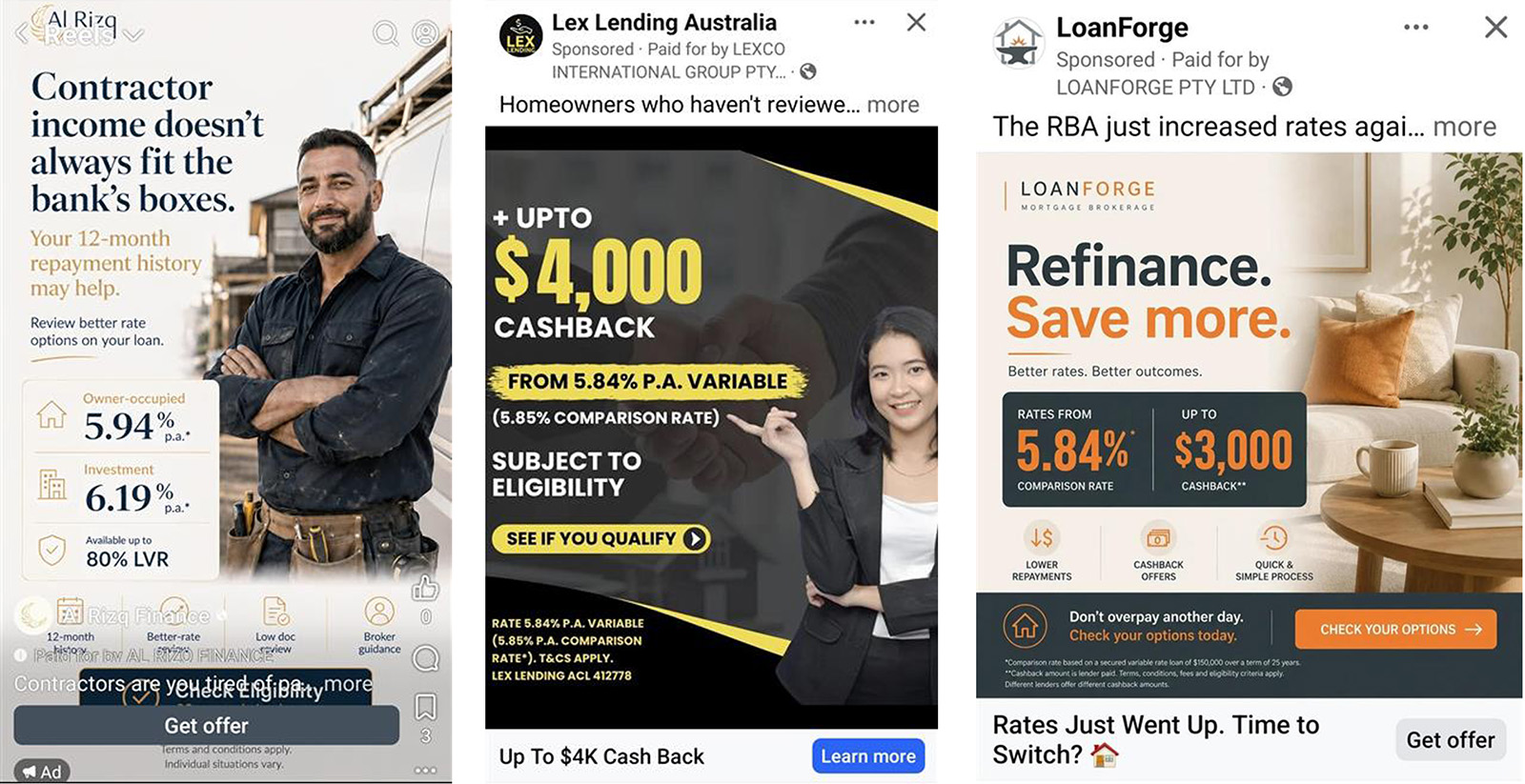

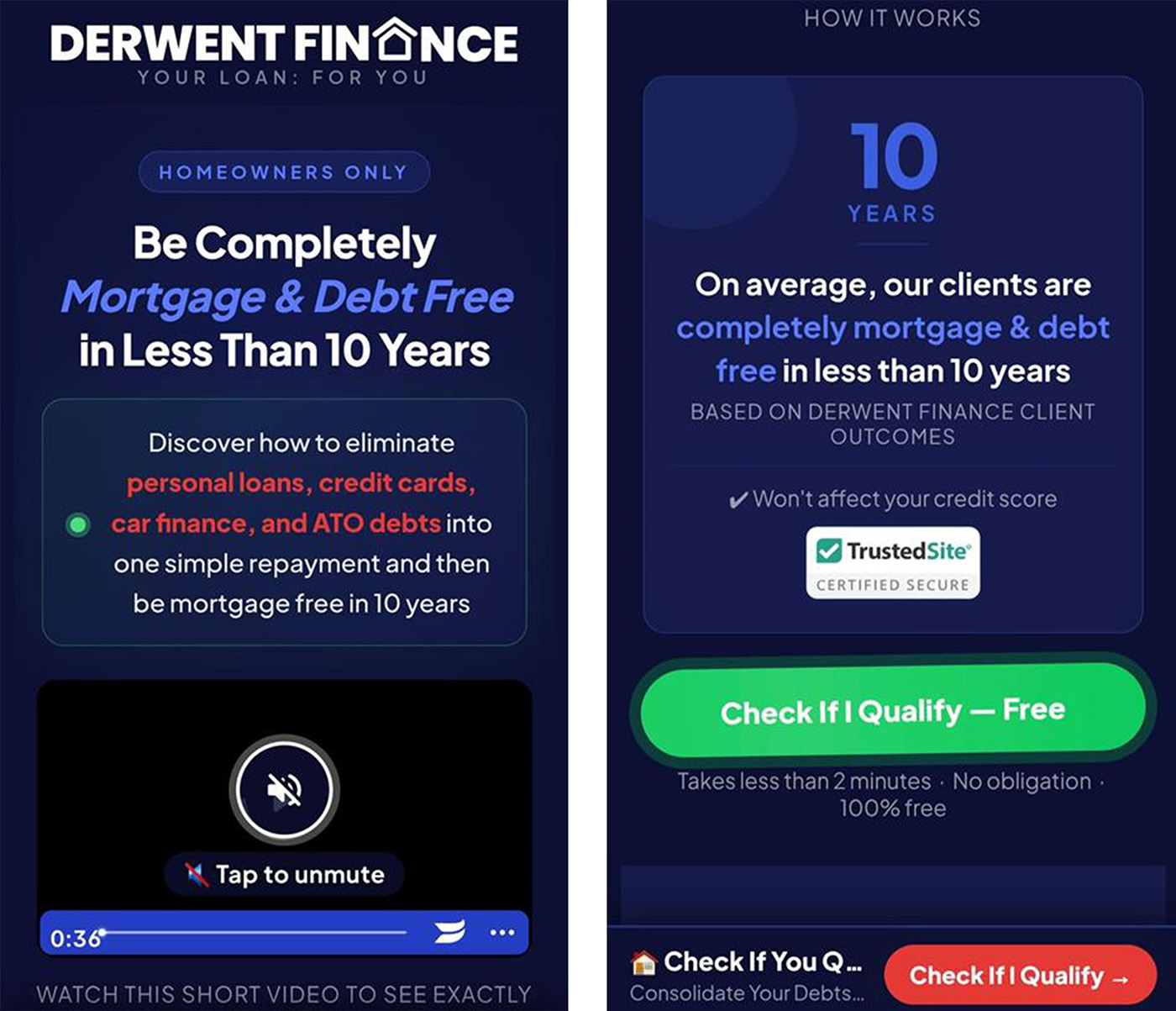

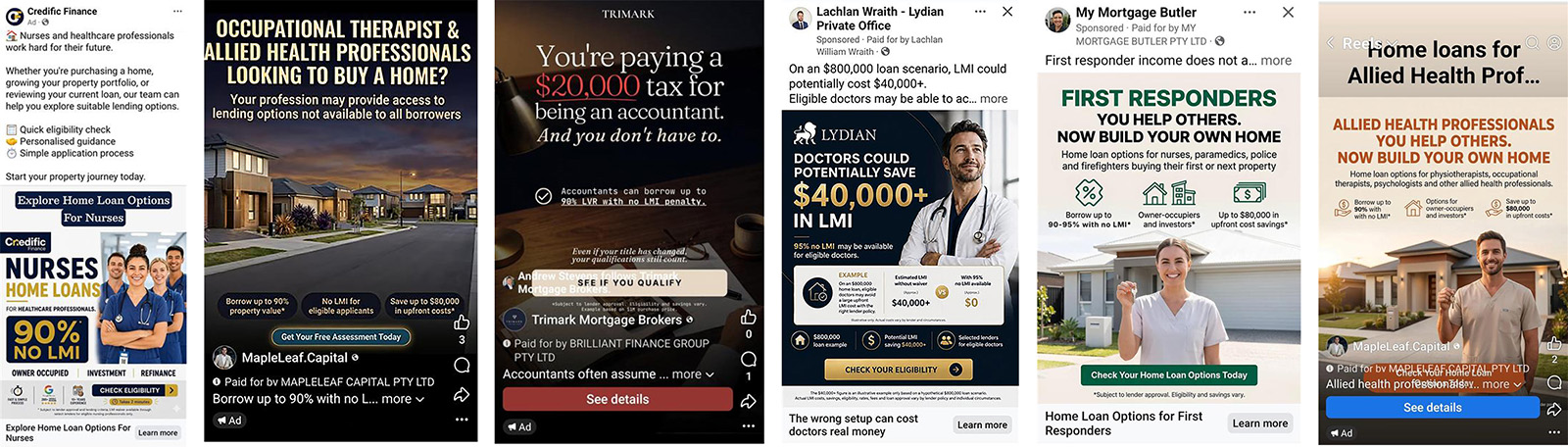

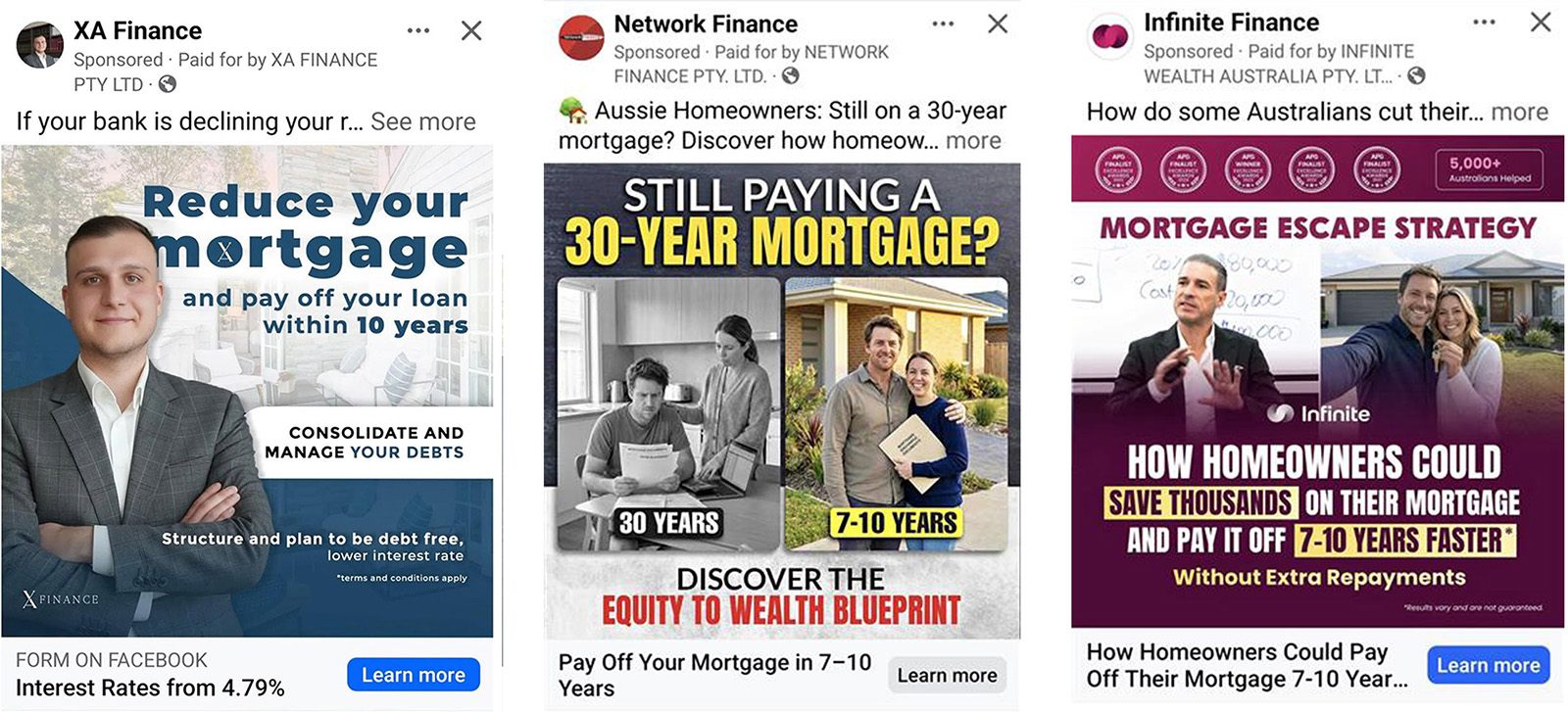

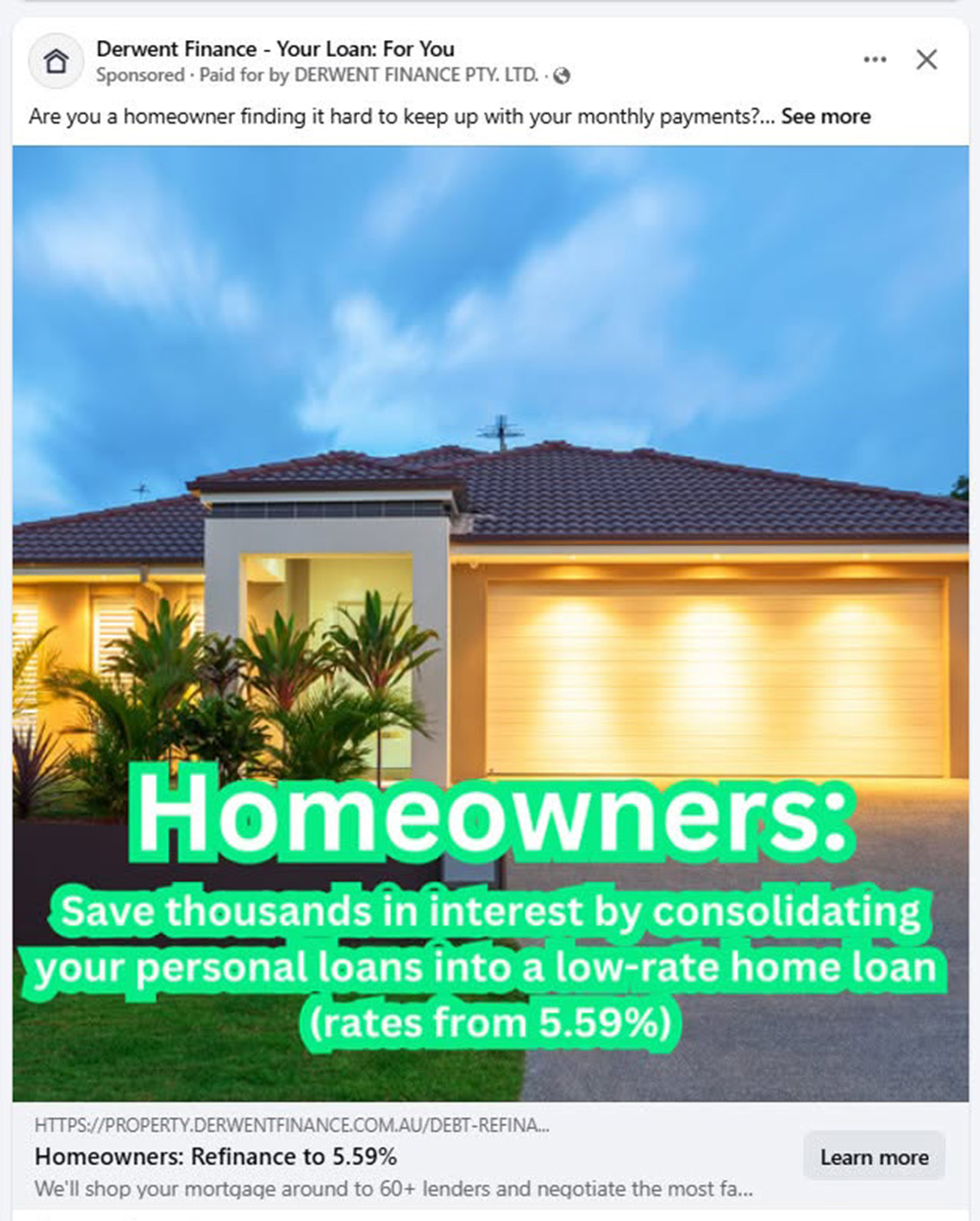

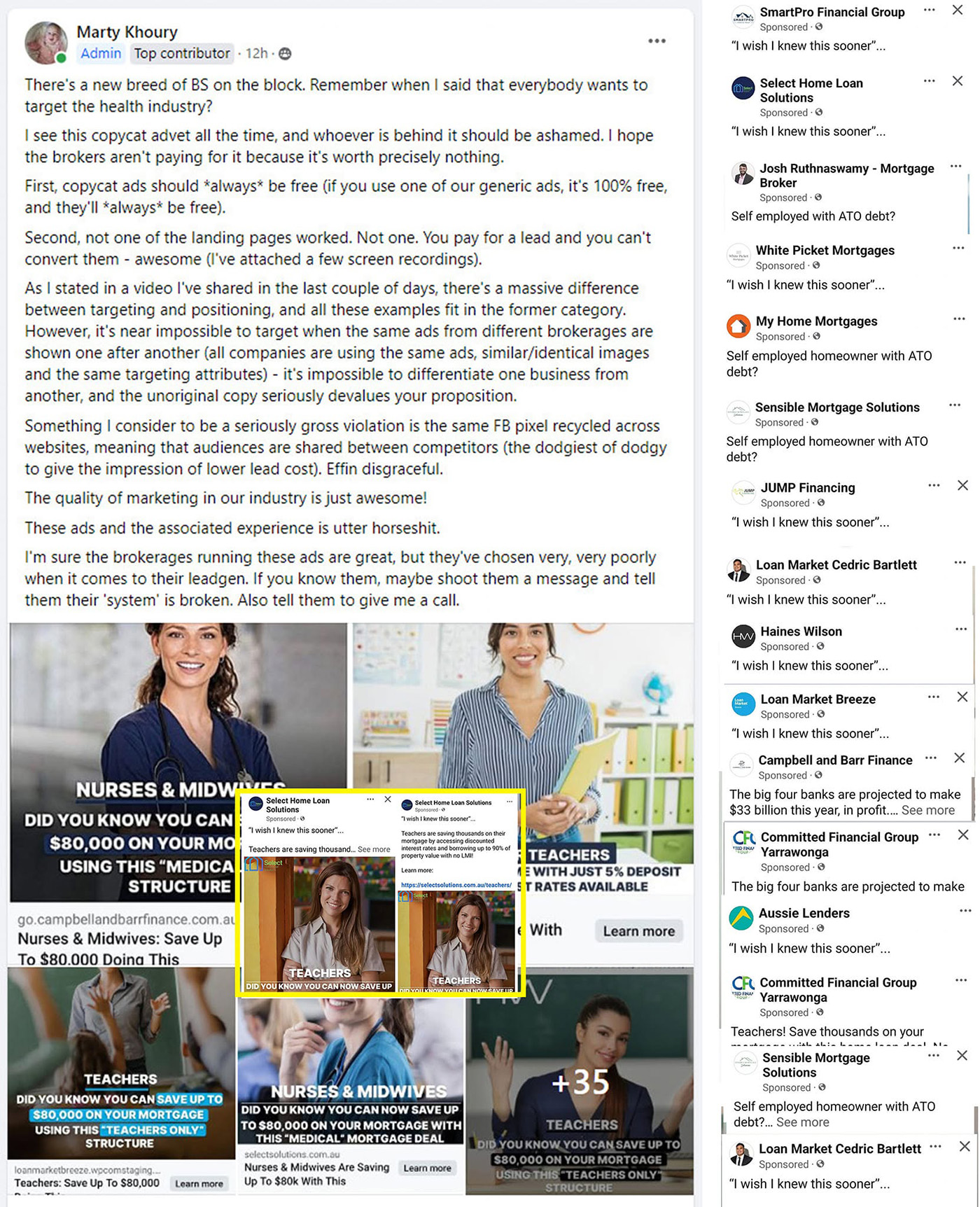

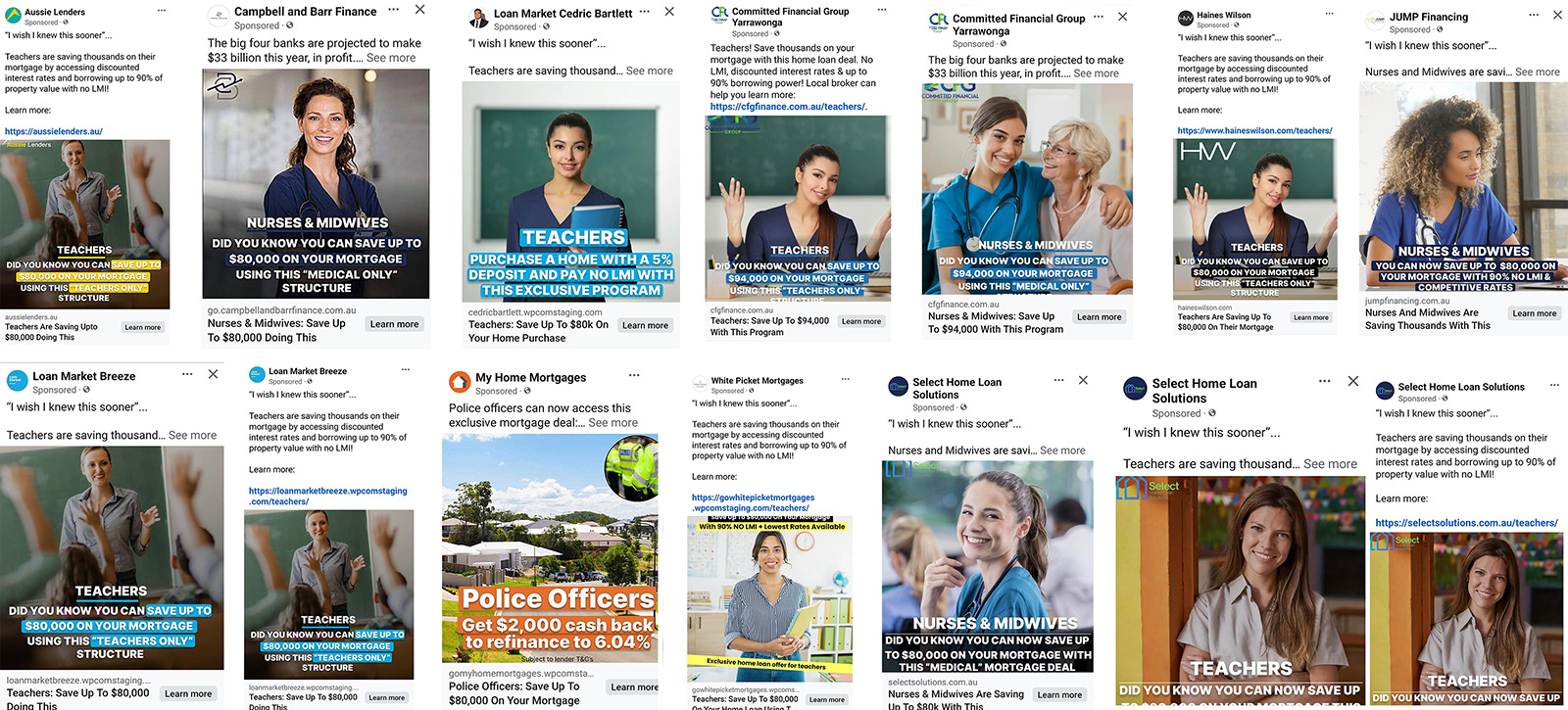

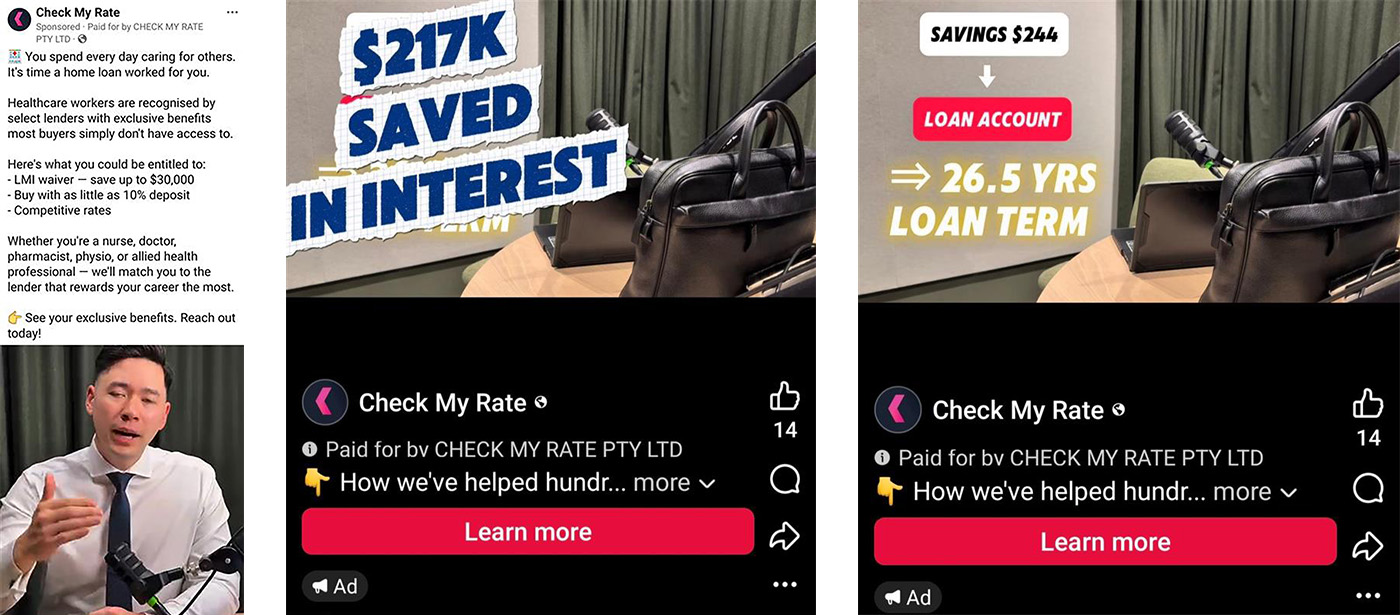

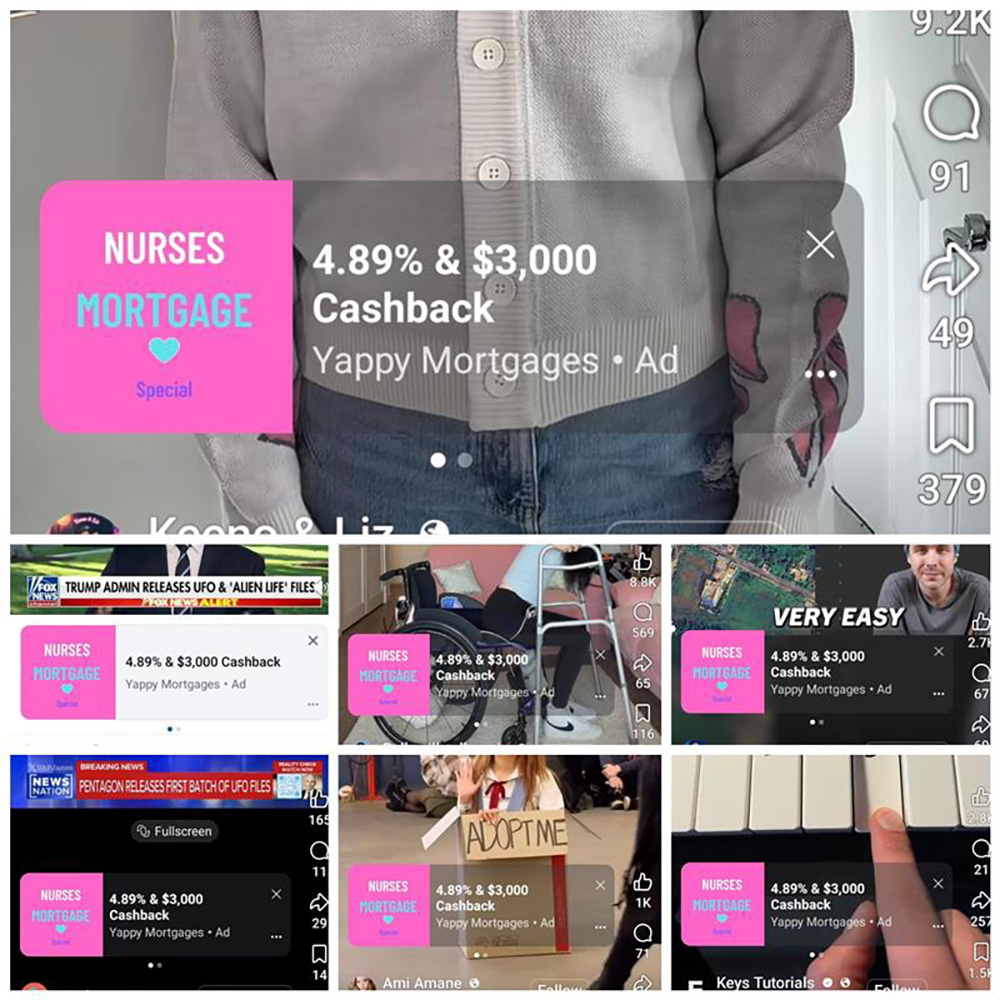

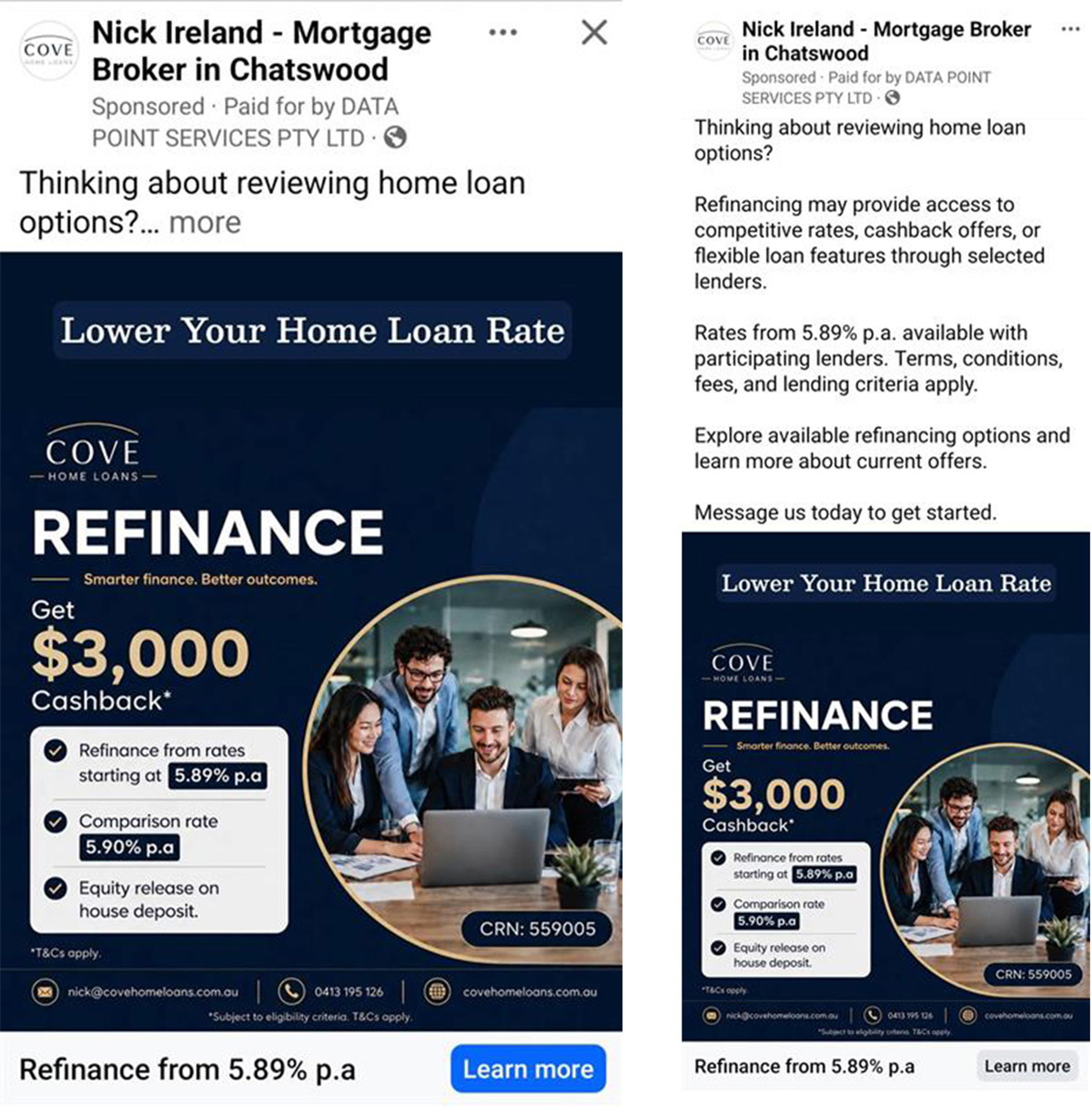

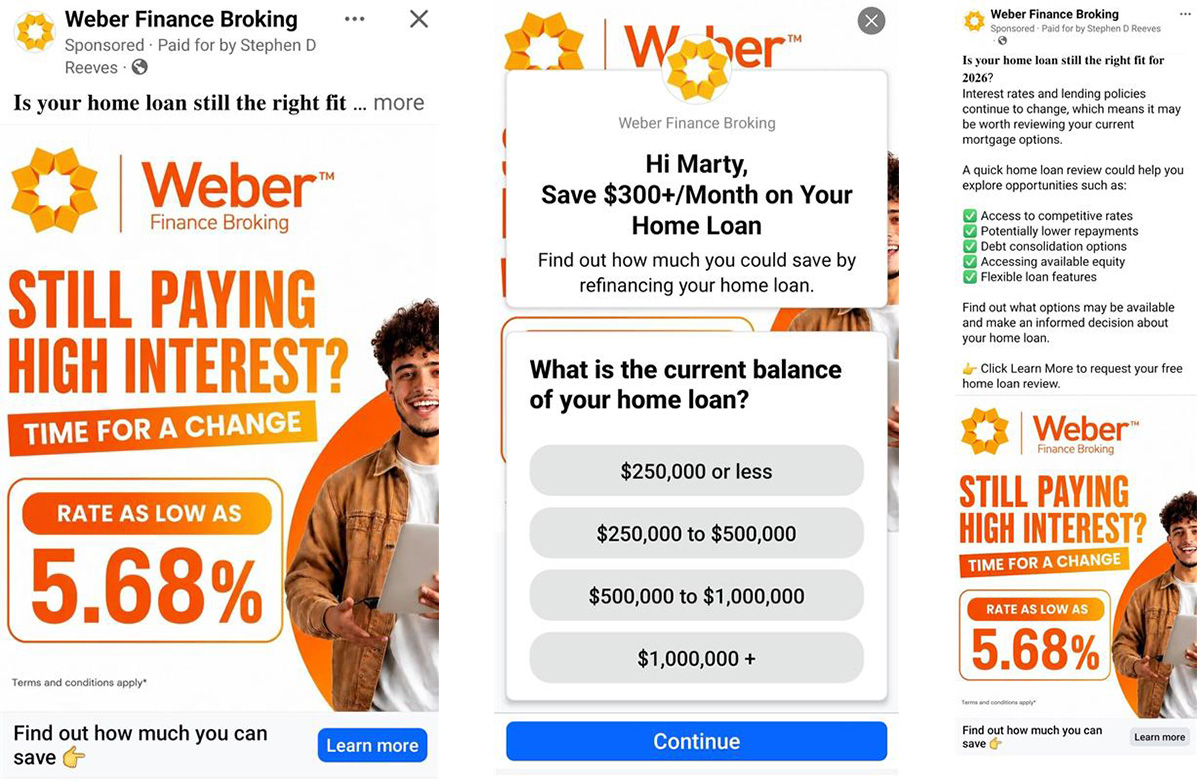

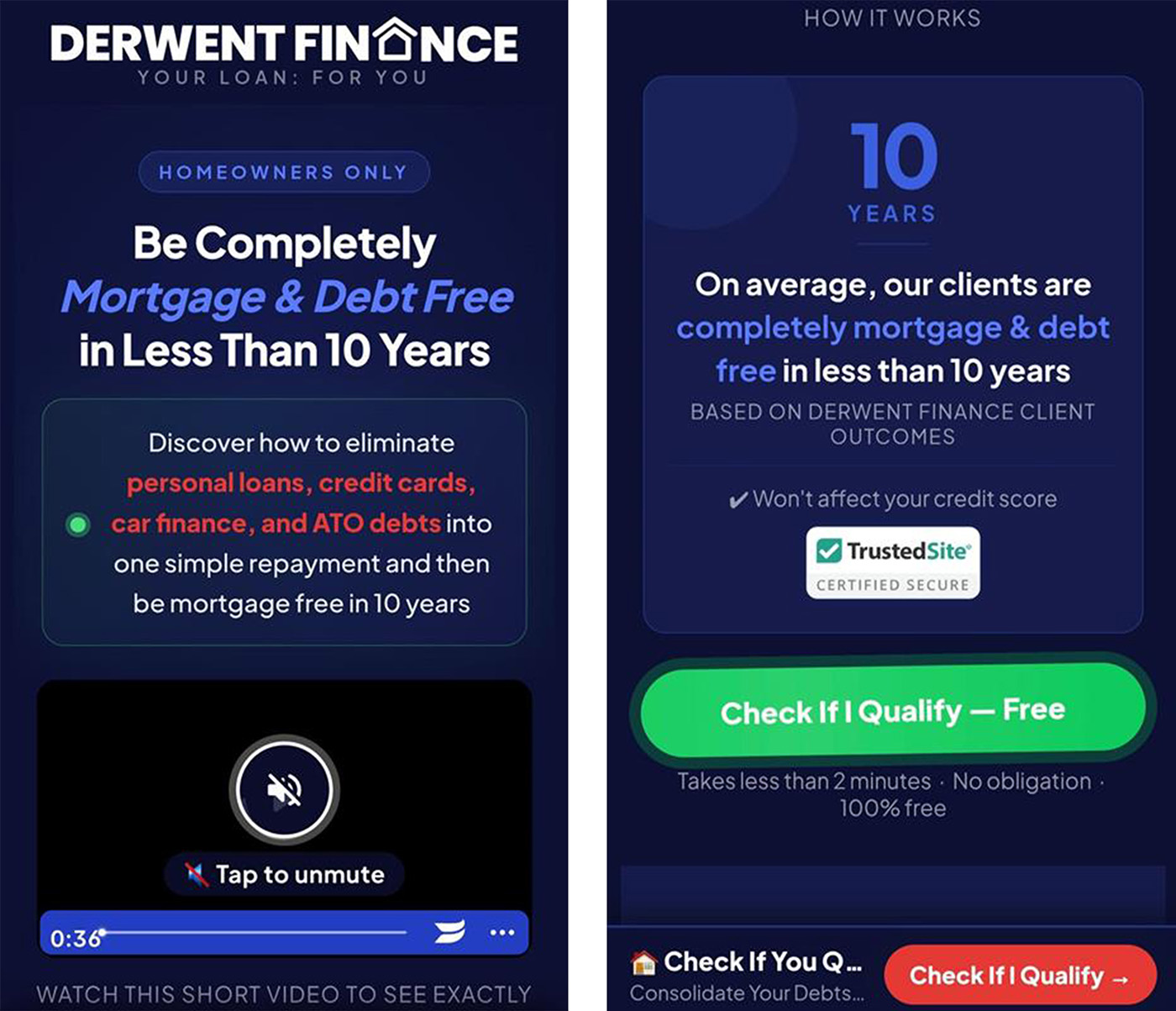

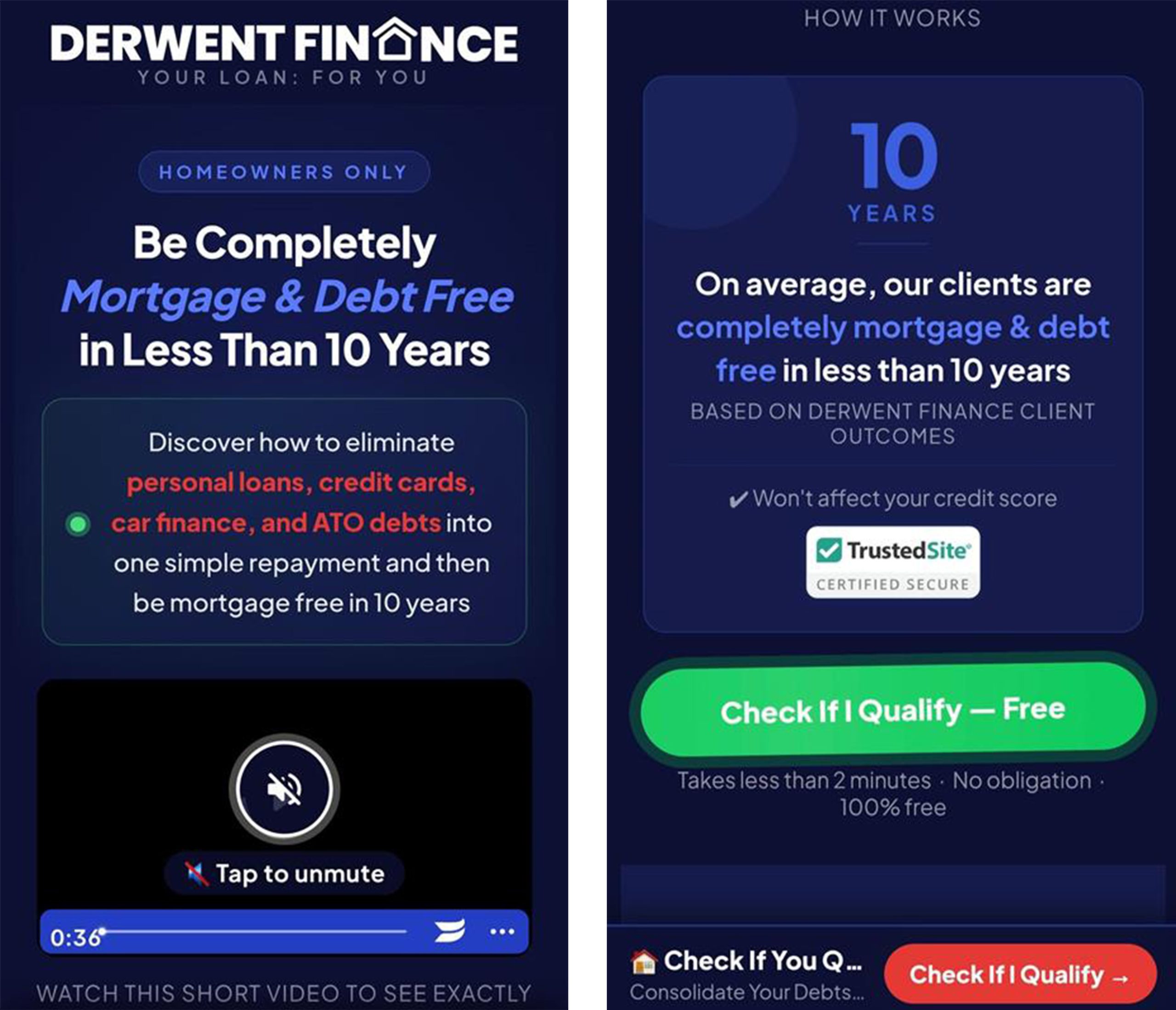

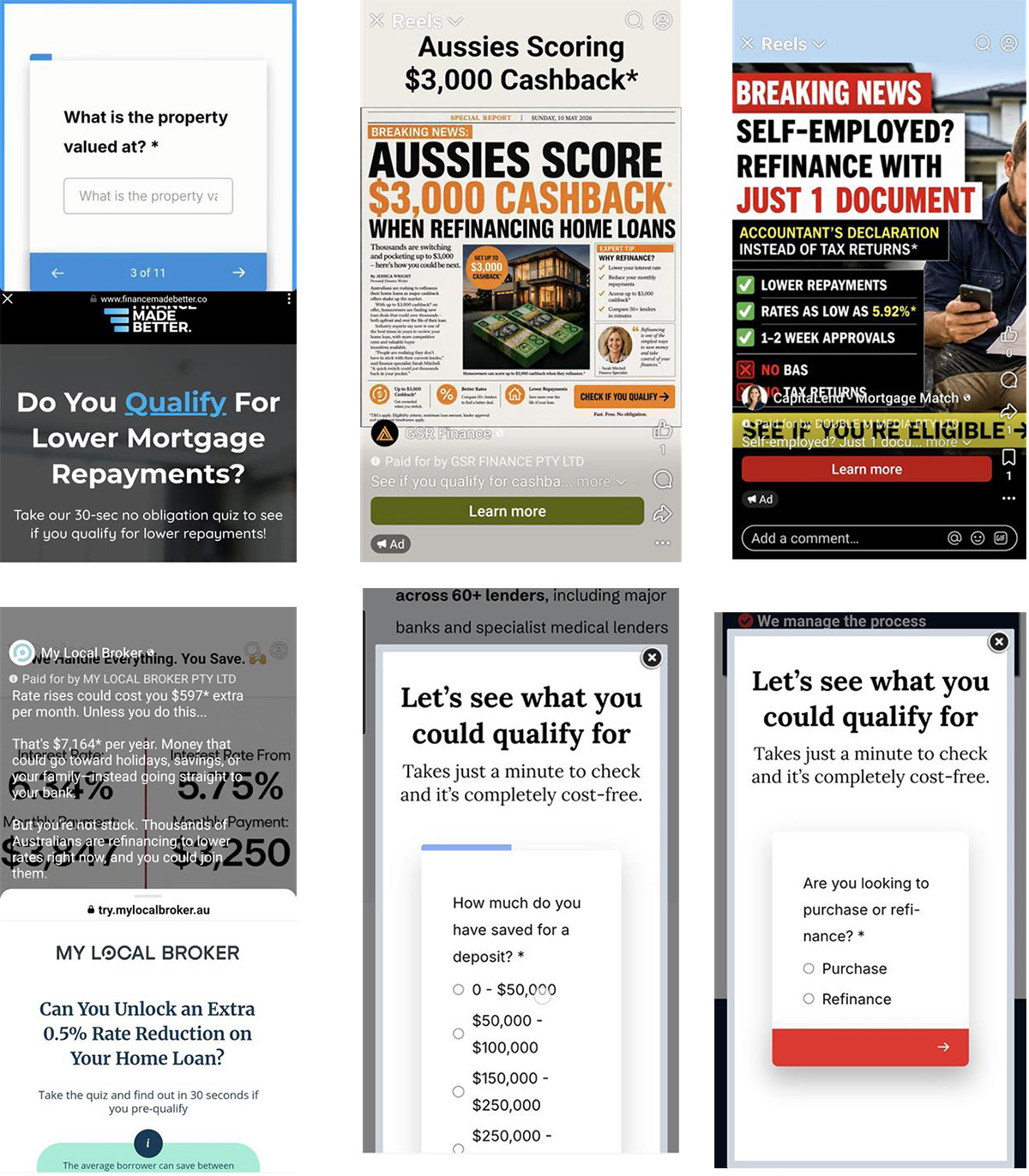

One of the most overlooked requirements in Australian financial advertising is the prohibition on creating a misleading "overall impression" in advertising or during the top-of-funnel subscription experience - even when every individual statement in the ad is technically true... and there's thousands of ads playing out right now that are technically (and usually clearly) illegal. At a time when we're engaged in silent war with lenders and AI, right now is a time when we should be more mindful of the serious consequences of blatantly breaking the law... or even testing legal limits. The problem is that most of the subscription funnels introduced to brokers are deliberately deceptive as a means to improve upon lead flow. While there are clear ways to improve the conversion rate, lying and deception are not two of them. When regulators or prudent aggregators assess your advertising or any consumer-facing assets, they'll consider the dominant message conveyed to an ordinary consumer, not just literal accuracy, and in terms of prosecution, courts will primarily refer to s12DA ASIC Act and ACL s18 to shape the "false and misleading representation provisions" that determine how our advertising is manufactured. It is the misleading representation that is utterly ubiquitous…

Blog & News

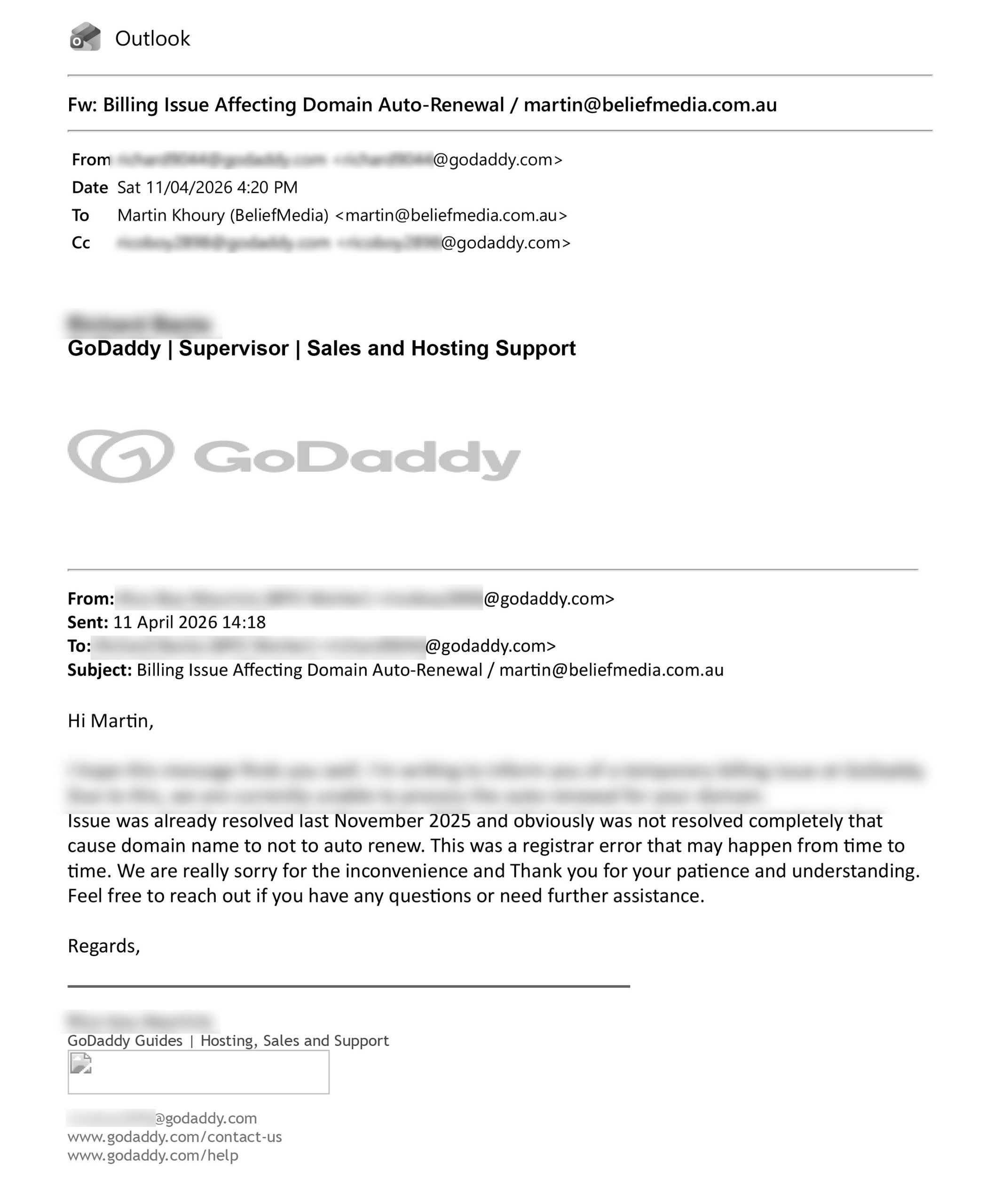

What would you do if you saw somebody drop a wallet in the street? What about if they left a suitcase full of cash on a train? What would you do if you were offered $1000 knowing that the life, business, and family of an individual that isn't known to you would fall apart? More important, what would you do if you registered a domain name through a drop site that was central to the life of somebody, and then kept it knowing it'd cause irreparable and ongoing business and personal damage to that person? I made the critical mistake of trusting GoDaddy with the automatic renewal of my FlightTraining.com.au domain name - a name that I've licenced for nearly three decades, and one that is intimately connected with every aspect of my life. It is my business identify as a Flight Instructor, and the email component especially is connected with the most crucial and private aspects of my life. It was let go in error by GoDaddy (more on this shortly), picked up by a drop site, and registered by Brisbane-based Katie Elizabeth Mathew, somebody that is seemingly most connected to aviation through the private hire of a Cherokee…

Blog & News

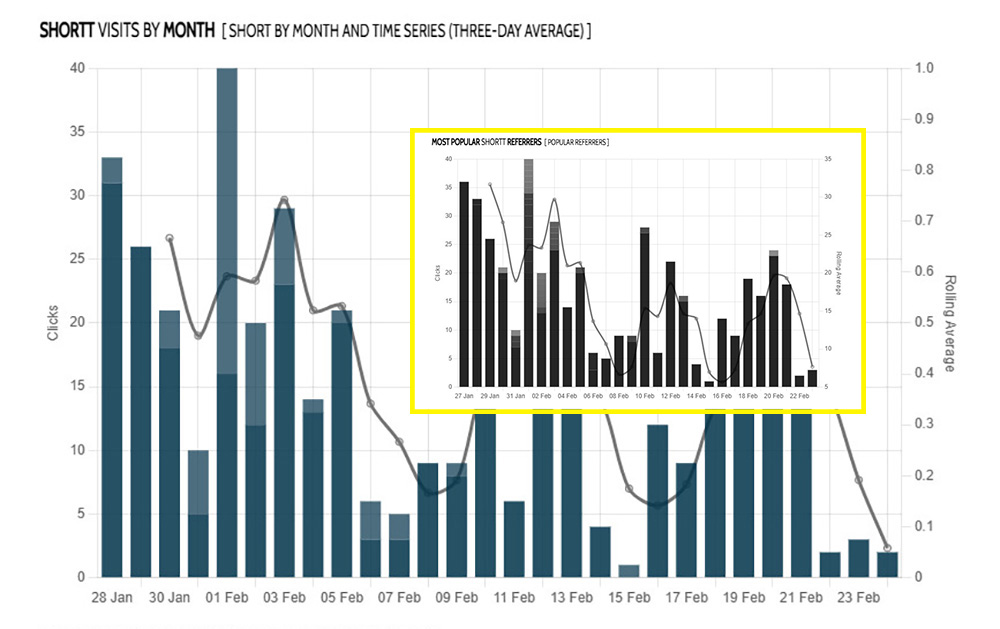

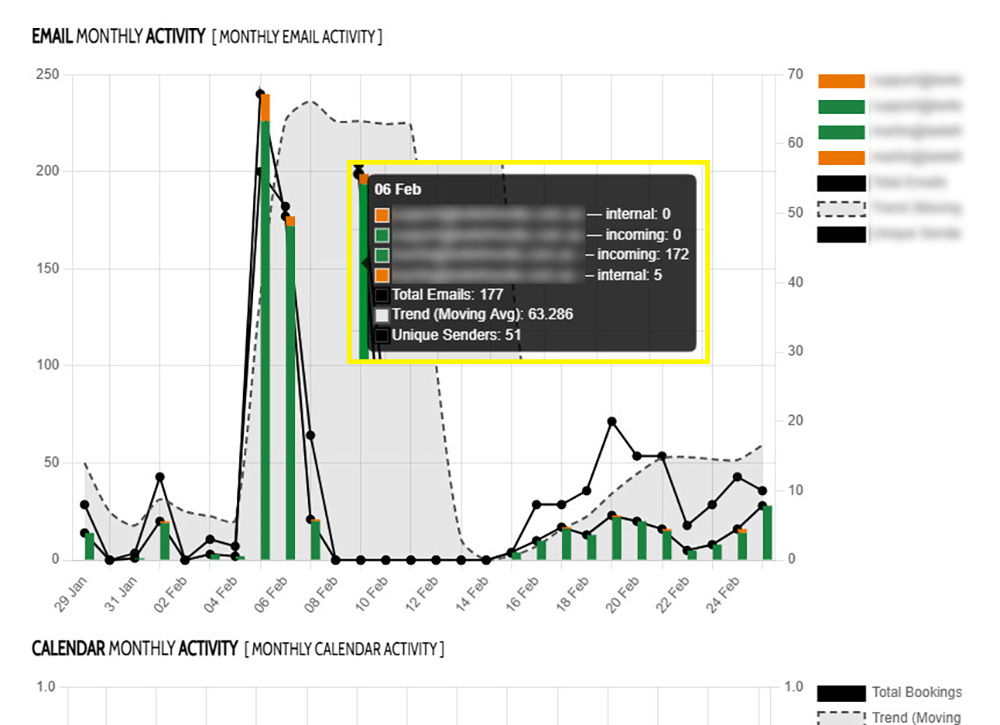

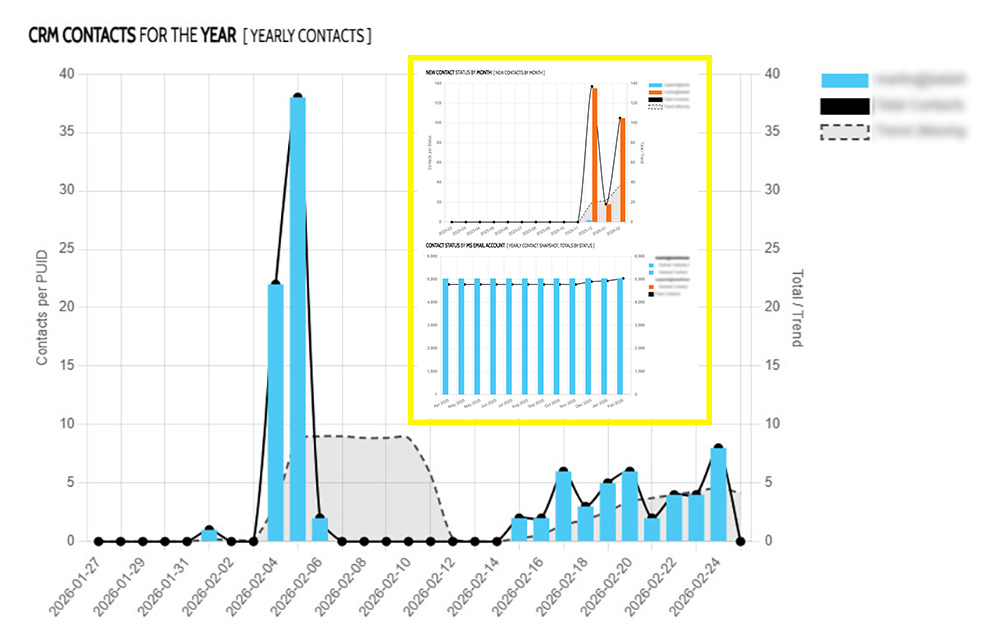

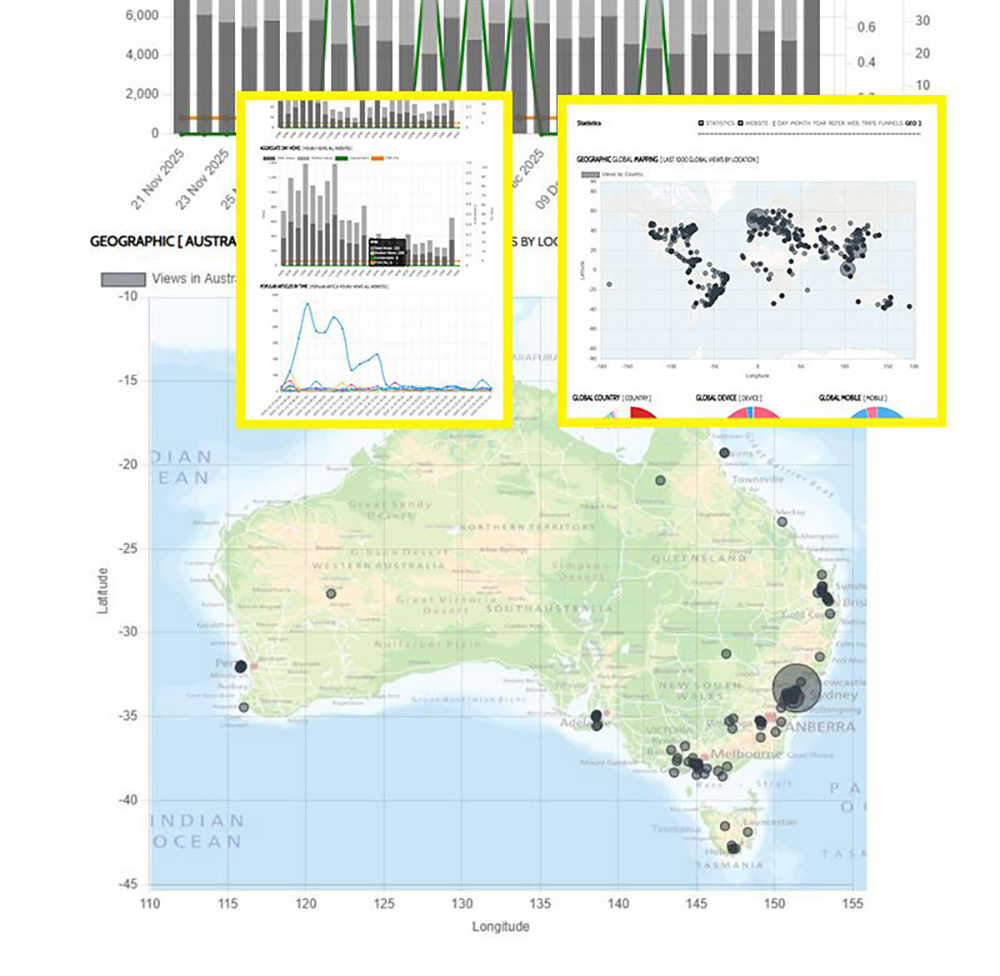

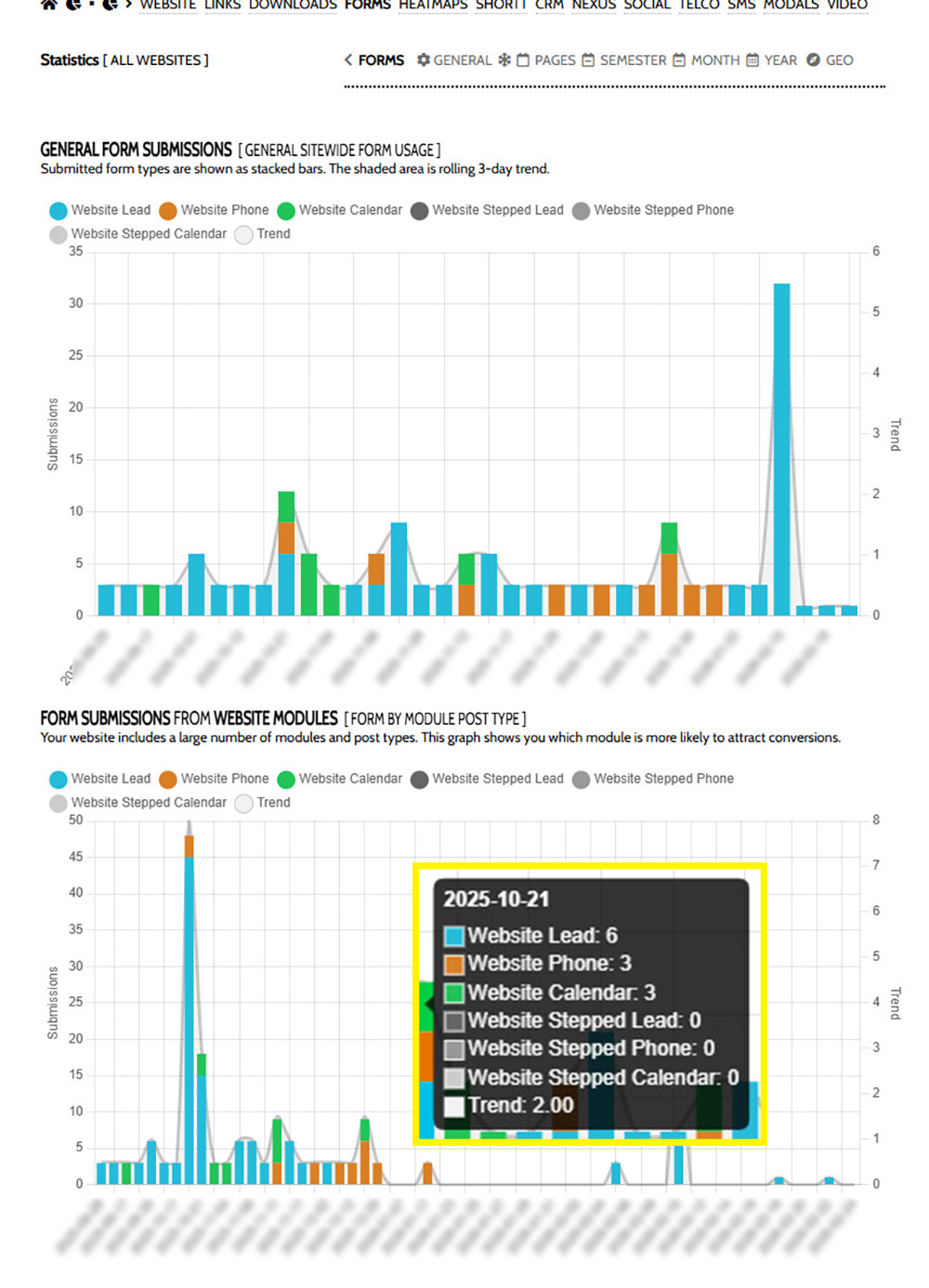

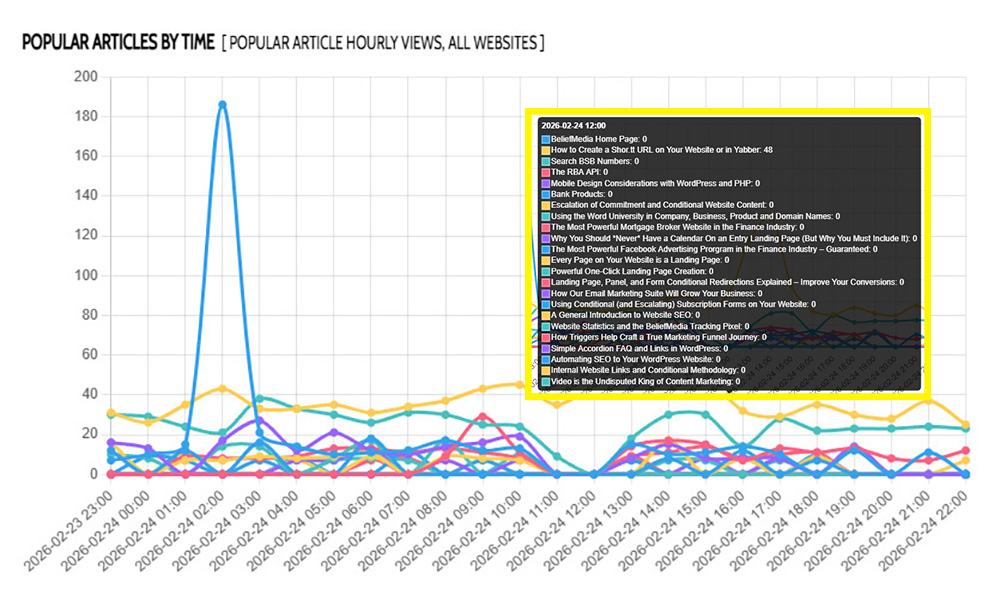

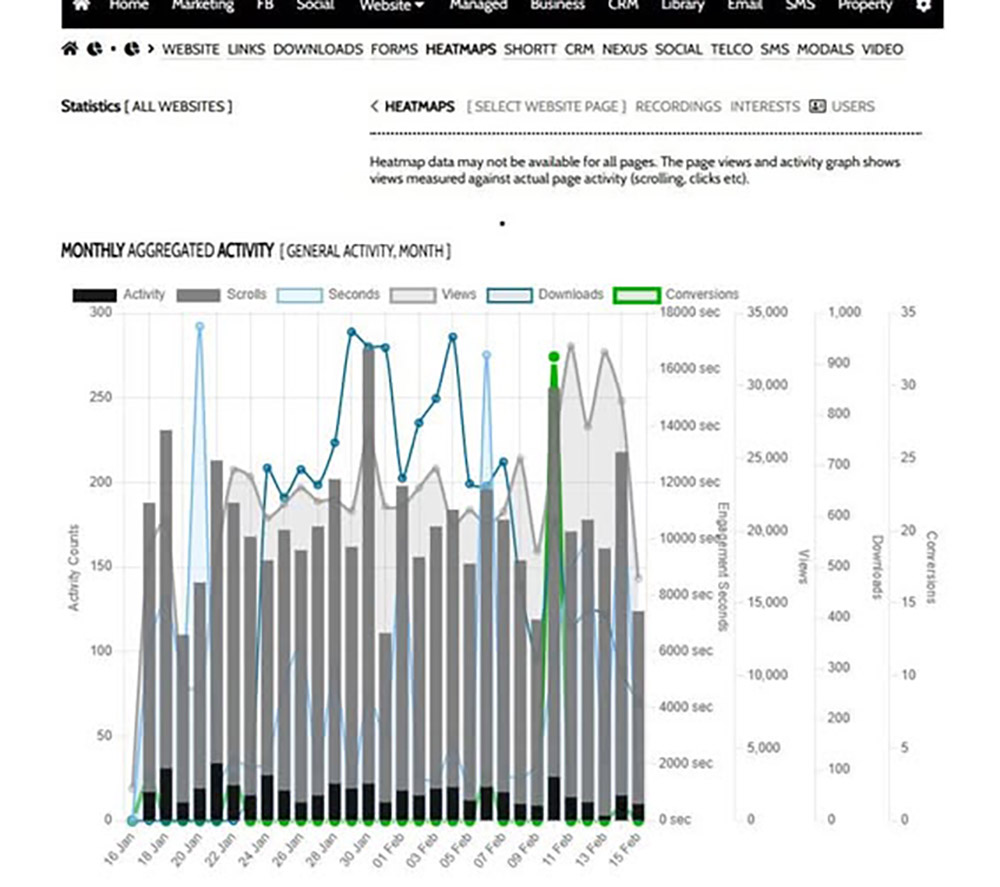

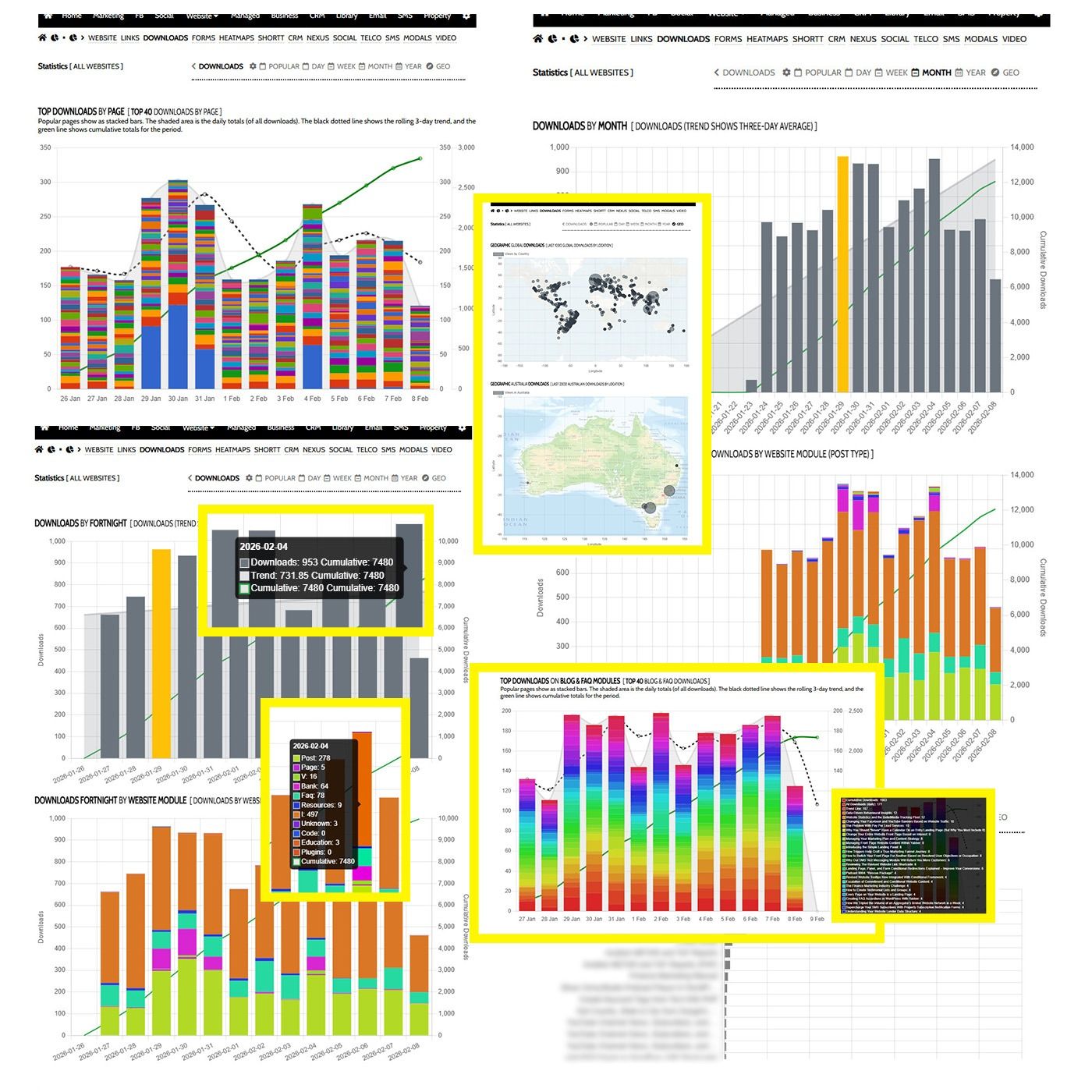

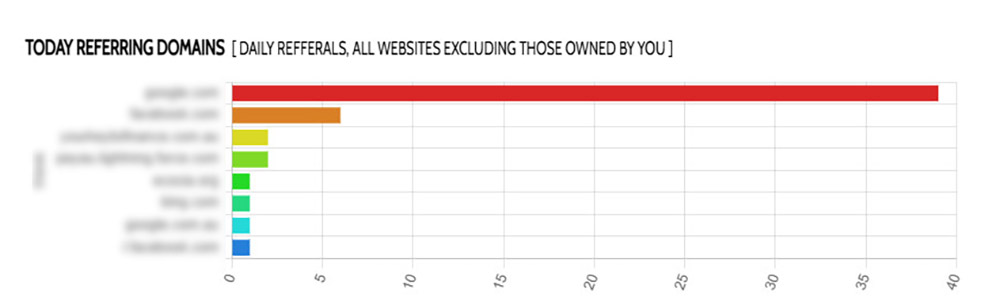

The level of statistical integration availed to those that use Yabber (and our broker website) was always industry leading. However, with over 100 modules that feed statistical data into our conditional engine, the system started to become fragmented, and with a massive focus on 'behavioural analytics', we determined an update was necessary. System growth led us to build a ground-up 'AI-first' statistical engine that was built on the back of several billion data points. We took an axe to the previous system and developed what we call Xena. The massive architectural and AI-supported update (dating back to 2024) finally unifies Yabber modules into a single source, and more seamlessly integrates shor.tt, email marketing (Nexus), CRM, Matrix Insights, property listings, lender data, social media, VoiP logs, CRM actions, landing pages, campaigns, triggers, and Microsoft tools, and we've finally migrated heatmap, scroll, and screen recording functionality that was once the domain of those engaged in paid promotion. The latter functionality alone would normally cost hundreds per month, but it's now part of the default stats engine. If your read no further, understand that we provide statistical insights that exceed the capability of any competing solution by a magnitude that makes other options…

Blog & News

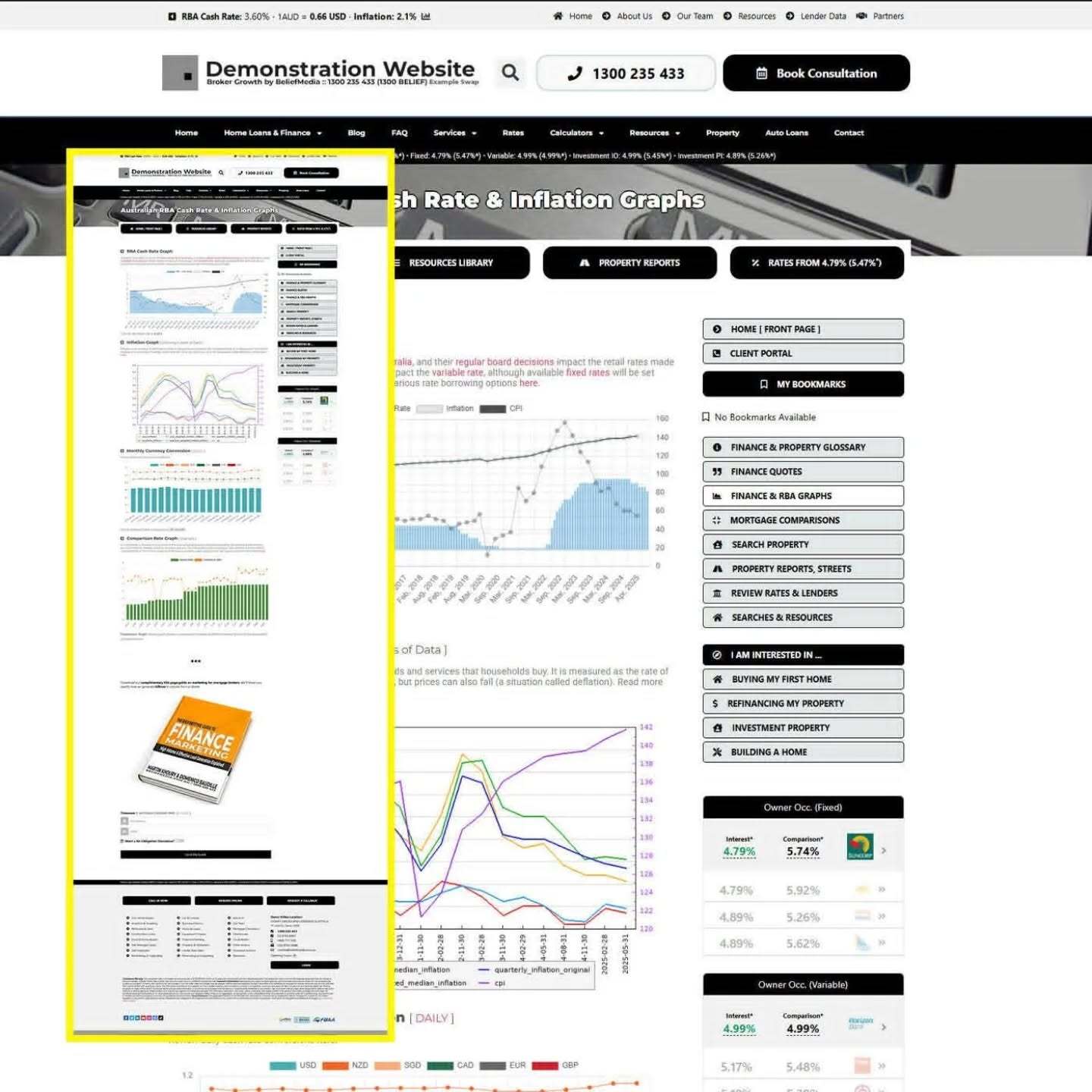

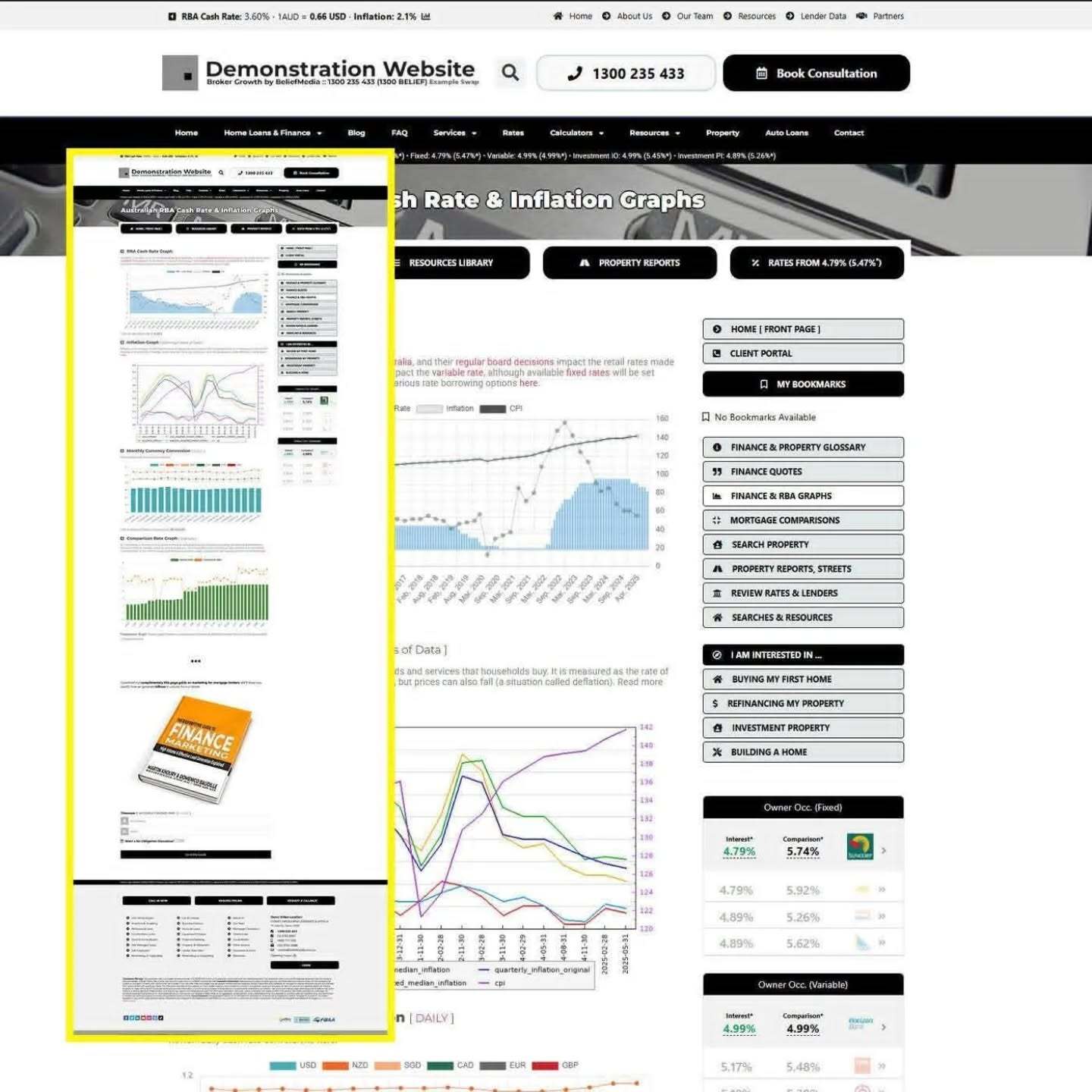

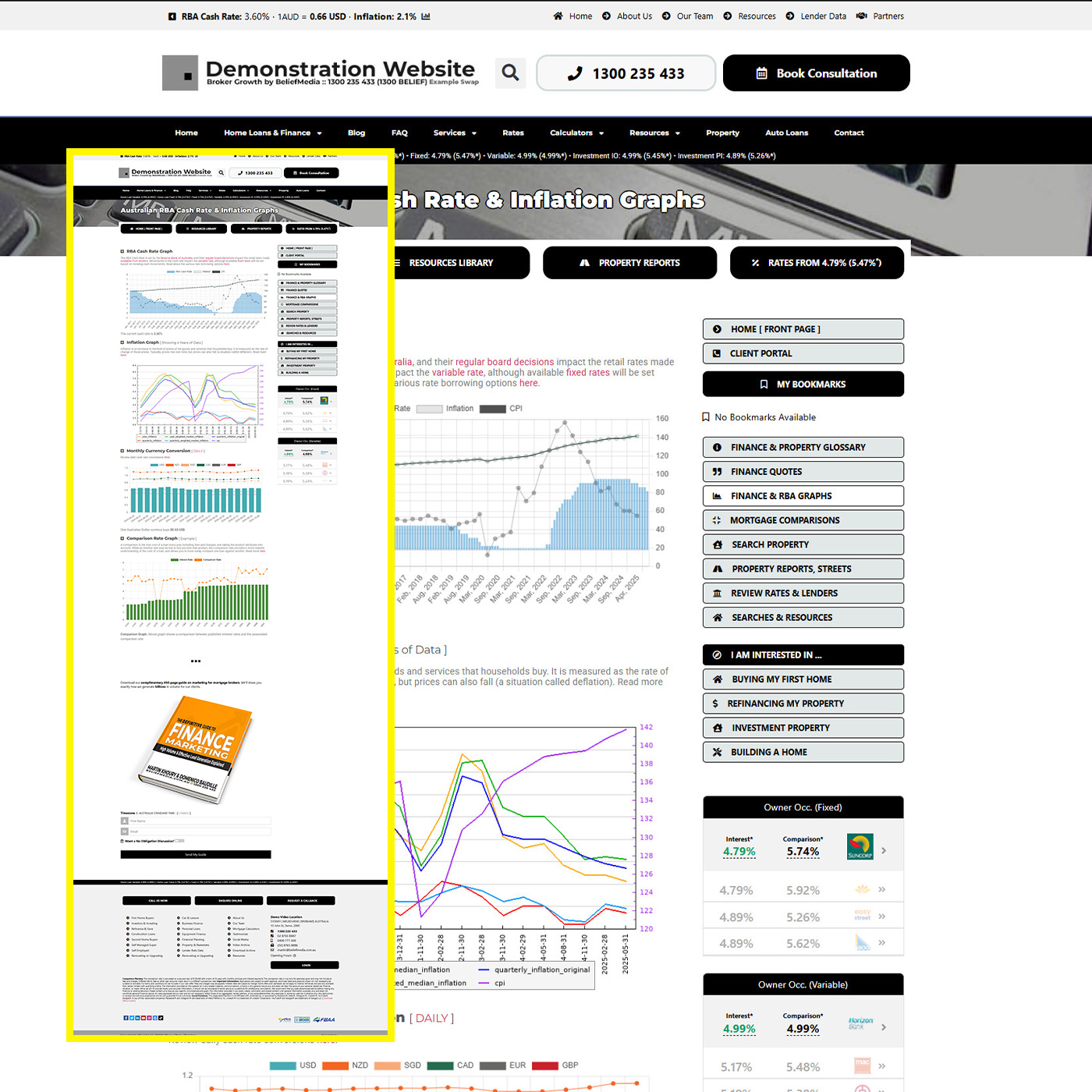

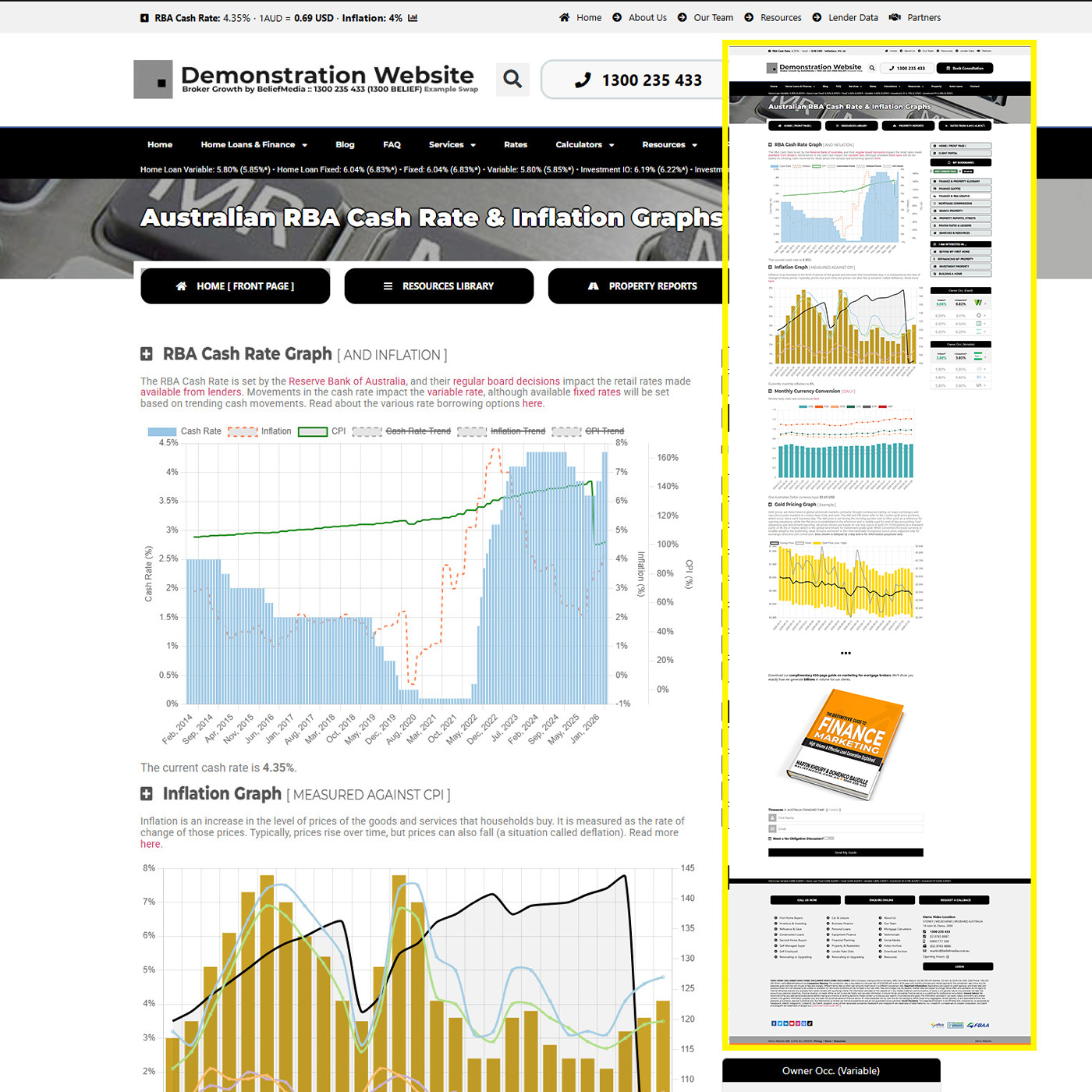

The Reserve Bank of Australia (RBA) publishes large amounts of data to its website as Excel Spreadsheets, but this method makes advanced queries and analytics difficult to query. For this reason, we synchronise our own systems with every available RBA data source, and we've built an API that return insightful information on current and historical trends that are suitable for graphing and broad reporting or analysis. The API itself was built several years ago, while the direct integration to our Comparison, Lender, Metals, Census, and Stock API made in mid 2025. The API is available to all clients by virtue of their personal API Key, and given the licencing of RBA data, keys are generally issued to anybody that requires access. Accessing Reserve Bank of Australia data is straightforward in theory, but in practice it’s slow, fragmented, and difficult to integrate into real-world analysis. That's why we built our RBA API = the only service of its kind in the industry. It’s a comprehensive suite of tools that lets you pull, process, and analyse RBA data in ways that aren't possible with pedestrian tools. Clients have used the API for years to automate reporting, track lending and household trends, and…

Blog & News

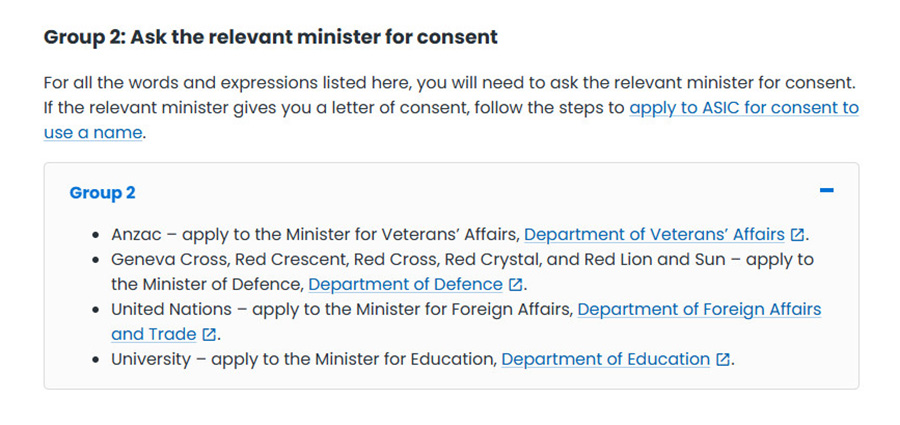

I've noticed a large number of businesses - particularly those in the finance industry - using the term "University" in their business, product, and domain names without understanding that the use is generally prohibited by legislation. Before you embark on any endeavour that purports to provide a university education for general coaching or education programs, or if you simply intend to use the term as part of your broader marketing efforts, ensure that you understand the qualifying requirements, and be prepared to lose any associated domain name if you don't have appropriate authorisation. The term "University" is restricted by ASIC for business names and products as part of their broad and regularly updated "" guidelines, with 'University' listed in the Group 2 bucket, meaning that to use the term in any way you'll have to obtain consent from the education minister. The makes 'university' term use eligibility known to businesses by way of their "Guidelines for the use of the word 'university'" webpage. They state that "[i]ndividuals or groups wishing to use the word ‘university’ in a business, company or domain name must apply for consent from the Minister for Education and Youth, regardless of whether they are offering educational…

The example does illustrate how the slider may be used for alternate post types, and at the moment it supports posts from the following post types: instagram and video posts (intended usage), posts, pages, FAQs, resources, and education. Standalone sliders exist for post types such as testimonials. In the above example, we've applied the 'meta' data which shows icons for images associated with each post, but this is an option we've enabled.

Our shortcode editor will make light work of applying this style of 'complex' markup, but until then, Elementor is far easier to use.

Elementor Widget

As with all our primary tools, a drag-and-drop Elementor Widget is made available that'll allow you to place the slider on any post or page. The widget includes customisation options for virtually every aspect of the slider style. Additional options will be added as they're requested.

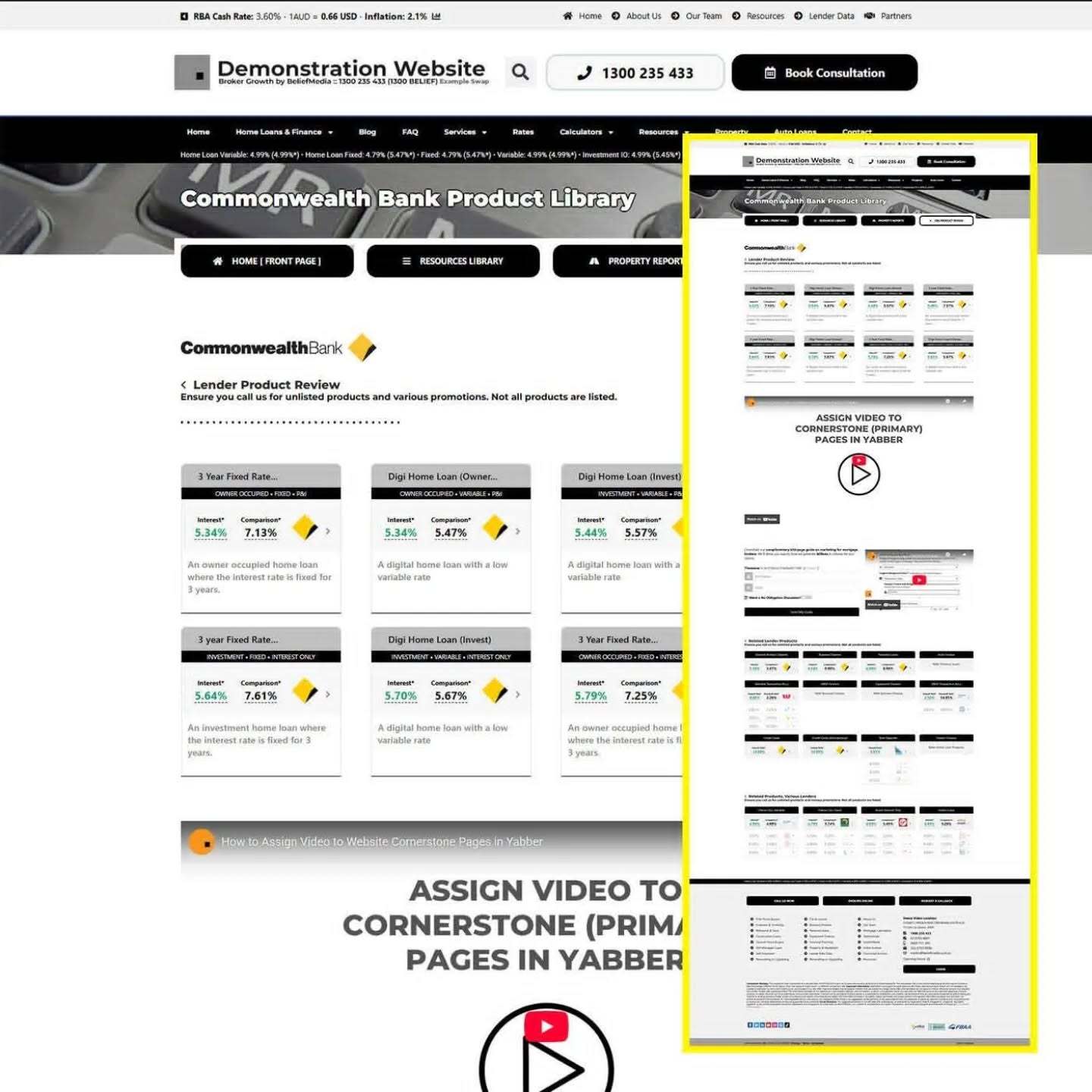

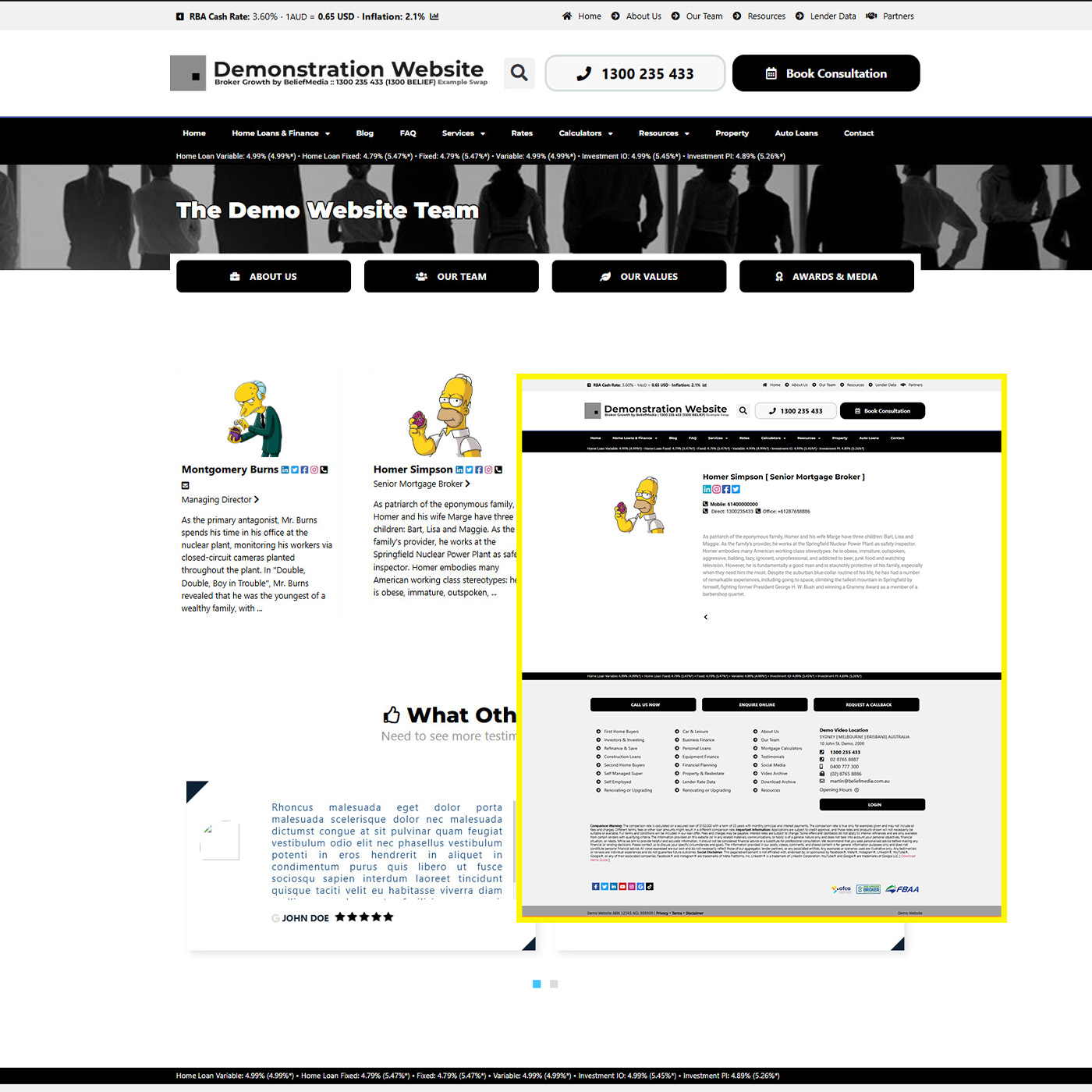

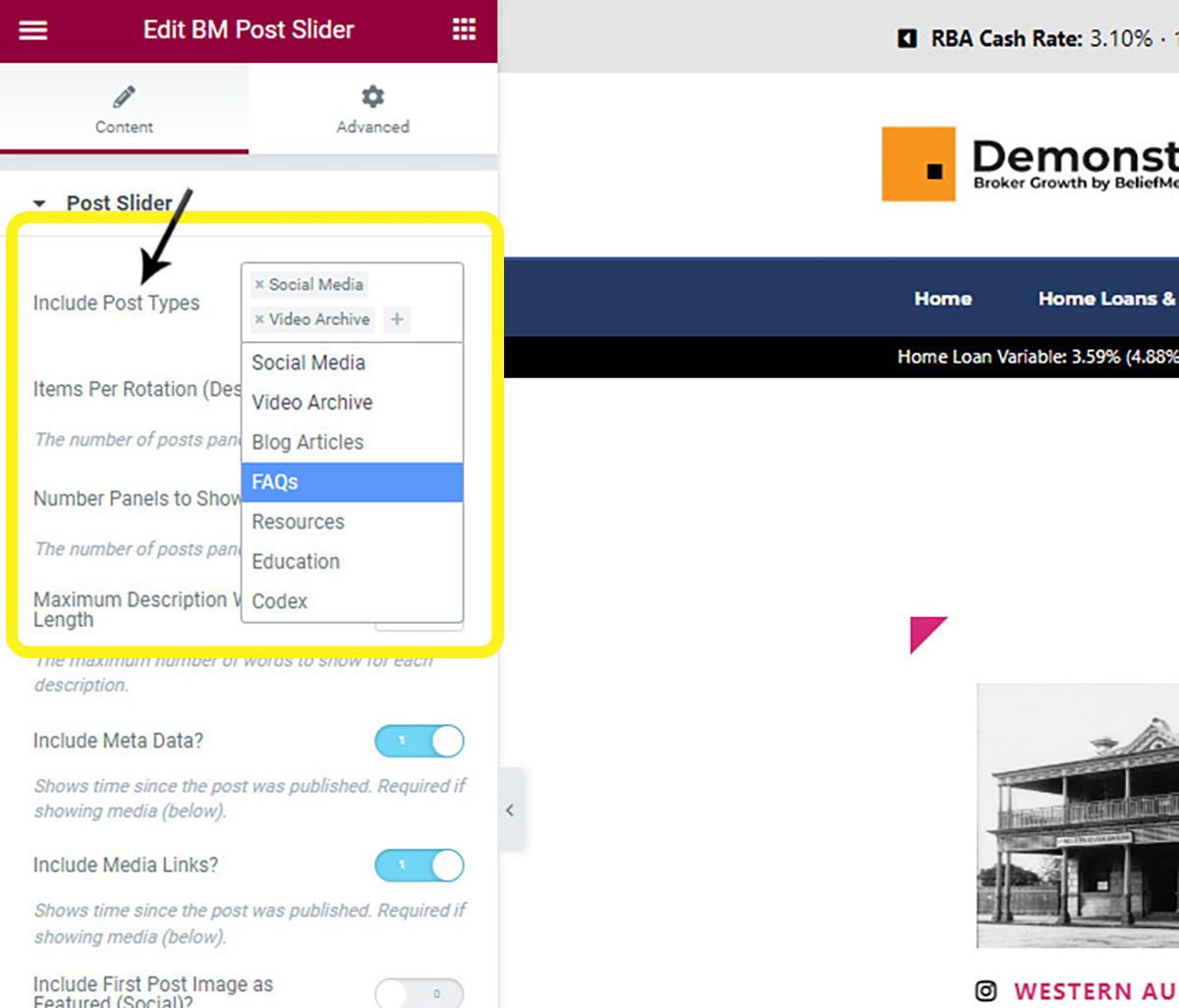

Pictured: The Elementor Post Widget. Drag and drop the widget onto a post or page, select the post types to show, and the slider will start showing results. A large number of options apply that alter the style and formatting of the rendered slider.

Shortcode is available, but the large number of options introduce a complexity that is best avoided. That said, rendering a default slider with only minor changes takes just a few seconds.

Updates to the Social Archive

In building what was a 'simple' slider, we encountered a 'problem' (and an opportunity). In the past, Yabber would create a social article on your website based on the attributes of the post content... but it wouldn't create tags or categories. However, social posts are based on hashtags, so it only seemed appropriate that we'd assign them to each social post created. The assignment of tags (or, in this case, hashtags) means that all content connected via a hashtag may be navigated independently of other content, thus providing a more usable and engaging customer experience.

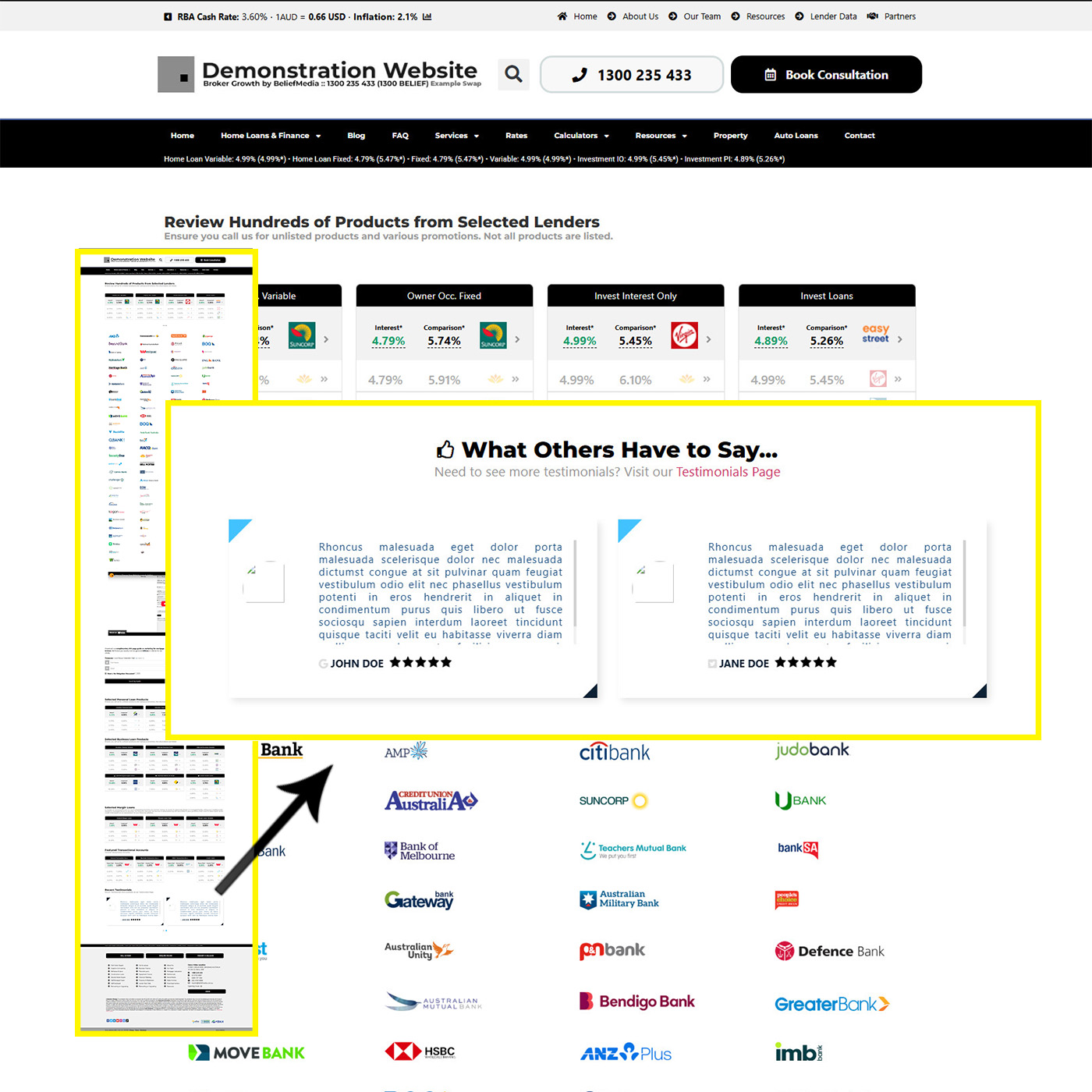

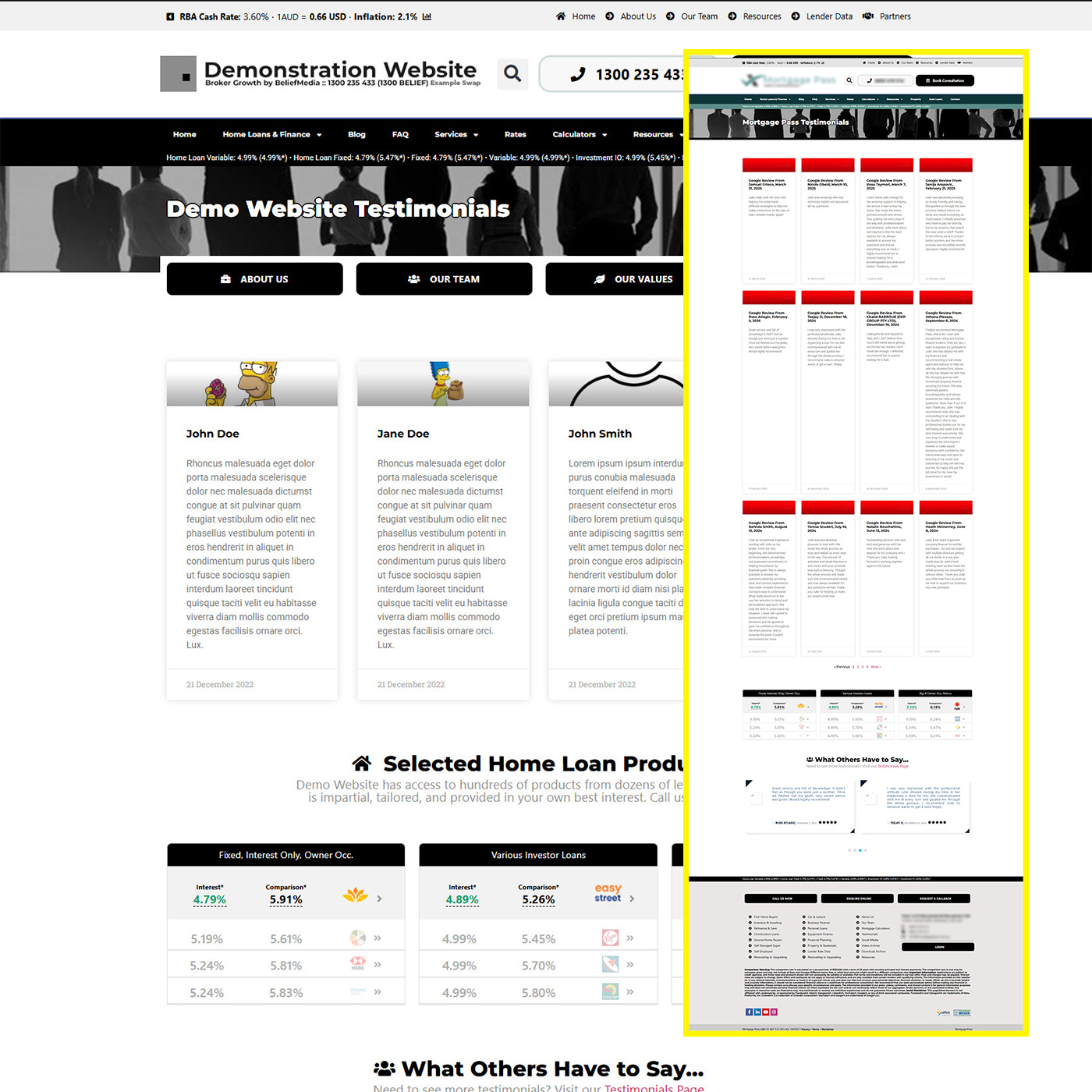

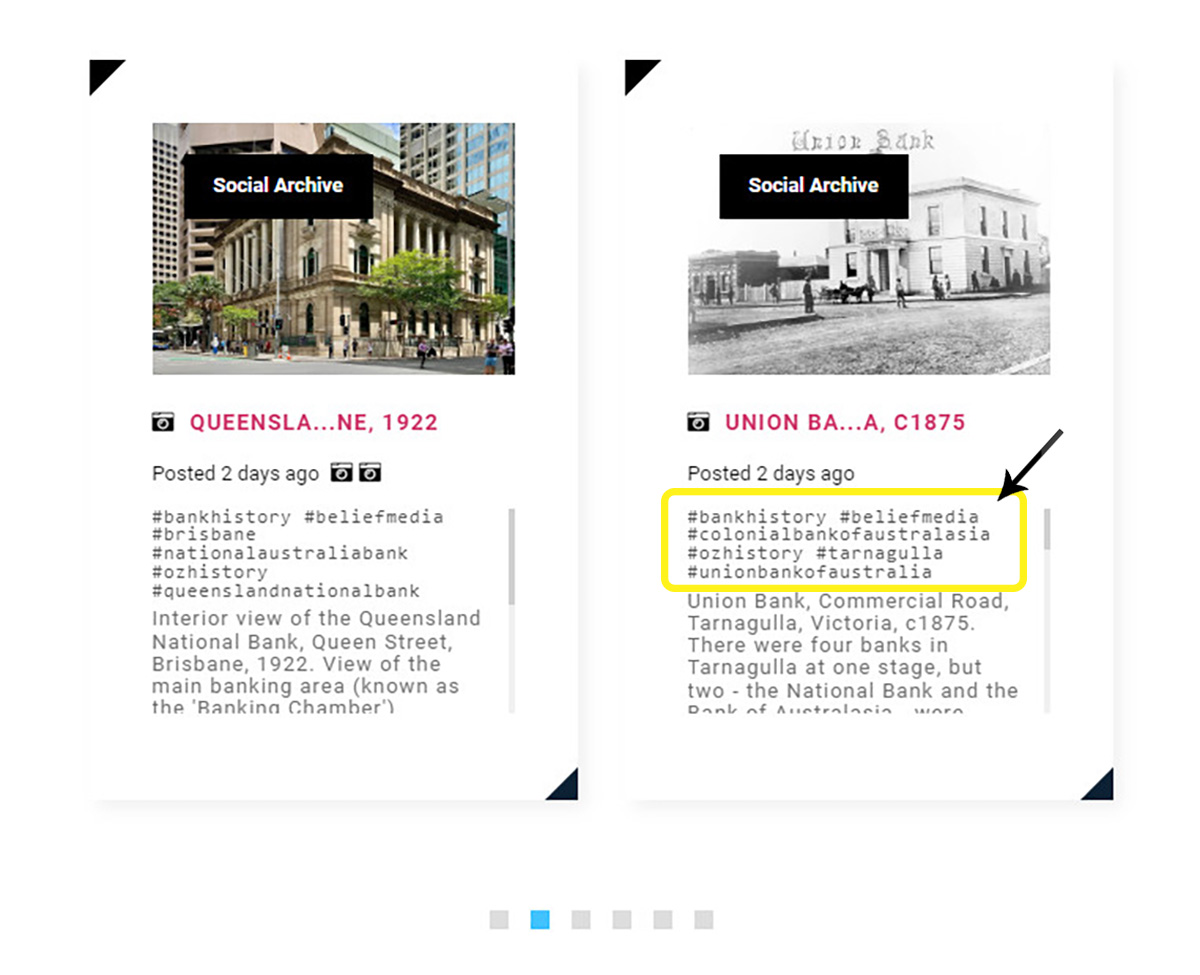

Pictured: The social archive on this website showing images associated with the #bankhistory hashtag. The archive allows a user to experience your social archive as if it were a social network by bouncing around content based on the hashtags associated with the post. This new archive presents some interesting social options we're yet to fully explore.

The framework is now shipped with a social tag archive that is linked to from the tags associated with each post (meaning you're able to browse your own social archive in the same way that you would Twitter or Instagram).

In terms of the slider itself - the primary reason the above changes were made - we now have the capacity to include hashtag links from within each panel, thus giving your website visitors direct access to social, video, and other content that interests them most.

In creating a searchable archive for the social media custom post type, we were required to create a 'hashtag' taxonomy (which is basically an association that connects the hashtag to the post), and we were required to build in a searchable hashtag archive page (or a paginated archive that shows all posts containing a single hashtag). If you're sporting a framework that was delivered anytime before January 23rd, the searchable hashtag archive will not work, and you shouldn't include hashtags in your social slider (or anywhere else) as the tags will link to an invalid page; this restriction only applies to social panels as it's the only location the tags are shown.

For those with an existing website, we'll provide video instructions on how to perform the update yourself (changes were already made on managed client websites). If you're an active social media user, and you're using our social systems, then we'd recommend an update.

Ironically, archived social media posts on your website will almost always have a higher reach than content posted to social media platforms.

Considerations

If you expect to use the slider, consider the following:

- In most cases you will use your post featured image as that which is shown in the social slider. For those cases where you set an unrelated and default featured featured image in Yabber, you may select the first post image

shown in your article as the featured image.

shown in your article as the featured image.

- Video and Social archives are the only two post types that will display 'alternate' content (images for social posts, and a video link for video posts). Other posts types will show in a generic format. The slider can be used for posts from any archive type, including just those from your blog (supplements an existing default Elementor tool).

- There are a large number of Elementor options . In most cases you will only select the post type, and alter only those values that are related to your brand. You may select your brand 'global' colour so that any updates in the future will alter the colours to all slider instances. It's expected that we'll build a panel in Yabber to set default or specific styles.

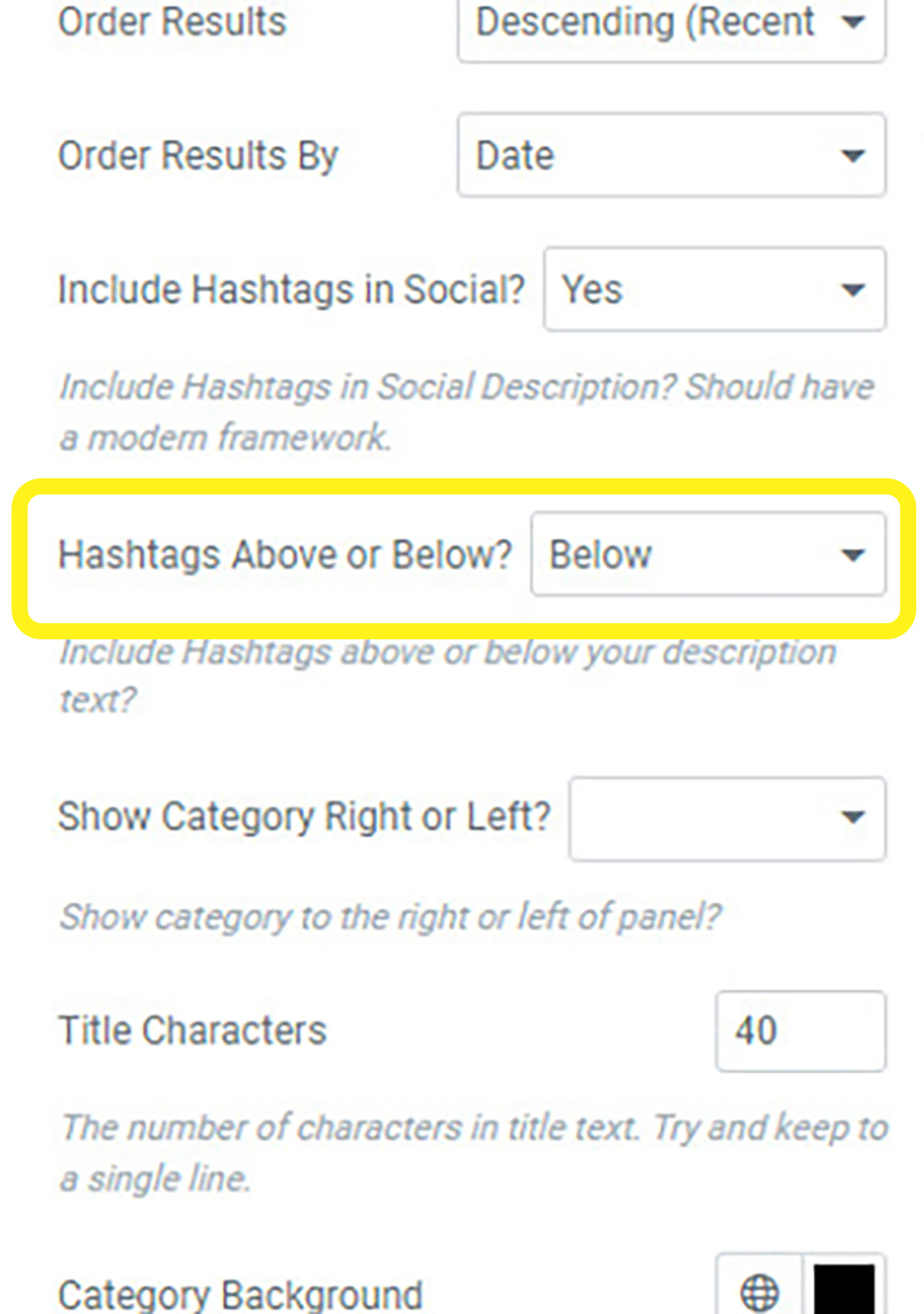

- Linked hashtags in social may be rendered above or below your post text. The option is defined in Elementor or with shortcode. We'll tidy up this option in the near future.

The feature is very new so you can expect minor bugs. Please report them as they're found. Please also forward any feature requests and we'll include them in the next plugin update.

Continued Development

One of the features we've considered implementing into the website framework is the history of lenders and banks in Australia. We've built up a significant archive ourselves, and as we post finance history to your social channels via the managed program, and as you post your own content, we can link that content to a 'history' page with more information. It's a little 'outside the box' so we'd appreciate your feedback on this type of feature.

Aggregation & Franchise

While it's yet to be used, Yabber provides for an aggregation or franchise group to include a full library of social content from all brokers on a dedicated or company website, with each post linking back to the original author - this style of social tool may also be suitable for an operation with a larger number of independent brokers. The idea is that we want our social media efforts to be archive and come alive before its buried deep down under thousands of feet of cat pics and dancing babies.

Conclusion

We're often required to explain why a company often perceived as a 'lead generation' company applies so much effort into building industry leading website tools... and the answer is a simple one: your website is required to support a full-stack marketing funnel, so the persuasiveness and value derived from your broader digital experience contributes towards your conversions. Simple.

While the slider is a fantastic tool that elevates the awareness of your social media content, it's the evolution of the social media archive that is probably more significant. Hosting your own social and video material gives you complete ownership of your own content. The searchable hashtag archive makes your website come alive with a complete searchable library of the content shared to social, and the system adds significant SEO value in the process.

Coming Soon: One of the more significant steps we've taken in this whole process was the modification of the backend framework to support a facility that will permit you to post to social media from within your social media archive. In other words, you will create content on your website, and the content and media associated with the post will send to selected social accounts. This tool will supplement the Vista and Instagratify tools, and will arguably be a more efficient mechanism for creating social content.

The last of a slider-style tool that we'll build in the short-term will return selected videos uploaded to YouTube and/or Wistia in a video slider, and the Elementor tool is expected next week.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}